People are saying I am not posting enough finance content. FINE. Once you have decent alphas a lot of the skill in running a systematic strategy is reducing turnover. Alpha is unknown but trading costs are certain. Keep trading to the minimum needed to monetise your alpha.

If you have a univariate strategy (all assets independent, no portfolio considerations) a simple heuristic is to use a no trade region. Your strategy outputs a target position x at all times and you compare it to your current position y.

Introduce a new buffer parameter b. If y < x - b then trade until your position is x - b. If y > x + b then trade until x + b. Otherwise you are in the “no trade region” and you don’t trade.

Another way to say it — you have an interval of width 2b around your target position, and if your position is outside that interval you trade until you are at the edge of it. Larger values of b will reduce turnover more.

How to pick b? A few ideas 1. Optimise it in a backtest (eg to maximise net Sharpe ratio) 2. Pick it to target a particular turnover, eg if your forecast horizon is ten days you hope to turn over ~20% of your book per day, so pick b to achieve this

3. Pick a sensible value based on your max position size, eg 5-25% of max position size.

I’m normally against optimising parameters based on a backtest but this is quite a benign optimisation. The main danger is that if your edge is overestimated, your optimisation will pick a value of b that is too low, so you should be conservative (eg double the “best” value of b)

In practise I normally do either 1 or 2, but 3 is a good check that you have selected a sensible value.

There is a mathematical model that produces this trading rule btw! If you have linear alpha, quadratic risk and trading costs proportional to trade size (eg a fixed bid offer spread) this is the trading rule that results. Can run through the math if there’s demand. Fin.

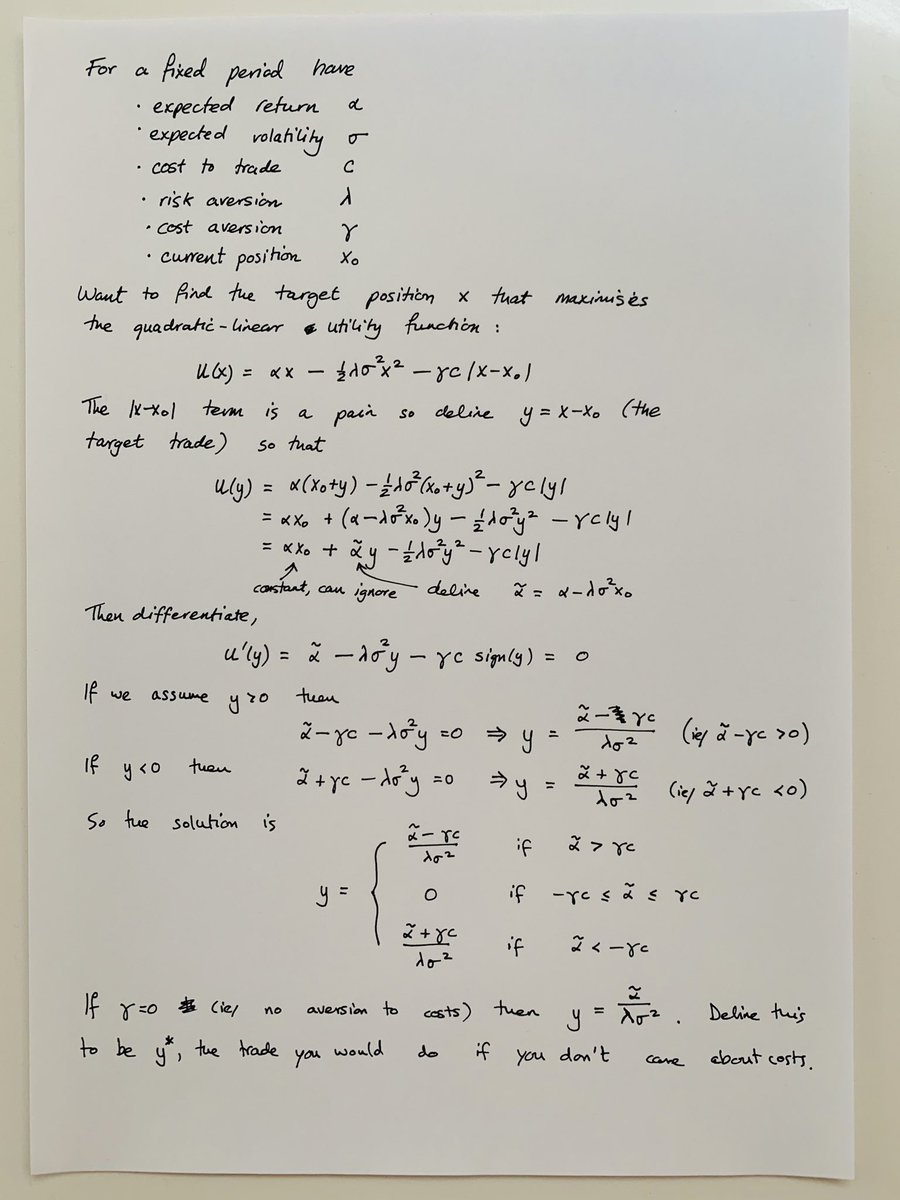

This is a sort of “folk knowledge” in quant finance. It’s rarely discussed in books/papers because it’s so basic that it’s assumed everyone knows it, so I couldn’t find a good reference for it. Derivation is below.

Nice thing about knowing the derivation is that it’s straightforward to extend it eg other t-cost forms (3/2 or quadratic), multiple assets (sigma becomes a covariance matrix) or introduce constraints on position size or turnover. Most extensions need to be solved numerically.

😬