"Renting is a huge waste of money!" You've heard this before, but it's not true. Here's the real math behind buying vs renting:

Analyzing buying vs renting comes down to a simple idea - recoverable vs non recoverable costs. Every expense, whether you own or rent, falls into one of these two buckets.

For example, property taxes or rents are non recoverable. You’ll never get back this money. Paying down the equity portion of your mortgage is recoverable. So, if you're planning to buy a house, live in it for 5 years, what should you do?

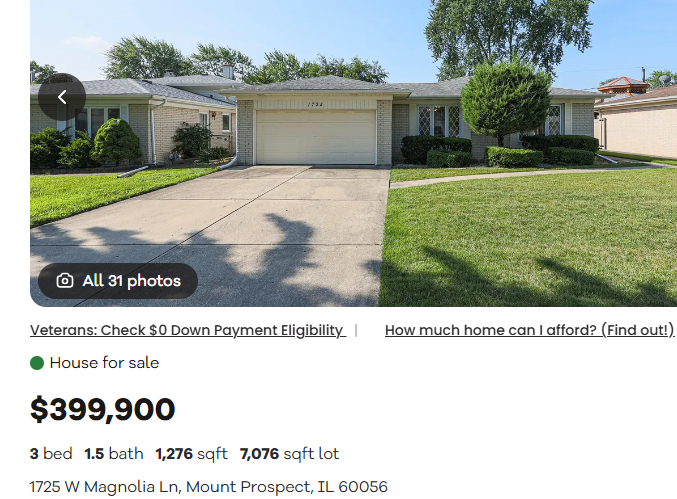

I found this home in Chicago suburbs for sale for $399k:

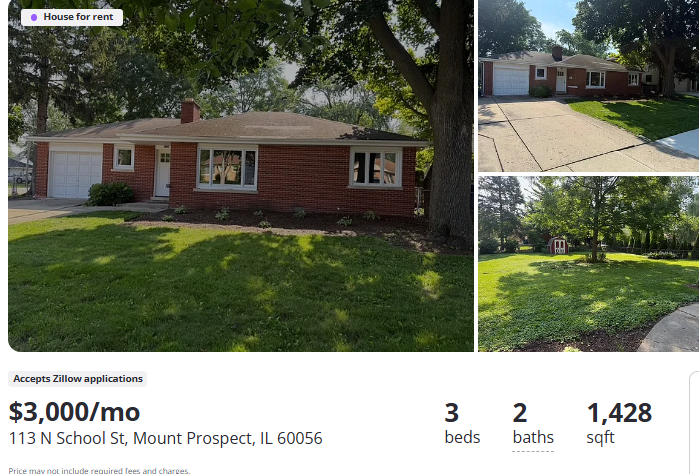

I did my best to find a comparable rent with same sqft and bed/baths in the area. It's going for around $3k/mo.

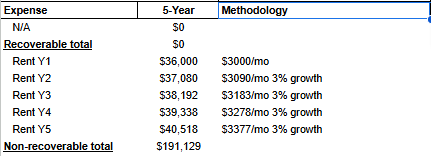

When renting, your only unrecoverable cost is the rent (some might need to add renters ins). There is no other benefit you receive in exchange for rent payments. 5 years of renting would cost $191,129 with a 3% rent growth per year:

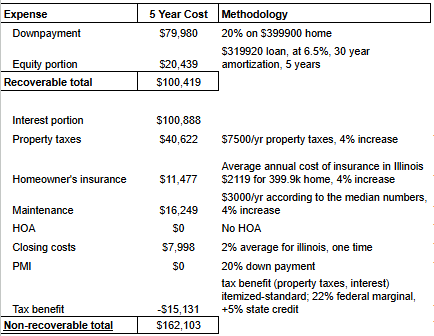

For buying: Your recoverable costs are the down payment and equity. The non recoverable costs are interest, property tax, homeowner's insurance, maintenance, closing costs, and PMI, minus the tax benefits

Let’s say you put a 20% down payment to buy the house. Currently, rates are high, and I'm calculating using a 6.5%. Here’s what 5 years of buying would look like:

After 5 years, you will spend $100,419 in recoverable costs and $162,103 in non recoverable costs, for a total of $262,522. If the home appreciates at 4% per year, it will be worth approximately $486,539.

