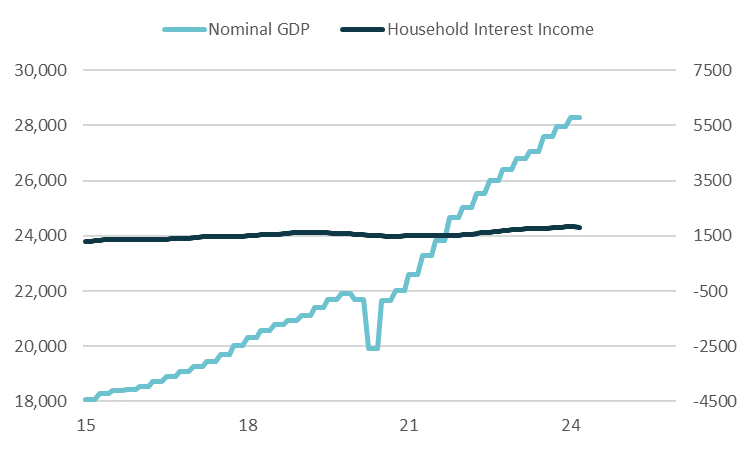

Its tough to make a quantitatively driven case that the interest income from higher rates has been an important driver of recent US GDP growth. Since rates meaningfully started rising in 2022, HH interest income is up about 275bln while overall GDP is up 3.6tln:

The impact is likely materially lower as well. Much of the interest income earnings is concentrated in high income/wealth cohorts who have a high propensity to save rather than spend. Even a 50% spend rate (high) would have only added 50bps to nominal GDP over the last 9 qtrs.

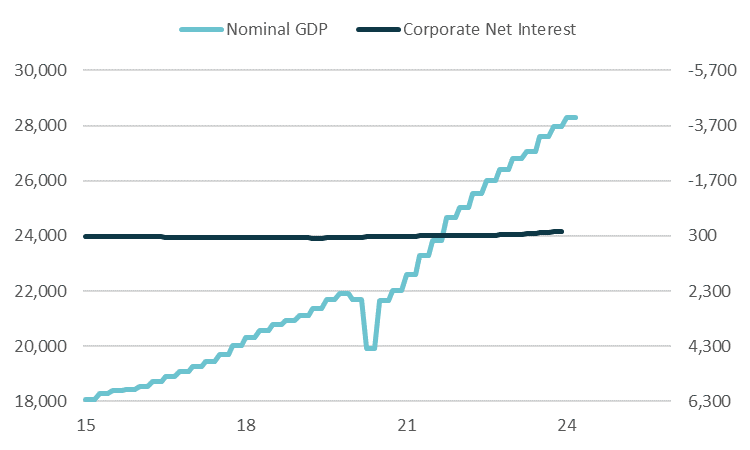

Interest income on corporate cash savings has also garnered a lot of attention but looks pretty small. The *net* interest expense for the corporate sector has fallen by about 150bln over the course of the last 2+ years, which is tiny relative to GDP growth.

Of course thats on a net basis and some companies are paying more interest and some are earning more. The more lagged, lower frequency data on gross income earned is only through '22, but doesnt show much uptick. Even tripling in size would still only be a few 100bln.

And that of course doesn't take into consideration the fact that biz incremental propensity to spend / invest isn't really much driven by the incremental income earned on assets. A much bigger force in the economy is likely the drag from much higher rates on desire to borrow.

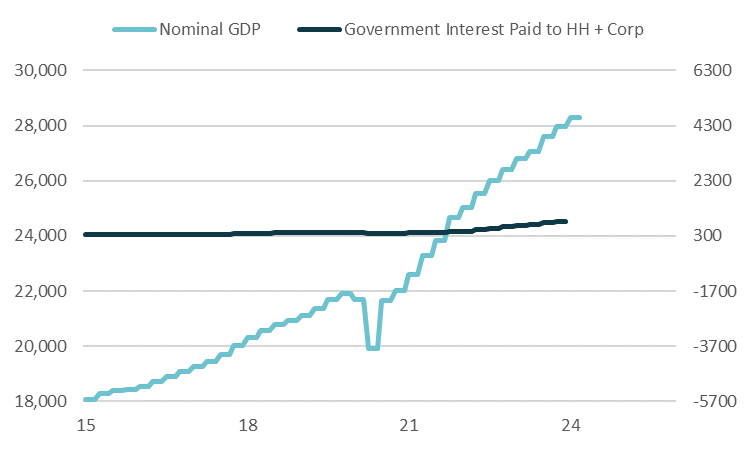

Another way to triangulate this picture is from the government side by looking at the estimates of how much gov interest is being paid to HH+Corp (the GDP producing sectors). This suggests a rise of 300bln in payments in the last 2 years, which roughly triangulates with above.

Put together, it looks like the income from higher rates is a marginal support to incomes & spending for HH + Corp but it really doesn't look like a substantial driver of the expansion in recent economic activity.

Folks pointing to income as the primary driver of the expansion are likely confused as to why growth is so strong when traditional drivers of expansion like credit and money growth are so weak. "Income-dominance" is unusual vs past cycles: https://x.com/BobEUnlimited/st...

While higher rates have likely been a support to some spending, the numbers suggest its small in the context of the expansion. As a result its a better indicator of folks who are not doing quantitative work to understand the drivers of the economy than explanatory of US growth.