Last week, I presented orally at a hearing of the U.S.-China Economic and Security Review Comission on China's efforts in the clean energy transition, focusing on industrial electrification. Testimony and recording in link. This is a summary thread. 🧵 https://www.uscc.gov/hearings/...

China has already achieved dominance of the current "big three" pillars of cleantech: solar PV, batteries, and EVs. To these, add wind turbines and ultra high-voltage transmission, and China's 2030 carbon emissions peaking target seems quite assured. But what then?

Yes, the emissions peak is mathematically inevitable, with both coal consumption and petroleum consumption having already peaked, or about to peak, depending on to whom you speak. But what must happen post-2030 to ensure the peak turns into a decline, and not just a plateau?

And furthermore, how does the objective to decrease emissions square with the importance of energy-intensive heavy industry in the Chinese economy...segments like steel, aluminum, chemicals? Demand for these products isn't going anywhere.

The answer, as I present in my testimony, is the next big battlefront of industrial cleantech: process decarbonization. I propose the "new big three", which will be industrial electrification, process applications for green hydrogen, and carbon capture & sequstration (CCS).

And if we're being precise, there are actually ALL about electricity. No matter whether the power is used for direct electrification of heat applications, used for electrolysis of hydogren, or used to run CCS, more electricity consumption is integral to industrial decarbonization. That's part of why outlooks for Chinese power consumption show constant power consumption growth pretty much all the way out to 2060, even though total energy consumption peaks sometime in the early 2030s.

Now, it must be acknowledged that while the engineering theory foundations for these electrified applications are sound, they are all horribly uneconomical now vs the the fossil-fuel powered applications they replace. I'm not gonna sugarcoat it - they can be VERY expensive.

But that isn't stopping Chinese firms from building them anyway - naturally with huge backing from the state to derisk the efforts of these bold pioneers. Theoretical research gets you from 0 to 1, but demo projects, iterations, and scale will get you from 1 to 10, 20, 50, 100.

For almost every next-gen heavy industrial process decarbonization technology, China already has a demo project, or two, or five, starting up somewhere in the country. In many cases, EU firms are matching Chinese efforts, albeit with less scale. The USA is almost a no-show.

I see examples of Chinese power-based decarbonization demo projects across segments as diverse as steel, silicon, ethylene, methanol, ammonia, cement, glass, and aviation fuel, all deploying now. Sometimes multiple competing pathways at the same time. https://x.com/pretentiouswhat/...

For instance, in steelmaking, the fossil-fuel dependent blast furnace process (BF-BOF) could be swapped for electrified Direct Reduction Iron (DRI) with hydrogen as a reduction agent. OR you could co-fire with green hydrogen in the blast furnace. THEN you could apply CCS to either pathway. Chinese steelmakers have different national-level demonstration project for virtually every combination of the technologies mentioned above. Will they all stick the the landing? Of course not. Some of them will be just too expensive, too hard, too inefficient. But they'll give them all a fair shot, and then the one that shows the most promise is the pathway that will be chosen to optimize, iterate, and improve over the next decades. If they could do it for solar PV, I believe they can do it for green hydrogen or CCS. Crucially, the (usually state-owned) companies that try and fail will NOT be risking the farm on these projects. When you carry out technology demostration projects in support of national mandates, you know the state has your back.

Long story short, for key industrial decarbonization tech post-2030, Chinese companies and energy stakeholders are recreating the same conditions that allowed them to dominate the critical cleantech of the pre-2030 era. Only this time, they'll be doubling, tripling down on electricity, stacking up exposure to domestically-produced energy while trimming exposure to imported energy. The economic and security advantages will be tremendous.

In this way, China will continue to be a major heavy industry player in the coming decades, and with deployment and scaling of these process decarb techologies, they won't even have to sacrifice their climate goals to do it. Mencius gets both his fish AND his bear's paw.

