NEW FROM US: Carvana—A Father-Son Accounting Grift For The Ages https://hindenburgresearch.com... $CVNA (1/x)

$CVNA is a $44 billion online car dealer founded in 2012. Its main business is an online platform that allows retail customers to buy and sell used cars. (2/x)

Despite facing bankruptcy risks in 2022 and 2023, $CVNA's stock spiked 284% in 2024, with investors believing the company’s worst days are behind it. (3/x)

However, our research, including extensive document review and 49 interviews with industry experts, former Carvana employees, competitors and related parties of the company, undertaken over the course of 4 months, shows $CVNA's turnaround is a mirage. (4/x)

Our research uncovered $800 million in loan sales to a suspected undisclosed related party, along with details on how accounting manipulation and lax underwriting have fueled temporary reported income growth – all while insiders cash out billions in stock. (5/x)

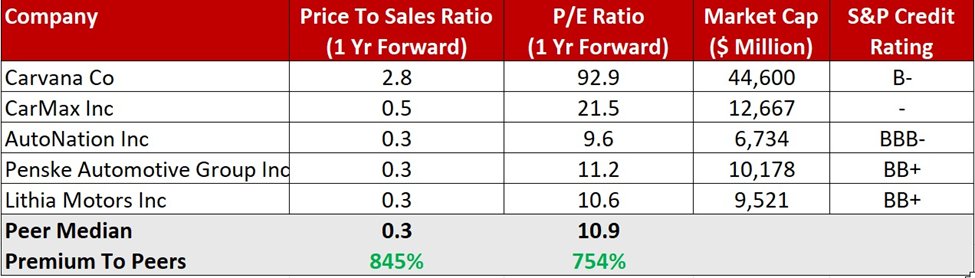

Even before considering our findings, $CVNA is exorbitantly valued, trading at an 845% higher sales multiple relative to online car peers CarMax & AutoNation, and a 754% forward earnings premium. $CVNA has ~$4.8 billion in net debt and is junk-rated by ratings agencies. (6/x)

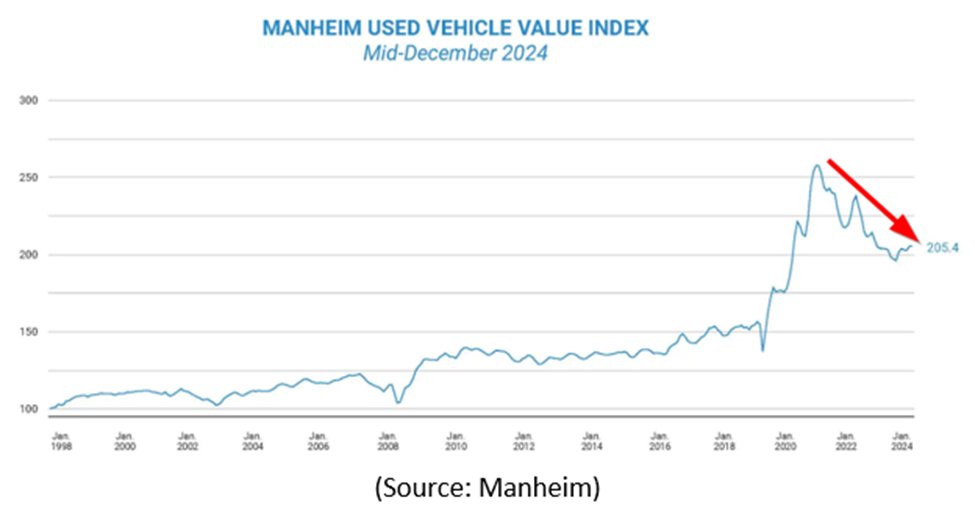

Carvana’s business already faces major headwinds. Used vehicle prices have declined 20.3% in the past 3 years, according to the Manheim Price Index. Subprime auto loan delinquencies are now higher than during the Global Financial Crisis, per Fitch. (7/x)

