I'm a sucker for stories about how corporate hedging flows cause massive pain for dealers and affect the spot-vol dynamic and the vol surface. Recently, we've seen a dynamic like this in no less than the most liquid FX market - the EURUSD, so I thought it worthwhile digging in

Our story begins with a little-known company - Safran. Now, don't feel bad if you've never heard of them. They are in the aerospace business, yet they are HUGE. This multinational company is one of Europe's biggest exporters, so they have serious hedging needs.

However, they can't just buy a ton of EURUSD spot to hedge their 5-year projected USD cashflows because, well, it will create a cashflow mismatch. So, they have to use FX derivatives, and more specifically, a strip of FX forwards. Clearly, this is where banks see $$$

Banks understand their need for a long strip of FX forwards and package them in a weird structure called Target Accrual Redemption Forward (or TARF), which is essentially a bunch of forward contracts with a chunky embedded option, skewed in the bank's favor

The basic mechanics of TARF are rather simple: periodic fixings against a predefined "enhanced" rate, in which the buyer (Safran) accrues P&L until it reaches the target P&L. This is where things get more complicated -To get an enhanced rate, the P&L is asymmetric

There are a bunch of clauses that allow the bank to offer this structure at zero upfront cost. For example, in a common TARF, the client has a 2x leverage on OTM fixings, so they lose twice for OTM fixing relative to ITM fixing, and usually, there are Knockout barriers

to "enhance" the strike rate, in addition to the early termination clause embedded (as the structure will terminate either when the target is reached or at maturity, whichever comes first). Now, anyone with some understanding of how derivatives work thinks of path dependency

And in the derivatives world - path dependency == massive optionality and vega And whoever thinks that is absoultely 100% right. So, whenever Safran's CFO (or whoever carries their hedging business) calls banks for a quote on the structure, they know one thing - SELL VEGA

Banks understand that this structure supplies them with massive vega (they are usually 1y-2y structures) exposure, and they know that once these structures are traded (with whoever wins the deal), someone will have to sell a shitload of vega to maintain their risk limits

Now, you can call it frontrunning (which is precisely what it is), but banks won't tell you that; they will simply say that it's getting ahead of the flow. Once this flow hits the market, backdated vols are already notably lower than before. Now the market is driven by spot path

As I said before, this structure introduces a massive path dependency due to all the early termination clauses (which is why banks hire a bunch of French quants and some sophisticated MC engines to price them and their risk), and banks constantly scratch their heads about greeks

Generally, banks are "locally" long vega (and gamma) around the strike rate, long some skew (usually for ITM/RKO barriers), but as spot moves (usually rapidly) away from the strike, they lose their vega, the odds of early termination rise, which makes them short convexity

Now, you'd think that banks would like this trade to be knocked out as early as possible, but because of the way banks hedge their exotic books, the worst thing for them would be massive moves that knock trades out, leaving them exposed, needing to buy back vega/delta/gamma

Anyway, the current pain in the EURUSD market started around late June, when most European money managers/hedge fund traders/whoever sells options went on their summer holiday. The USD has generally been on a downtrend this year, with the EUR being one of the main beneficiaries

Entering July, the EUR has already started creeping higher, and noise around Tariffs/Powell/US data only added to the market's love affair with the idea of topside EUR. When dealers ran their spot ladders, they saw quite a nasty exposure, which got them spooked

