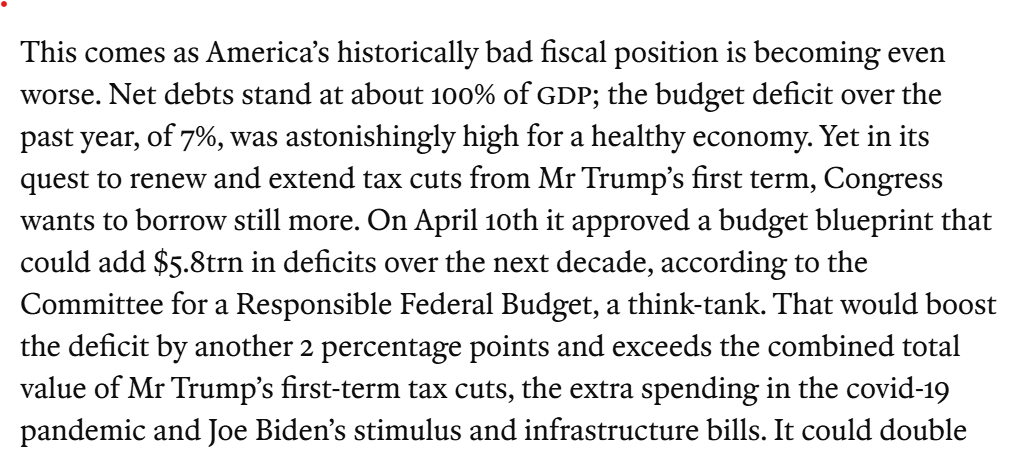

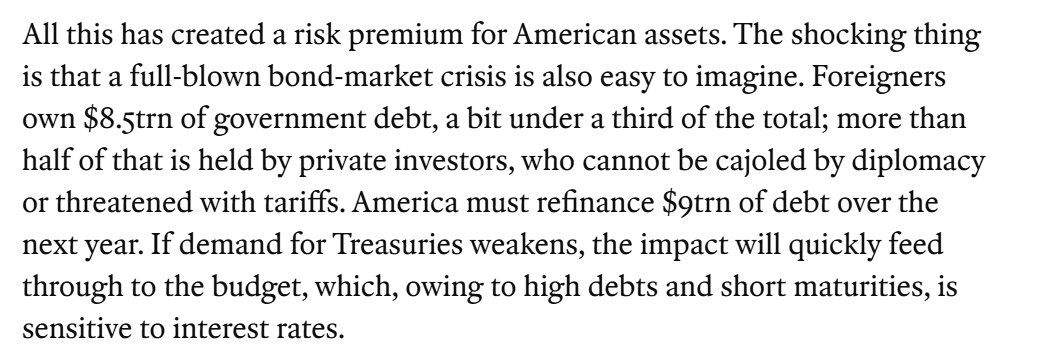

The Economist this highlights the dollar's recent drop & the risk of a future fall. It was striking that they made the argument essentially on fiscal grounds (tax cuts + a desire for easy money spook the bond market). The balance of payments enters only tangentially 1/

External factors weren't entirely ignored, but they weren't the focus either -- even though conceptually a discal crisis is a bit different than a dollar crisis (folks can sell bonds for cash w-o exiting the dollar) 2/

The Economist thus joins the IMF in, well, thinking almost exclusively in fiscal terms (see the IMF's market access debt sustainability framework) even though a true dollar crisis requires, well a flight out of the dollar into foreign assets ... 3/ https://www.economist.com/lead...

What the Economist left out is the clear deterioration in what I would call the dollar's external fundamentals (and unlike some, I do think they matter even for the dollar) ... 4/

