Issue 1) Widening $1T fiscal deficits are causing large supply of UST at unprecedented % of GDP outside of recession/war.

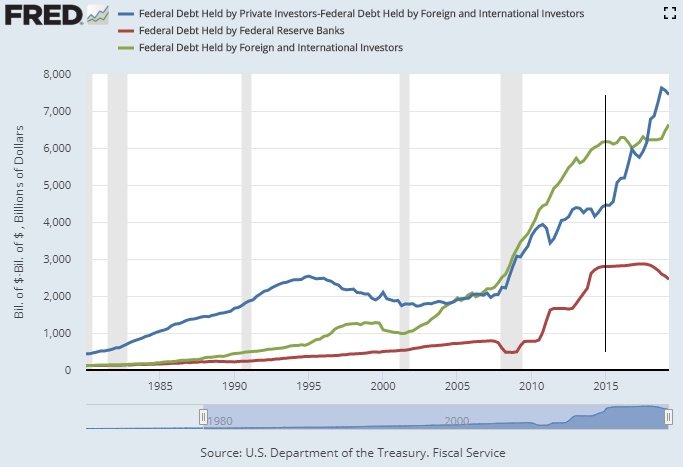

Issue 2a) In last five years, foreign sources and Fed not buying UST. Private domestic balance sheets (blue line) have thus absorbed $3T in new UST in those five years.

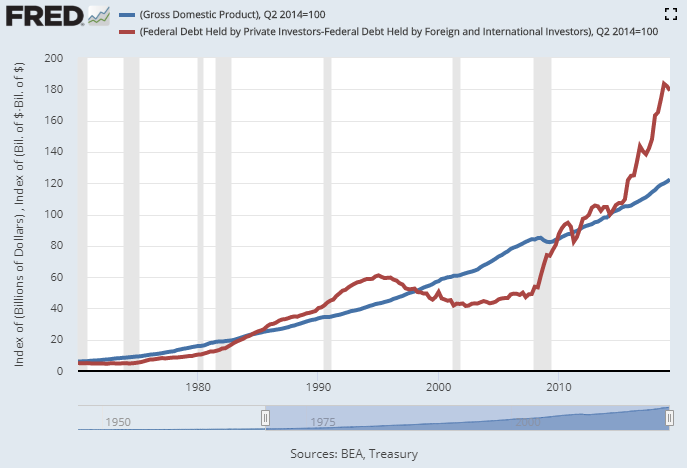

Issue 2b) 12.3% annual growth of domestic UST holdings vs 4.1% annual nominal GDP growth over past 5 years = unsustainable in long run. Chart indexed to 100 five years ago showing domestic UST holdings vs GDP.

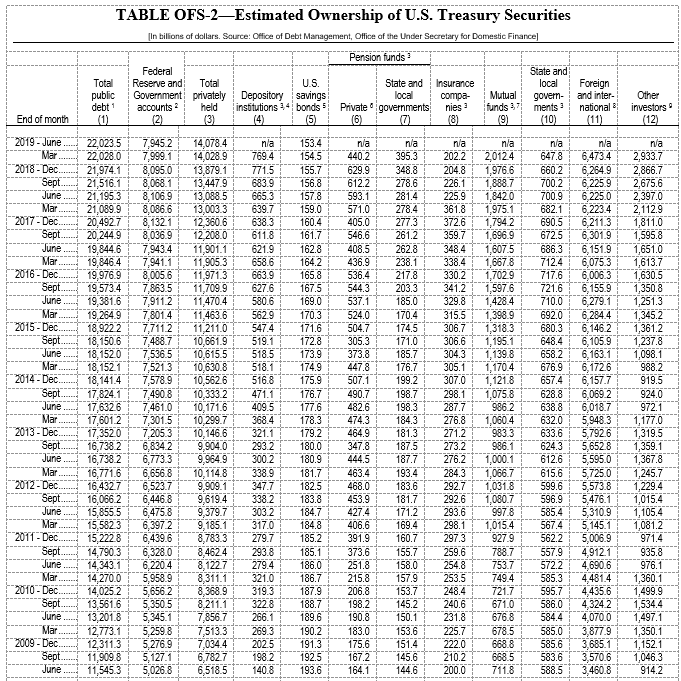

Issue 3) Biggest UST buyer in 2018 was the “other holders” category, which includes non-financial corporates. (S&P500 holds a lot of t-bills.) “Other holders” bought $1T in UST in 2018; by far the most of any group, and way more than they bought in 2017.