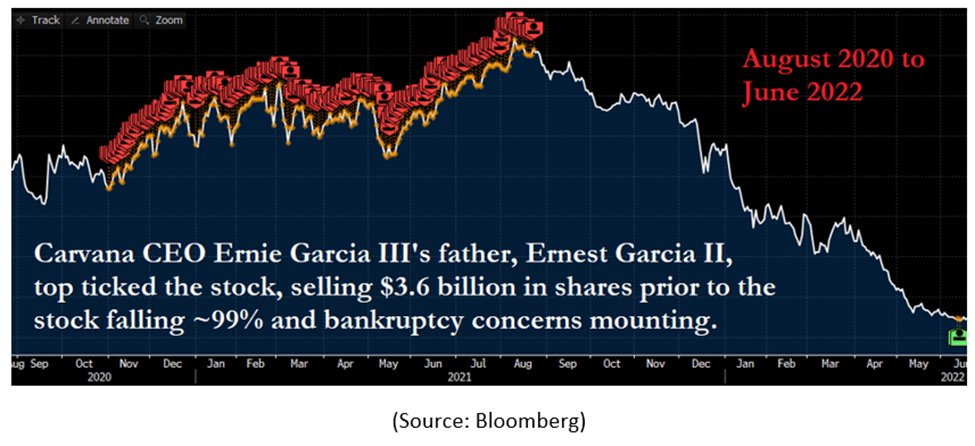

Previously, Carvana CEO Ernie Garcia III’s father, Ernest Garcia II, sold $3.6 billion in stock between August 2020 and August 2021. In the year after he stopped selling, Carvana’s stock plunged 99% and faced bankruptcy concerns shortly thereafter. (8/x)

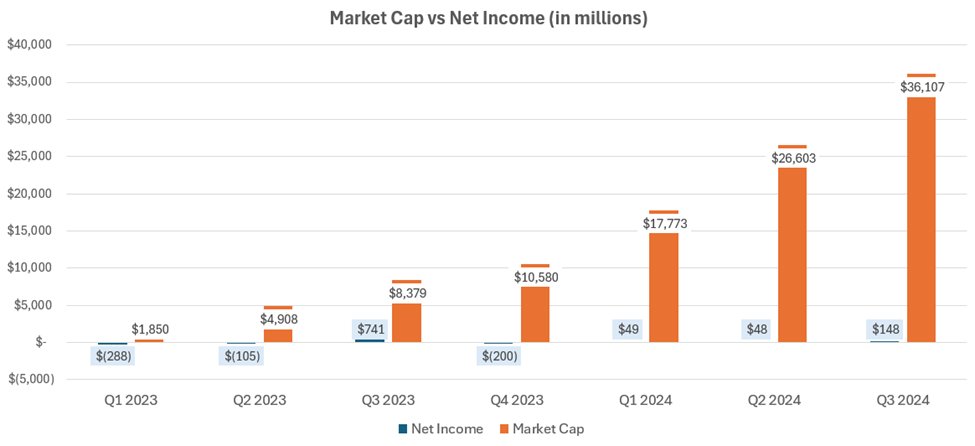

Since 2023, we see the same trend: $CVNA has touted a bright future and posted three consecutive quarters of modest positive net income, an aggregate of $245 million, despite stress in the used auto market. (9/x)

For every $1 in net income it reported, the company has added $139 in market cap – a $34 billion market cap increase. With $CVNA shares up ~42x, father Ernest Garcia II has sold another $1.4 billion in Carvana stock. (10/x)

As insiders unload stock, solvency risks remain. Almost 26% of $CVNA's gross profit consisted of sales of customer auto loans to 3rd parties, largely in the risky subprime and deep subprime space. Gain on loan sales was 2.2x Carvana’s net income in the past 9 months. (11/x)

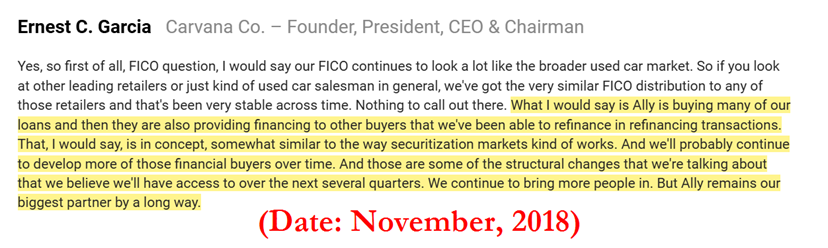

Carvana has relied on a purchase commitment agreement with Ally Financial, to which it sold $3.6 billion of vehicle loans in 2023, ~60% of its total originations. (12/x)

Carvana has told investors for at least 6 years that it is seeking to diversify outside of its relationship with Ally, but thus far has not announced new financing partners. (13/x)

After calling off an earlier agreement in principle with Carvana around 2019, a Wells Fargo senior manager told us: “As we dug into it, the more we learned, the less we liked about it.” They cited specific concerns about lax underwriting & related-party loan servicing. (14/x)

As subprime auto has declined, Ally has amended its arrangement with Carvana 5 times in the last two years. Each time, Carvana redacts crucial information that would help investors understand the terms of the relationship. (15/x)