When it’s sold, you will pay off the mortgage balance of $299,480 and a 6% selling cost of $29,192. You will walk away with $157,867 tax free. NET cost of homeownership will be $104,655, calculated as $262,522 (your total $$ payments) - $157,867 (your $$ recovery after sale)

When renting, we can also invest the initial down payment amount ($79,980) and the buying closing costs ($7,998) in the market for 5 years. With an 8% yearly growth assumption, you'd have ~$129,268.55, with $87,978 as the contributions.

Since we are calculating net of tax, you'll pay LTCG tax of ~15% on appreciation, your net is $123,074. The net total cost of renting would be $68,055 ($191,129 - $123,074) So, renting would be cheaper by $36,600 over 5 years, or $7,320/yr.

BUT we only compared rent vs buy for 5 years. If we extrapolate the numbers over 10 years, owning a house is better by $69,885 than renting, or ~$6,988/yr. This makes sense, as buying becomes better over the longer timeframe (usually at around 8 year mark)

TLDR: 1. The longer you stay, the better buying looks 2. Numbers vary significantly by location 3. Higher home price vs rent = worse for buying (i.e. buying $1.3M home in CA vs $4,000 rent) 4. Interest rates (lower rates can make buying better) 5. What are your goals? Not

If you enjoyed this thread, I would really appreciate it if you could help spread the message by: 1. reposting 2. sending this thread to a friend or family 3. following me @money_cruncher for more personal finance tips

@money_cruncher The problem is you’re at the mercy of the landlord to raise rents.

@money_cruncher Would a landlord allow me to cut a hole in the side of the house for a doggie door so the dogs can relieve themselves and get exercise while I’m at work? What’s that worth?

@money_cruncher My convictions is that you buy when you'r eplanning to live their for more than five years. Less than five years, then renting is a better option.

@money_cruncher It's a huge waste of money

@money_cruncher The best part about owning a home for most people- It's a forced savings account. You can put zero down (if you qualify). And 30yrs later your home would have tripled in value and you'll have no loan payment. (doesn't work that way with renting)

@money_cruncher I mean dude home values can go up or down

@money_cruncher Good analysis. I've done both and currently own but it's not a money thing, it's a freedom thing--to make the space my own. There's a savings from interest deduction but that can easily be offset by repairs and maintenance which are mostly non-recoverable

@money_cruncher Two other surprise cost risk factors: Owning: do you live in a financially irresponsible city that could randomly double property tax? Same with HOA. Renting (US): is your landlord selling and wanting you to leave at lease end (or before with just a few months notice

@money_cruncher Renting and buying are tools that work in individual circumstances. My first purchase was a duplex a few years out of college. The power of utilizing the purchase of a home while having someone else pay your mortgage and reaping tax benefits is not championed enough.

@money_cruncher Great analysis. I get so annoyed when people ignore the opportunity cost of the down payment. I know most people don’t save and invest, so the mortgage as a “forced” investment vehicle actually makes sense. But for people like myself who want to maximize how hard each dollar I

@money_cruncher Home ownership is the best long-term hedge against inflation. You don’t want to rent when you retire, because your health care premiums will take a good part of your income.

@money_cruncher is a cost of opportunity problem

@money_cruncher Totally agree, but there are deals to be had. We run the numbers like this all the time ! Pro formas shine here

@money_cruncher buy crypto tech stocks and pay rent

@money_cruncher Don’t care. Can afford it and another person will not tell me on a yearly basis if I need to move or not. Y’all discount the http://know.security of a roof over your kids heads like it’s a line item.

@money_cruncher Your math is only true for some scenarios. In Seattle a property worth 700k cost 5k a month mortgages but only 3k to rent. Extra 2k goes into pocket

@money_cruncher Well said! Sunk costs + opportunity costs - I agree that for the short-term rental is a better option. The closing costs on both sides of the transaction eat a year's or two worth of returns when you own a home as well.

@money_cruncher Put that down payment and closing cost $ into Bitcoin, and renting will forever be the right financial decision, no matter any other factors.

@money_cruncher If you have no ego, renting is great

@money_cruncher Problem is the renter, in many cases, likely isn’t investing their down payment funds diligently. The homeowner has no choice but to repay a portion of their principal each month. Real world might look a lot different than the hypothetical scenario presented.

@money_cruncher Good content

@money_cruncher Renting buys you flexibility and freedom.