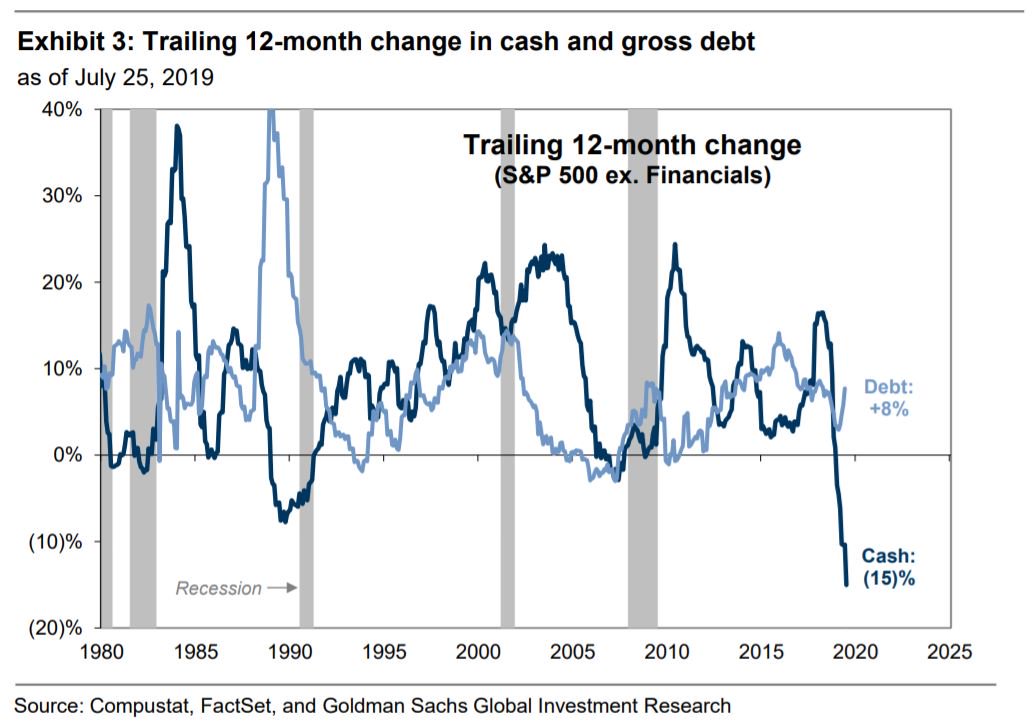

Issue 4) 2018 was the tax cut year of cash repatriation for S&P 500, which paid for record buybacks, and their cash/t-bill levels briefly went up. Now there’s a cash/t-bill drawdown in 2019 for more buybacks without repatriation. https://www.marketwatch.com/st...

Issue 5) Add proximate timing issues on top of rather saturated domestic balance sheets (tax payments, Treasury refilling cash levels, etc.)

Result) If other/corporate category not buying UST heavily in 2019, after being biggest buyer in 2018, & other domestic balance sheets near limit, could cause demand issues. So, Fed Funds over IOER for months, weak UST bid-to-cover all year, then repo spike.

A new buyer of UST is likely needed. Probably will be Fed. Start small then ramp up.

@LynAldenContact this is helpful thx @chigrl @LukeGromen

@LynAldenContact @LukeGromen Excellent; clear & concise description. Thx!

@LynAldenContact I looked at your blog just now- very cool!

@LynAldenContact @threadreaderapp unroll

@LynAldenContact @threadreaderapp unroll please. Thanks