Over the last 2 years, Ally’s loan book has become increasingly concentrated, with $CVNA loans rising from 5% of its consumer auto portfolio to 8.4%. In Sept. 2024, Ally’s stock fell ~20% after warning “on the retail auto side, our credit challenges have intensified”. (16/x)

Sales to Ally have scaled back year to date through Sept. 2024. Carvana sold $2.15 billion of loans to Ally in the period (~$2.86 billion annualized), only 35% of total originations. This compares to $3.6 billion in loans or 60% of total originations in 2023. (17/x)

One Ally executive told us: “We've pulled back from them [Carvana] pretty significantly in 2024.” Ally’s Carvana purchase commitment extends to January 2025, posing a near-term risk to Carvana’s business model should it renegotiate on less-favorable terms. (18/x)

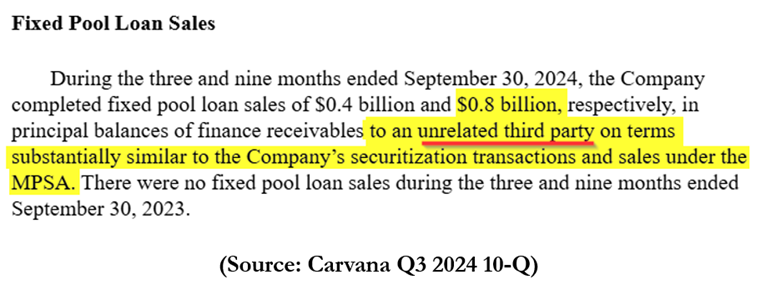

With Ally pulling back, a new, unnamed buyer has quietly emerged exactly when Carvana needed it. In the past two quarters, Carvana sold $800 million in loans to an “unrelated third party.” The mystery buyer made up 18.3% and 16.3% of total loan sales in Q2 and Q3 2024. (19/x)

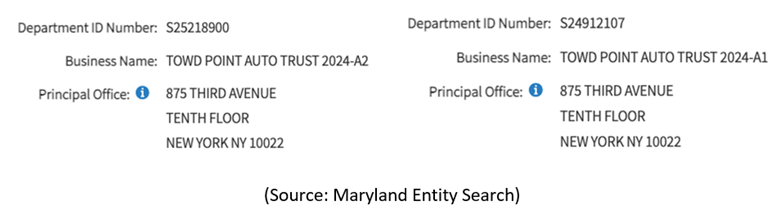

Lien filings reveal the buyer is likely a trust affiliated with Cerberus Capital, where Carvana Director Dan Quayle is a member of its “senior leadership team” & Chairman of Global Investments, indicating the new buyer is an undisclosed related-party, contrary to $CVNA's claims.

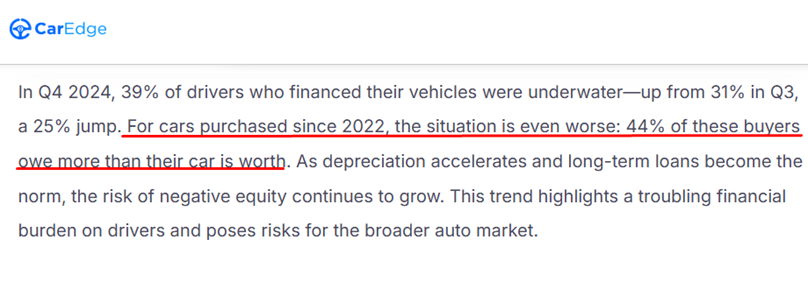

These suspected financing games are occurring as Carvana faces major economic headwinds— 44% of loans for cars purchased since 2022 are underwater, per a recent survey from CarEdge. (21/x)

Carvana’s “originate to sell” model is highly skewed to packaging non-prime and subprime borrower loans. Per a former Carvana director: “I don't think the model is much different than what we saw with kind of the early 2000 mortgage-backed securities". (22/x)