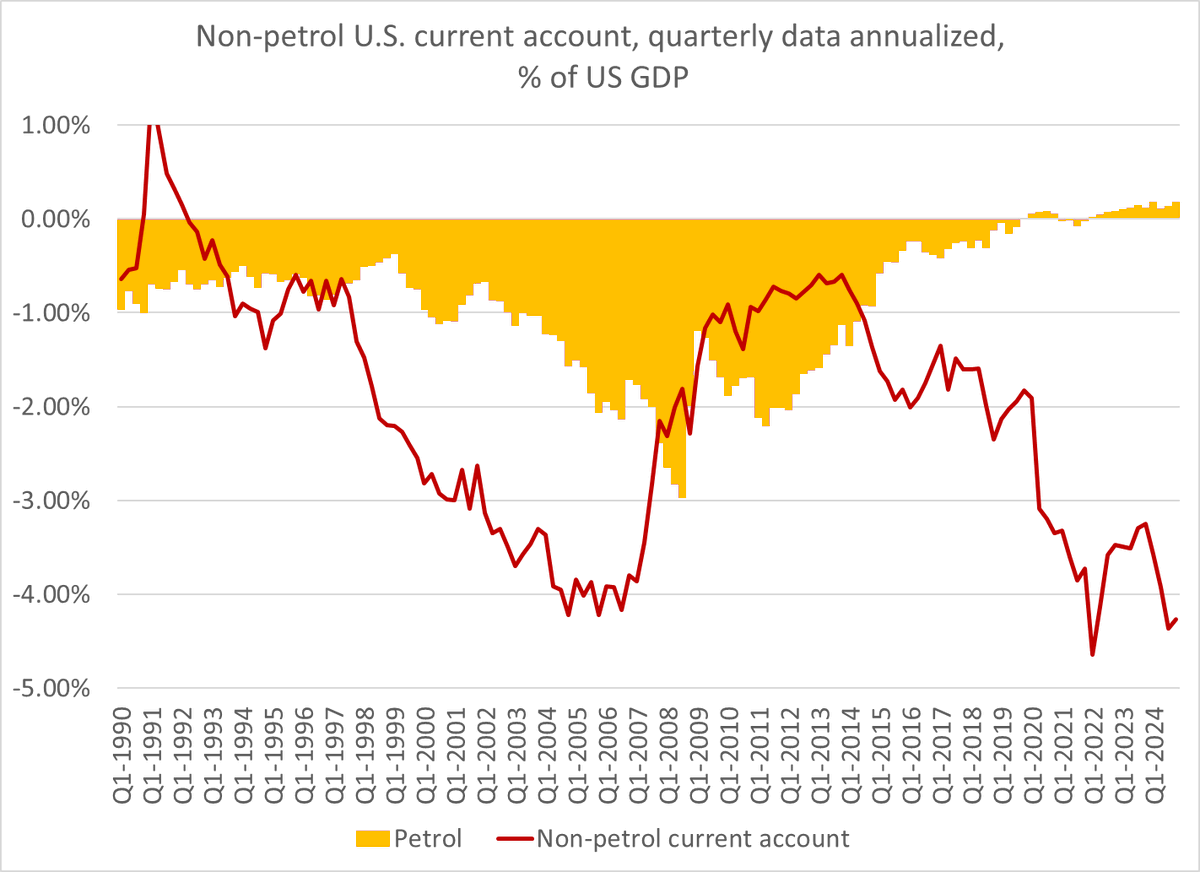

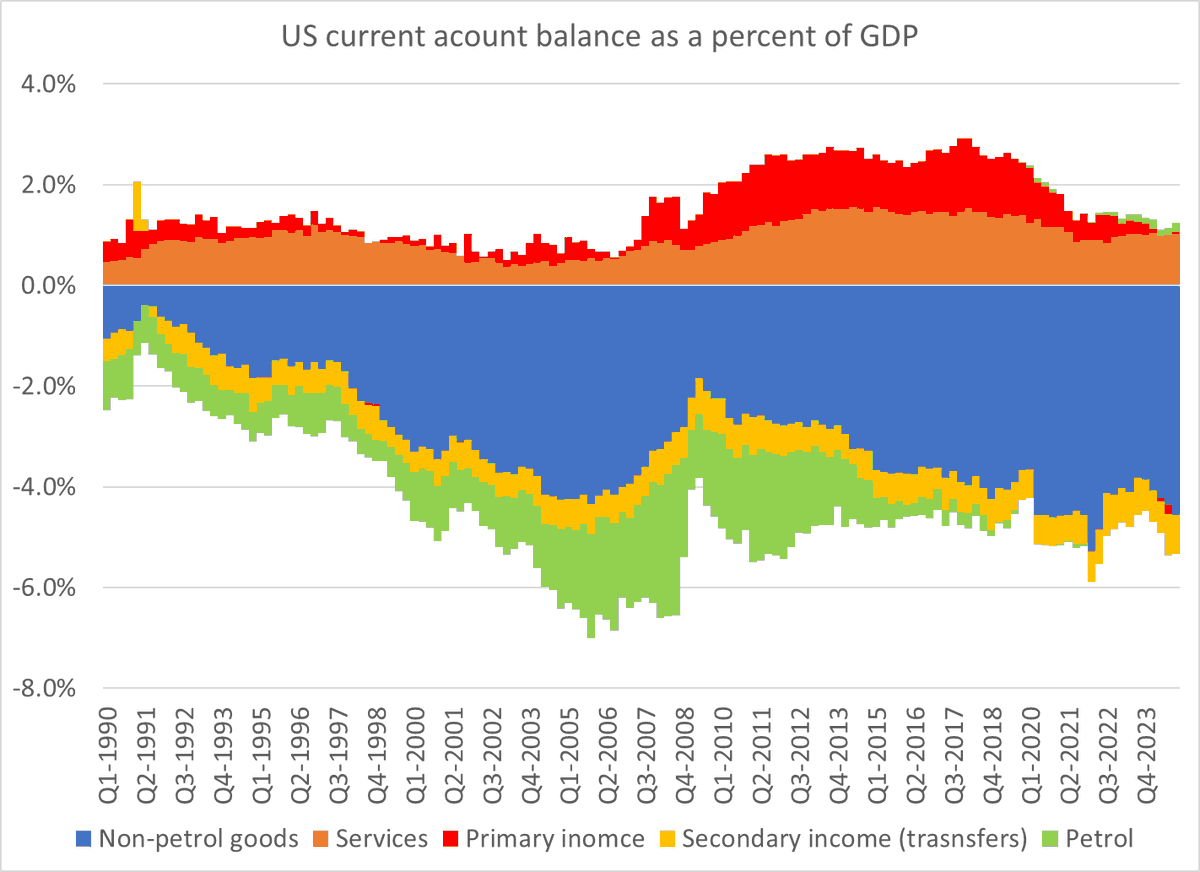

The non-oil current account is back above 4% of GDP (and will be 5-6% of GDP in q1 with all the tariff distortions), the petrol surplus will fade away at current oil prices and the investment income surplus has disappeared 5/

