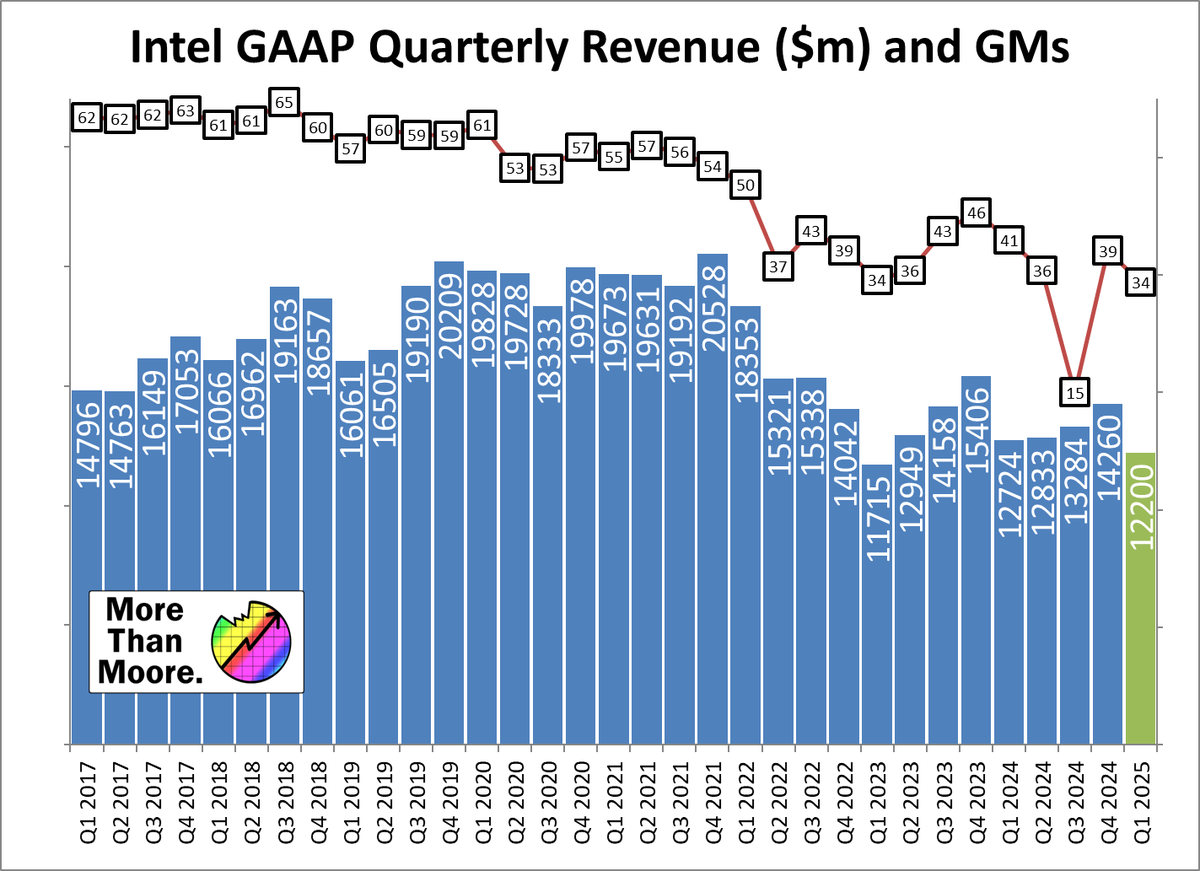

$INTC Q4 Results are in 🧵 💵 Revenue $14.26b, down 7% YoY (Guide 13.8b) 📈 Gross Margin 39.2% GAAP, down 6.5pp YoY 📈 Gross Margin 42.1% non-GAAP, down 6.7pp YoY (Guide 36.5) 💰 Net Income -$0.1b, down from $2.7b 🪙 EPS -$0.03, down from $0.63 Beat guidance quite comfortably!

