This bet has been analyzed to death but it came up in my feed recently and I couldn't find an actually intuitive explanation anywhere. Black-Scholes and simulations are cool and all, but what's the ELI5 for why Do Kwon got picked off?

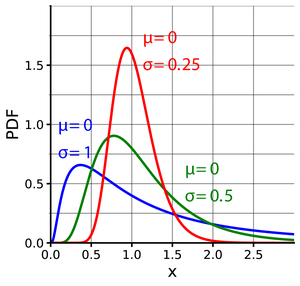

Let's say LUNA is worth $X right now. Markets are random, but in expectation, LUNA's price a year from now is $X (assume zero interest rates and shorting is easy). The price can't go negative but can be arbitrarily high. So the one-year return might look like one of these curves.

The important thing is, the bet here is an over/under as opposed to a typical trade where one side buys and the other sells. That is, Do made a good bet if and only if 50% of the time LUNA is above $X in a year. It doesn't matter by how much!

But look at these graphs: the price distribution is right skewed, i.e. the median (50% mark) is left of the average. Since the market is pricing in that the average is $X, the median must be less than $X. Therefore Do made a bad bet.

So next time you make an over/under bet on the price of a financial asset, maybe set the threshold to less than the current price. Not financial/gambling advice, just some plain English analysis without fancy math formulas.

@chameleon_jeff Cool breakdown. For us smooth brains. Would this compare to buying options and just having it expire out of the money if price ends under ?

@KingJulianIAm Yeah you can totally model the trade using a combination of options. You have to have multiple options together to recreate the capped upside though. But yeah the bet Do took is like buying this combo of options at the wrong price.