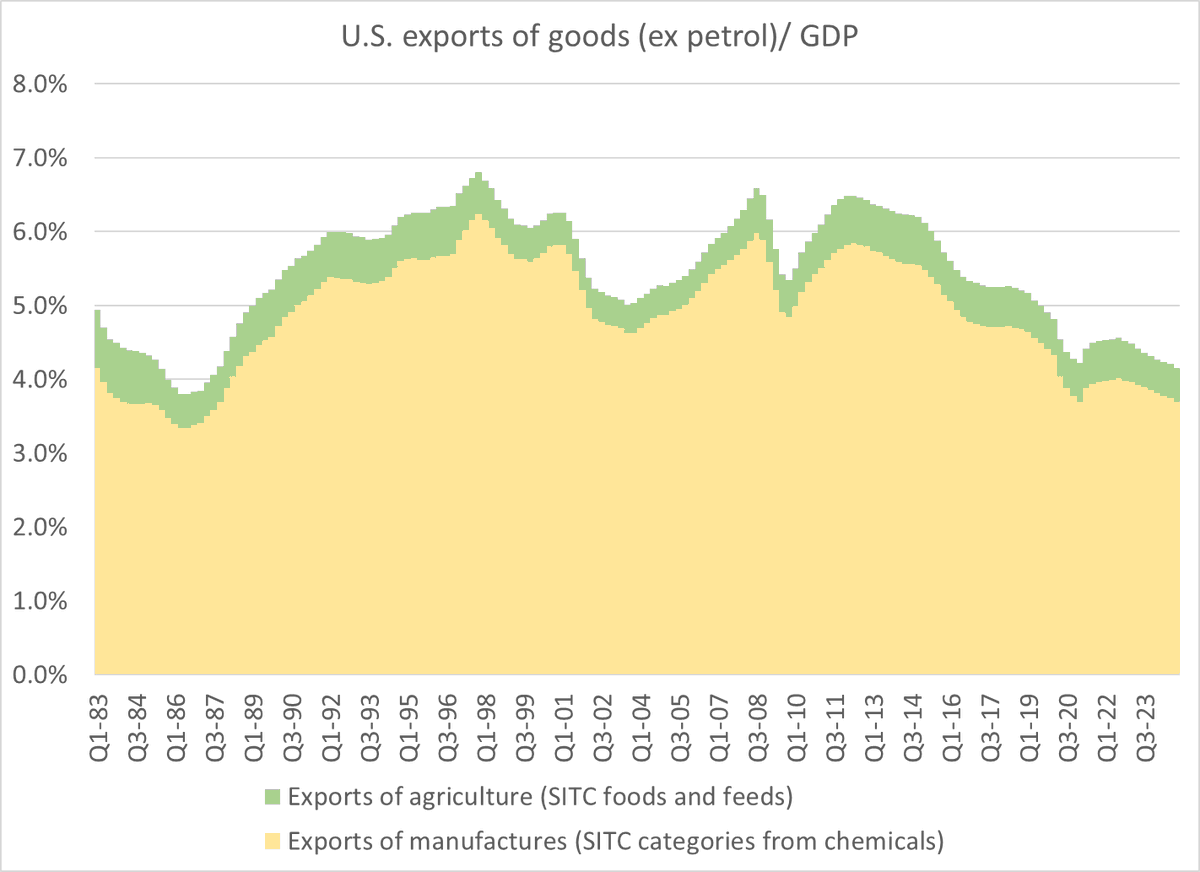

The current account deficit is about equal to US manufacturing and ag exports (using the SITC definition) 6/

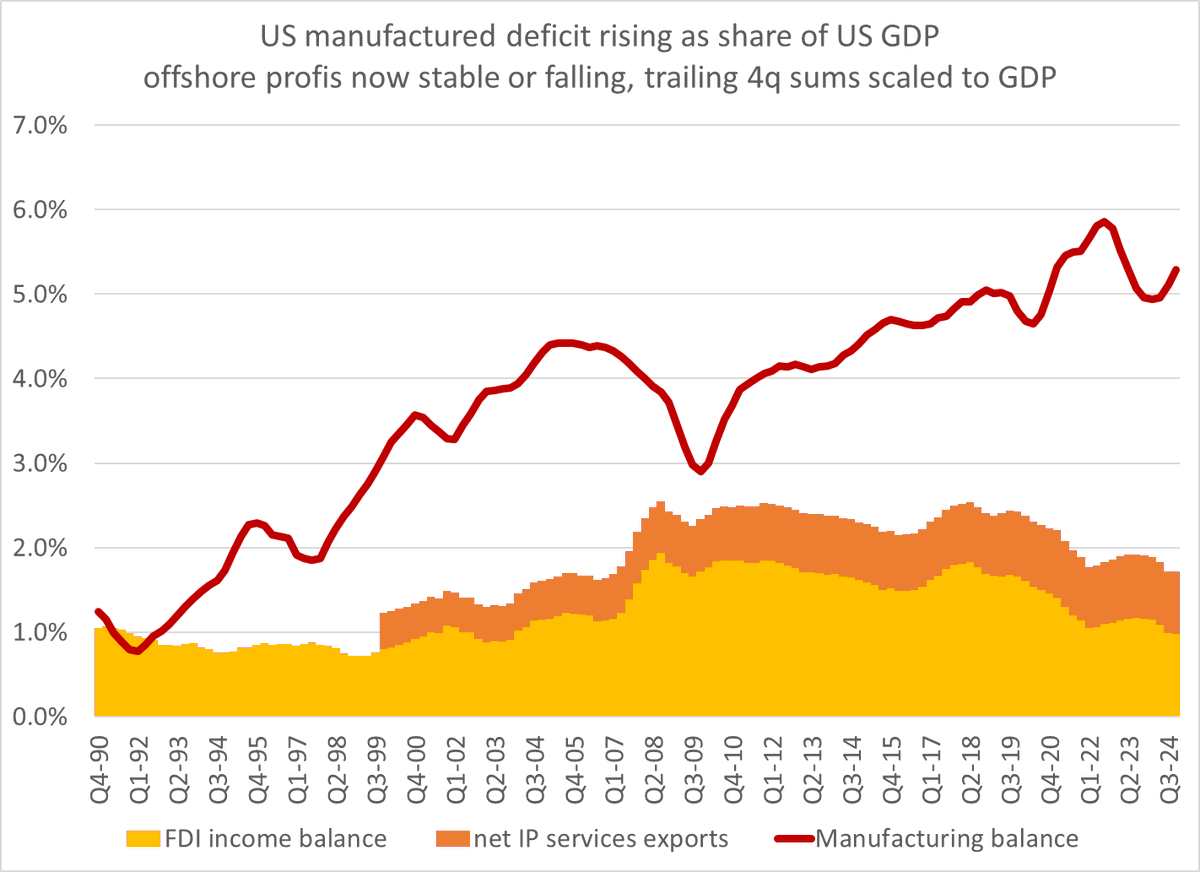

Adding in the "intangibles" export base (net FDI income , which essentially is all in the world's tax havens and IP related services exports) doesn't change the story much, as those sources of foreign earnings have also shrunk as a share of GDP 7/

So the current account deficit has gotten to be large absolutely, and large relative to the United States sources of external earnings - and that deficit is now financed by large private inflows. Reserve growth has dried up 8/

the net result, as James Aitken highlights, is that the financing of the US external deficit was a function of the "American exceptionalism" trade 9/ https://www.aitkenadvisors.com...