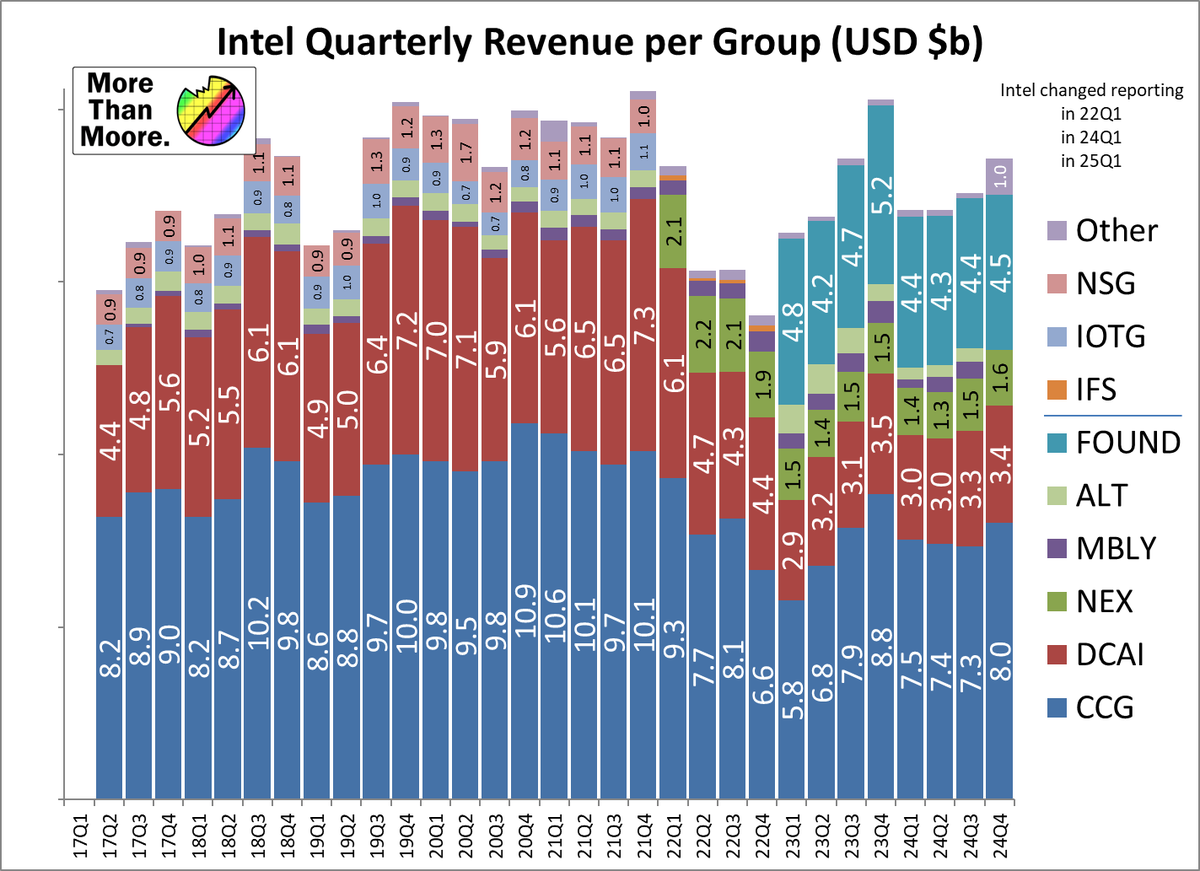

Highlights: - Altera and MBLY are now moved into 'other' - CCG had a really good Q - DCAI revenue up, but margin down - NEX all looking up - From NEX, Edge to CCG, Network to DCAI - Foundry steady on revenue but OM is a lot better

Client Computing Group (CCG) Revenue $8.017b, up QoQ from $7.33b Op Margin 38.1%, up QoQ from 37.1% Strong Lunar and Arrow launches 200 ISVs and 400 AI PC Features 100m AIPC shipped by year-end Launching Panther Lake (18A) in 2H Takes Edge from NEX

Data Center and AI (DCAI) Revenue $3.387b, up QoQ from $3.349b Op Margin 6.9%, down QoQ from 10.4% Expanding Xeon 6 roadmap through H1 Price adjustments, stabilizing market share #1 choice as host processor in AI Strong start to x86 Ecosystem Advisory Group