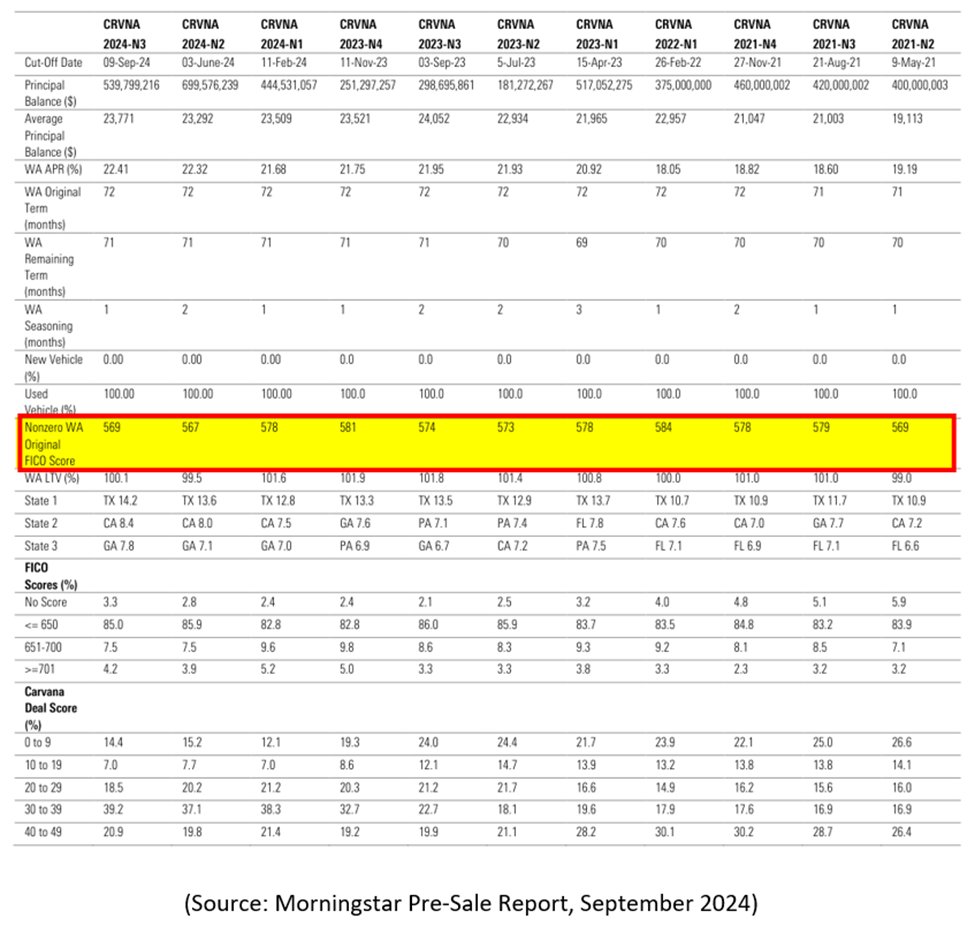

Almost 44% of Carvana’s loans it sells in ABS deals are non-prime. Over 80% of its recent non-prime ABS deals have weighted average FICO scores in the “deep subprime” range, the riskiest levels, per Morningstar data. (23/x)

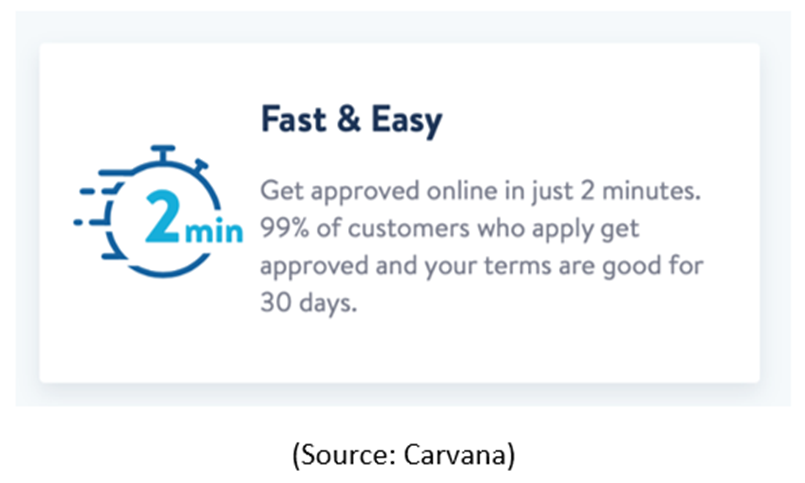

Carvana’s toxic loan book is a result of lax underwriting standards. “We actually approved 100% of the applicants”— interview with a former Carvana director describing virtually non-existent underwriting standards. (24/x)