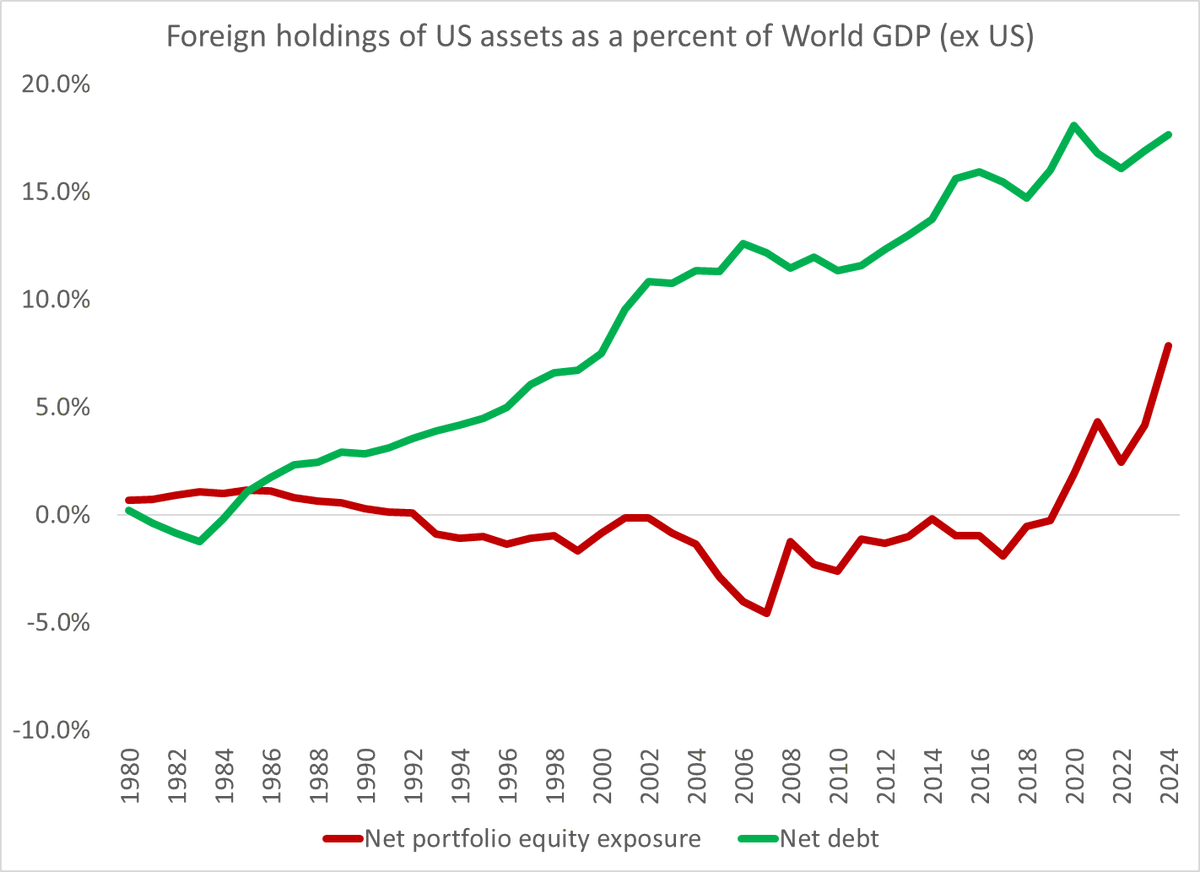

It isn't enough though for the world to just hold on to their existing exposure -- to fund the US external deficit they needed to keep adding to it ... US external debt wasn't rising v US GDP (which was inflated by the strong dollar) but it was rising relative to WGDP 10/

The dollar doesn't need to lose its central position in the global financial position for it to fall -- it just has to start to be a bit less exceptional (a self induced recession will do that ... ) relative to other financial assets globally 11/

Another way to think about the risks is that the world has been running a big carry trade, holding say US corporate bonds against yen liabilities or as part of a European pension portfolio ... 12/

And when carry trades unwind, the "destination" currency tends to fall -- which would explain how US bond yields could rise/ bond prices fall while the dollar also fell ... 13/ https://www.nytimes.com/2025/0...

Put differently -- the risks around the US aren't limited to a loss of confidence in US fiscal policy. The underlying BoP position has started to weaken + there are a lot of "stale" dollar/ US asset longs that were premised on a world and US that is no more 14/14