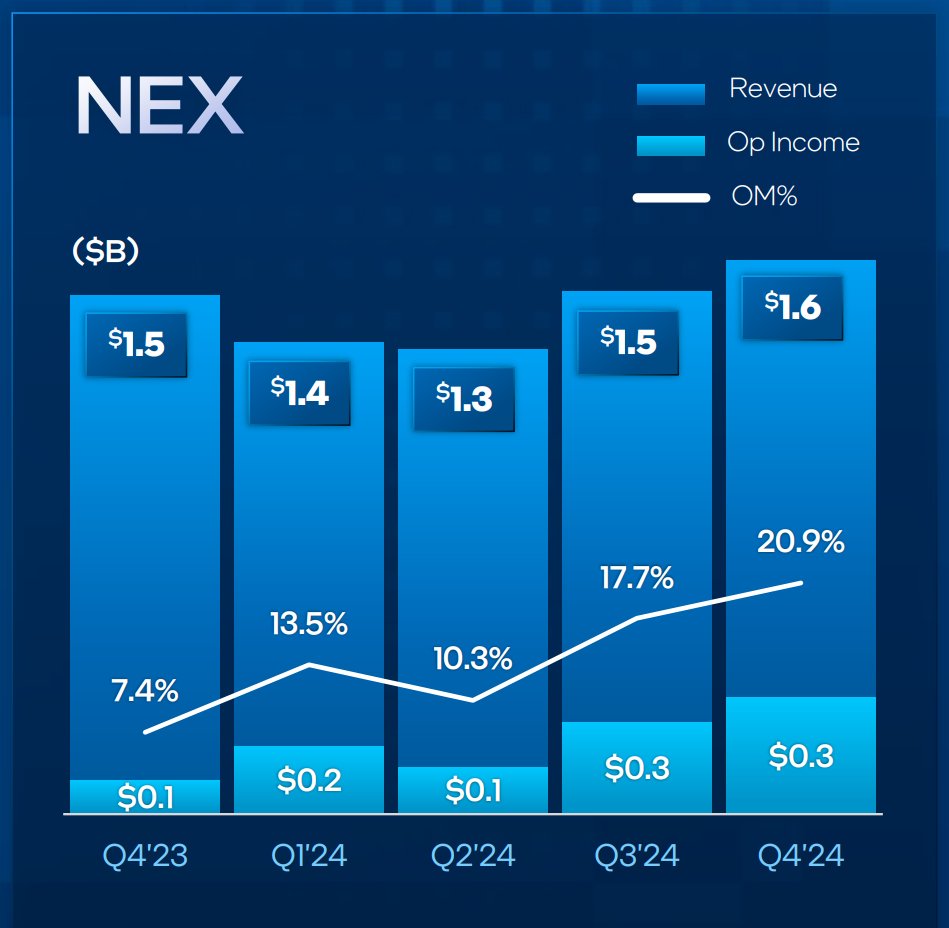

Networking (NEX) Revenue $1.623b, up QoQ from $1.511b Op Margin 20.9%, up QoQ from 17.7% Revenue up >20% from Q2 lows Core Ultra for Edge now launched

Other (MBLY, Altera, all others) Revenue $1.042b, up QoQ from $1.039b Op Margin 11.3%, up QoQ from 4.3% Mobileye with better leverage Altera still experiencing inventory digestion, 2H recover perhaps

Foundry Revenue $4.502b, up QoQ from $4.352b Op Margin -50.2%, up QoQ from -134.3% 18A volume ramp in 2H25, yields proceeding smoothly Margin benefits as EUV ramp matures Margin benefits as 2H products return to Intel Op Inc break even by end of 2027

Other highlights: Employee count down to 108,900 from 124,100 - That's a 12.25% reduction, but includes MBLY/Altera First quarter with zero dividends paid $7.68b awarded on CHIPS Act - First $1.1b in 4Q24 - Second $1.1b in Jan 2025 18A Production ramp in Fab52

Other highlights Full tape out of Intel 16 for external in December, volume ramp at Intel Ireland Launch of Intel 200V with vPro, unveil of 200H, 200HX

Guidance 💵 Revenue $12.2b 📈 Gross Margin 33.8% After Market, $INTC is up 1-2%

Stay tuned for the analyst Q&A!

From the prepared remarks ➡️ Intel Products executed to drive revenue in the quarter, even as PC inventory continued to normalize ➡️ Intel Foundry drove incremental operating efficiencies while achieving key grant-related milestones, which supported solid upside to gross margins

➡️ In client, Intel CPUs power roughly 7 out of every 10 PCs. ➡️ Intel as the market leader in AI PC CPUs ➡️ On track to ship more than 100 million cumulative systems by the end of 2025.

➡️ Launch of Panther Lake (18A lead product) in 2H 2025. ➡️ Intel Foundry is making on performance and yields.

➡️ Nova Lake coming in 2026 !!!!

➡️ Good progress on Clearwater Forest, first Intel 18A server product, plan to launch in 1H26.

➡️Based on industry feedback, plan to leverage Falcon Shores as an internal test chip only without bringing it to market. !!