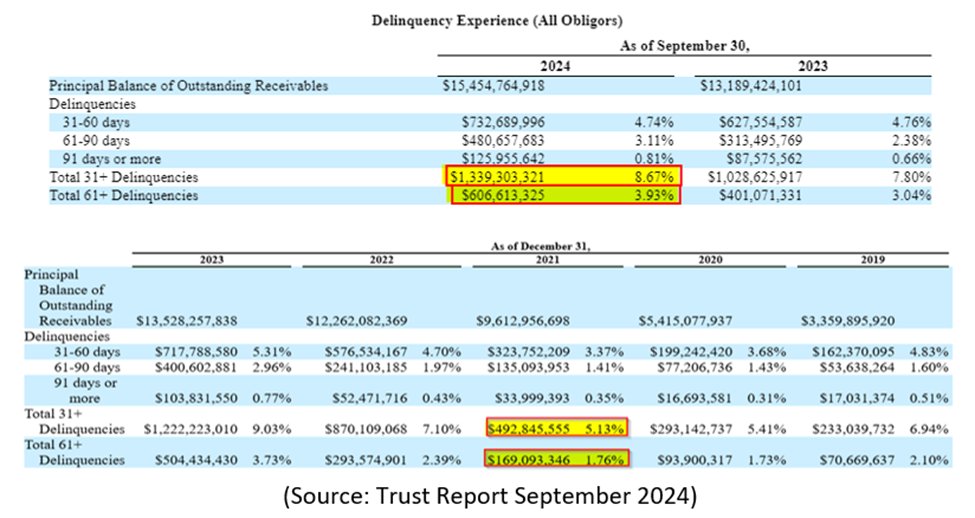

Carvana has issued over $15.4 billion of asset-backed securities (ABS), which it retains partial interest in on its balance sheet. 60-day delinquencies across its supposedly “prime” borrowers are over 4x industry averages. (25/x)

A former Ally executive told us: “Those numbers… my heart might have skipped a few beats…. Those loss numbers are high. The delinquencies across 30/60 buckets are high.” (26/x)

Carvana's subprime loans had the highest increase in borrower "extensions" of any subprime auto issuer, a major sign of stress, per S&P data. Carvana’s extensions more than doubled this year, while most peers saw declines. (27/x)

With its market collapsing, Carvana has propped up its numbers through a grab bag of related-party accounting games. (28/x)

For example, Carvana’s increase in borrower extensions is enabled by its loan servicer, an affiliate of private car dealership DriveTime, run by Carvana’s CEO’s father. The company seems to be avoiding reporting higher delinquencies by granting loan extensions instead. (29/x)

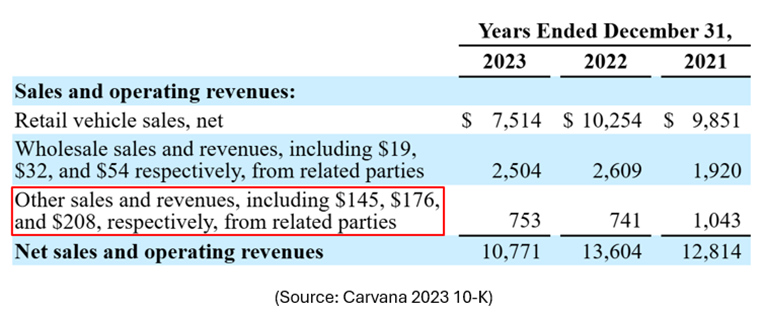

In another example, in 2023, $145 million of “other revenue” or ~8.4% of gross profit came from related parties. This included $138 million of commissions and profit-share from DriveTime. (30/x)

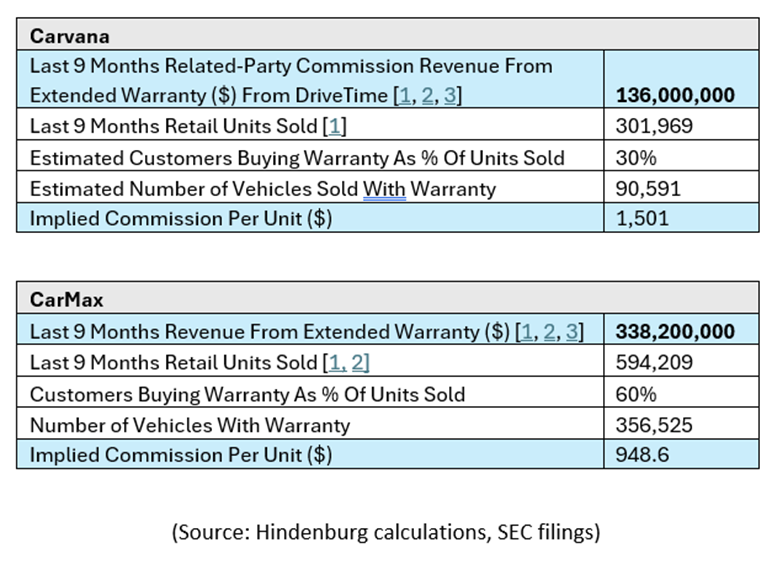

Carvana appears to be dumping unreported costs of extended warranties onto related-party DriveTime, resulting in artificially inflated revenue and profitability. We estimate Carvana reports ~58% more warranty income per sale due to the relationship. (31/x)