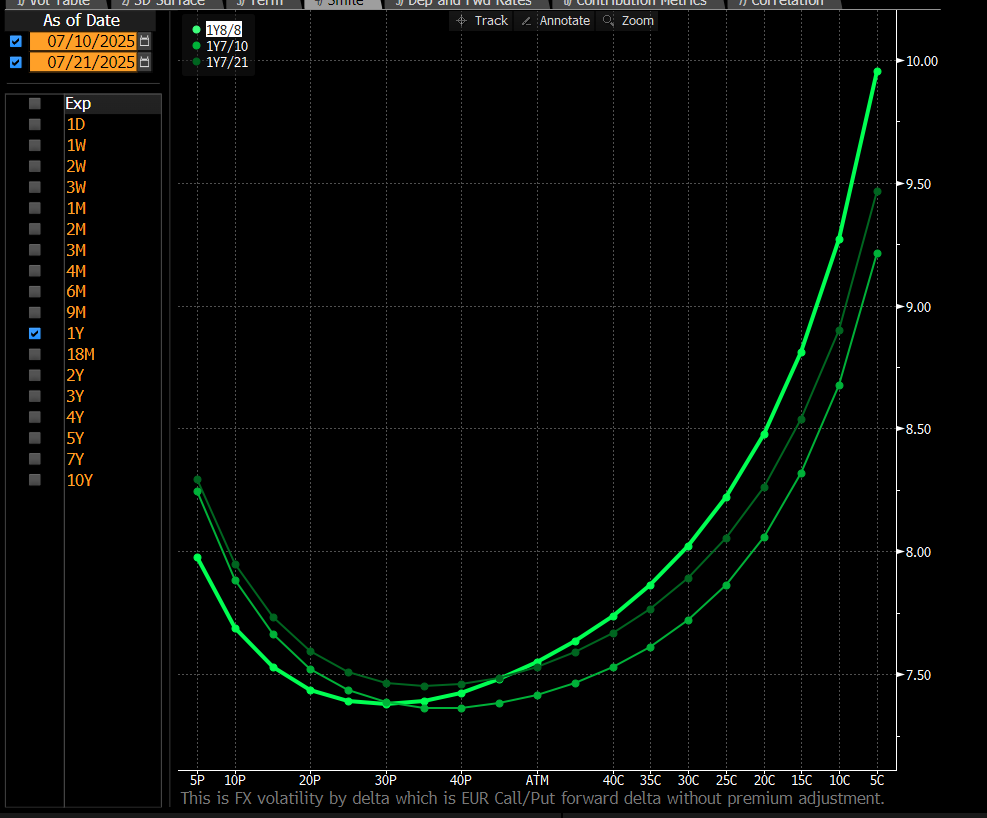

These massive TARF structures, in a summer/illiquid market, when nearing some level (my best guess is 1.2s in EURUSD), make your risk team lose sleep at night, refreshing the Bloomberg every 5sec. One good evidence for that dynamic is the fixed-strike stickiness

Usually in FX, fixed-strike vols tend to "roll under" the delta strike vol, or in other words, if one sells a 25-delta option on the expensive side of the smile, they expect that vol to roll under as spot moves towards the strike (and it gets closer to the money)

This has hardly been the case lately. Despite being exactly at the same level a few times in July/ early August, the backdated smile kept on repricing higher (driven mainly by an endless bid to skew)

Not to mention the extreme spot-vol beta, and the sensitivity of the ATM vol curve to the level of EURUSD (not just the size of the underlying move), due to the massive Vanna position the market is carrying, and the lack of supply.

This entire dynamic landed itself into a massive pain trade for EUR vol desks, which collectively have to run a gigantic short vanna position, and feed into this reflexive bid for vega, vanna, and volga, and it doesn't seem to go away anytime soon

For any vol nerd, like myself, exploring the effect of flows and positioning on the vol surface and its evolution is a fascinating dynamic. So, how does this feedback loop play out, or how does this loop break?

Usually, such a dynamic breaks down due to one of three reasons: 1. An external factor pushes the spot away from the painful region towards long gamma/long vega region and vols selloff 2. The market is getting supplied with vega, skew, and convexity, usually by hf traders

3. Barriers are taken out -> vol explodes -> banks buy a ton of vega back -> FX vol RV players use it to enter short vega/skew at good levels -> market digests the flow -> spot finds a new equilibrium -> vols collapse I'm rooting for the third option, but I'm biased

My point - behind vol surface moves there are many moving parts that are not found in the raw numbers we see on our bloomberg terminal, and cannot be taught by textbook derivatives theory (or academic literature)

@OneHotCode1 Think EADS is creating more of that than SAFRAN, they are the biggest eurusd buyers in all Europe much much bigger than safran

@0xAmSS perhaps, but every bank i've been talking to over the last few years only cares about what Safran are doing