➡️ This will support efforts to develop a system-level solution at rack scale with Jaguar Shores to address the AI data center.

➡️ Excited by the launch of Panther Lake this year and the internal ramp of Intel 18A in the 2H that will support increased volumes and improved profitability in 2026. ➡️ The team will re-double their efforts on ease-of-porting, IP availability and best-known foundry methods.

➡️ We look forward to updating you as RFQs become wins. ➡️ Have good momentum in advanced packaging and in our collaborations with Tower Semiconductor and UMC.

➡️ Remain highly focused on goal of delivering break-even operating income for Intel Foundry by the end of 2027. ➡️ Financial benefits of shifting our wafer volumes from Intel 7 to Intel 18A.

➡️ Pleased to sign with the U.S. Department of Commerce a definitive agreement awarding us up to $7.86 billion in grants. ➡️ Received $1.1 billion in 24Q4 ➡️ Received $1.1 billion in January of 25Q1.

We announced our intention to establish an independent subsidiary structure for Intel Foundry to provide clear governance and operational separation. This structure also enables us to seek additional funding options from both strategic and financial partners, which we are now actively beginning to explore.

Tempered revenue outlook based on seasonality and macro-uncertainty (tariffs)...

$INTC CEO search is progressing, but nothing new to report.

Q - Ross Seymour, Deutsche Bank: Talked about no quick fix, but a lot of things to improvee roadmap. on DCAI, is Granite closing the gap? CWF isn't being talked about 2025 for launch or revenue. What will it take and when to close gap? A, MJ: It's going to be 1-2 years of consistent execution to bring customers back to table. GNR is good first step, it closes the gap, customers excited about it. It's competitive in volume. See that continued 2026 to Diamond. For CWF, look at DC in two buckets, P-core and E-core. CWF is more niche market, haven't seen volume materialise as quick. CWF will be 1H26, 18A is doing fine on yield and perf, but has packaging complications to push to 2026, but it will close the gap. It's a journey, not a destination.

Q: Profitability on GM QoQ on Q1, and low point of year, what's head and tailwinds? A: For Q1, contributor will be revenue decline. Mid point down $2b on fixed cost business. But Q4 had revenue beat, the CHIPS agreement took some grant as benefit as cost to sales. Wasn't sure we were to sign in Q4 so didn't guide then, but it pushed margins up. In 1Q, Intel products GM are under pressure this year. Some parts have higher cost, such as Lunar, because mem in package, selling mem at cost, so margins for products all year. Panther will alleviate that for margins. That was always to offset for margins on foundry - see more of a mix EUV in foundry, better pricing, better cost, but also reducing period expenses part of $10b cost reduction. It doesn't really show up in Q1, more later in year. Benefits improving on foundry as mix of EUV increases through the year to Panther, then selling 18A wafers at higher margin. In 2026, panther in higher volume, big benefit to Intel.

Q - Stacy Rasgon, Bernstein: On segment guide for next Q, all products segments are down. What makes DCAI and NEX down same as CCG? A: Little cautions on macro, that affects all markets. Seasonality across all markets, impacts Q1 as well. Combination of macro, uncertainty, and seasonality.

Q: Increased competitiveness on margins on Q1 - is that just pricing? Will that persist? How you think about competitiveness in client and DC? A: New market entrants to CCG - we have good product, but margins are more pressured. Going to stem the market share decline in segment, going to win every socket. GNR is very positive step in competitive direction, but have to stem the tide in share loss - going to fight for every socket. Going to be aggressive and show customers can win with us.

Q: CJ Mews, Cantor Fitzgerald: Under new co-leadership, how has strategy evolved for IFS? A: Not looking to spent ahead of success. Capex guide has come down 22-23 range to 20, that's in support of that strategy. Absolutely wow the customers, but to do that we need to be careful about promises. Deploy capital, engage with customers, do more than promised, customers and suppliers. Main goal of building world class foundry is still in place. Need for another player in this space in leading edge - especially in USA. Aligns with government. Need to generate best ROIC.

Q: 3mo ago, the goal for 2025 was FCF positive. Given Q1, what's that path? A: We're not guiding beyond Q1, did very good job in 24 around cash from operations. While neg in 24, closer to zero than should have been given top line. More of the same in 2025, focused on cash flow from operations and others. Do expect significant offsets, more than 10b of offsets, that will help too. It's a focus. We have non-core businesses, see monetization there - see leverage of those. Altera is doing that, earnings next Q will likely say more.