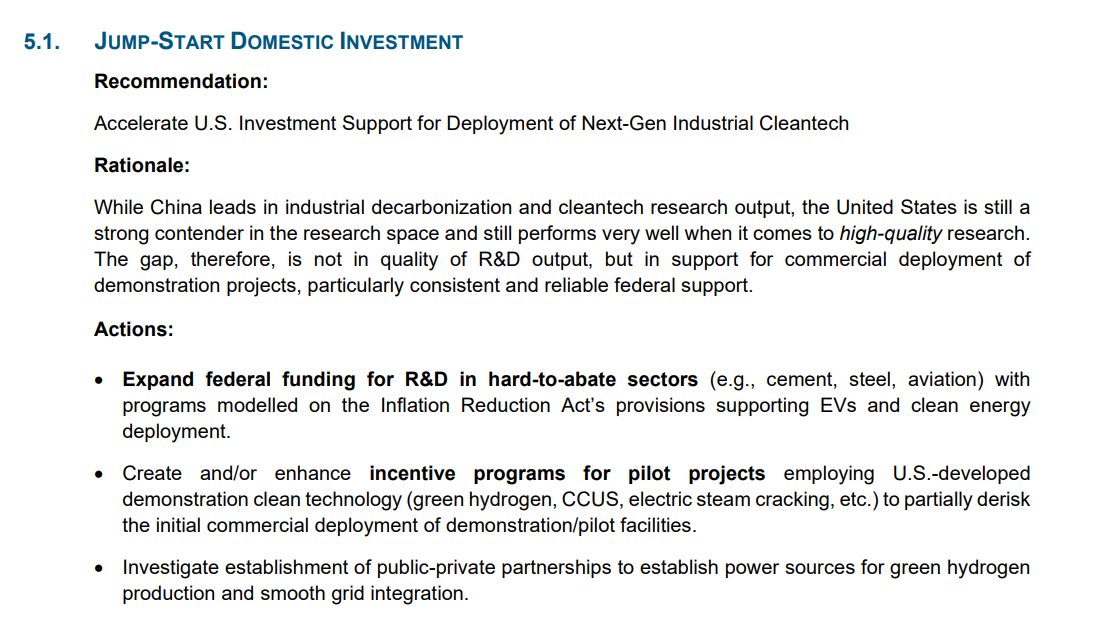

In my testimony, I advise US policymakers they have three options vis a vis China and next-gen cleantech: collaborate, compete, or concede. Of course I prefer the first. I can respect the second. The third should be a non-starter.

I provide recommendations for US policymakers that should be relevant, no matter when they choose to collaborate or compete. Dunno how realistic these are in the current geopol climate, but I have to try.

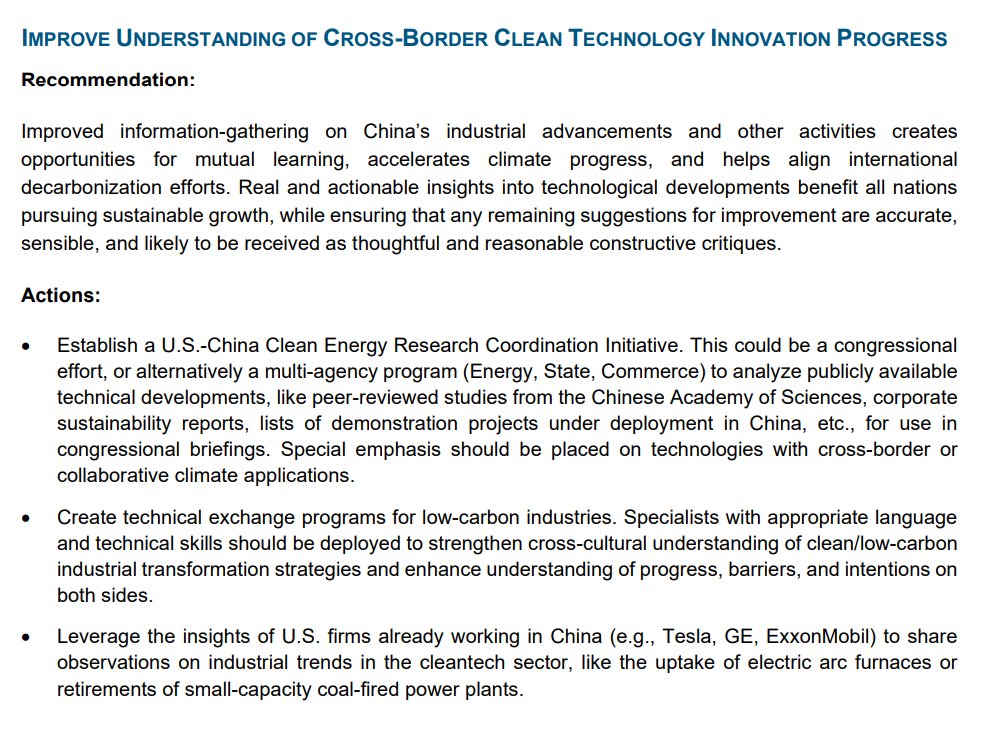

My final recommendation speaks directly to a theme I've been harping quite a bit recently: if the US wants to compete, it'll need to get a lot better at learning what China is up to by doing more homework and talking to the right people.

This topic is massive, and I know I barely scratched the surface with my testimony. Unfortunately I didn't have a year to write, but just a few weeks, so there are many gaps. I encourage anyone interested to please keep going deeper with it. And thanks for your attention.