Banks’ investments drive earnings & book value. But how they’re classified under IFRS 9 makes a BIG difference. Today: FVTPL vs FVOCI — using Habib Bank Ltd (HBL) June 2025 financials. #HBL #CommercialBanks #KSE100 #PSX

🔎 First, the categories: FVTPL = Fair Value Through Profit & Loss FVOCI = Fair Value Through Other Comprehensive Income Both are at fair value, but income recognition differs. #HBL #CommercialBanks #KSE100 #PSX

👉 Why does it matter? Because: FVTPL flows into P&L → EPS → Dividend FVOCI flows into OCI → Equity → BVPS Same security, different impact. #HBL #CommercialBanks #KSE100 #PSX

⚖️ IFRS 9 Logic: FVTPL: Used when assets are held for trading/short-term gains. FVOCI: Used when assets are held for collecting cashflows + selling. This is called the business model test ✅ #HBL #CommercialBanks #KSE100 #PSX

🎯 Mathematical View: If FV = Fair Value today AC = Amortized Cost ΔFV = Change in Fair Value Then: FVTPL Impact: P&L (t) = P&L(t-1) + ΔFV FVOCI Impact: OCI (t)=OCI (t−1)+ΔFV (t) #HBL #CommercialBanks #KSE100 #PSX

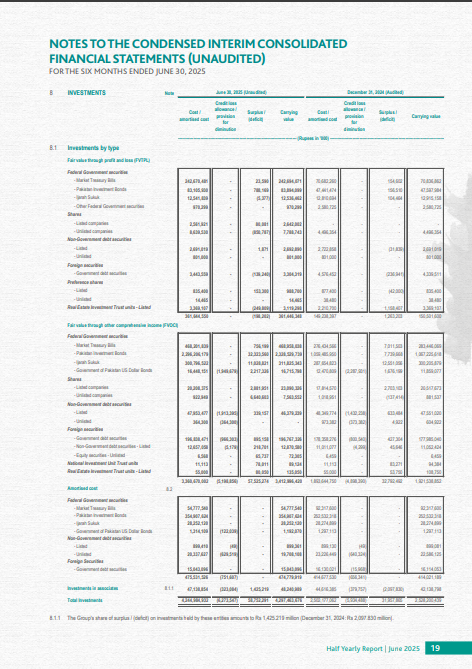

📊 Example HBL (June 2025): FVTPL portfolio: PKR 361.4bn FVOCI portfolio: PKR 3,412.9bn So most of HBL’s book is FVOCI, not FVTPL. #HBL #CommercialBanks #KSE100 #PSX

🔵 FVTPL: Federal Govt Securities (MTBs, PIBs, Sukuk) + listed shares. 🔴 FVOCI: Huge portfolio of PIBs, Sukuk, T-bills, GOP USD Bonds, listed shares. #HBL #CommercialBanks #KSE100 #PSX

💡 Recognition Difference: FVTPL gain/loss → Income Statement FVOCI gain/loss → Other Comprehensive Income (OCI) EPS vs BVPS game. #HBL #CommercialBanks #KSE100 #PSX

🧾 Example – HBL’s listed shares (FVOCI): June 2025: Surplus PKR 2.88bn Dec 2024: Surplus PKR 2.70bn This increase (≈ PKR 0.18bn) didn’t hit EPS. It boosted Equity reserves. #HBL #CommercialBanks #KSE100 #PSX

🧾 Example – HBL’s PIBs (FVOCI): Surplus June 2025: PKR 32.3bn Surplus Dec 2024: PKR 7.7bn Gain of PKR 24.6bn in 6 months — but again → only OCI. #HBL #CommercialBanks #KSE100 #PSX

🧾 Example – HBL’s PIBs (FVTPL): Surplus June 2025: PKR 0.79bn Surplus Dec 2024: PKR 0.15bn This gain flows directly into June 2025 earnings → lifts EPS. #HBL #CommercialBanks #KSE100 #PSX

💰 Formula impact on EPS: EPS= Net Income+ΔFV (FVTPL) / Shares Outstanding FVOCI changes don’t appear in numerator. #HBL #CommercialBanks #KSE100 #PSX

💰 Formula impact on BVPS: BVPS=Equity+Surplus (FVOCI)/Shares Outstanding Here FVOCI matters a lot. #HBL #CommercialBanks #KSE100 #PSX

📌 HBL Numbers: Equity (June 2025): PKR 448.7bn FVOCI Surplus: PKR 57.5bn So ~12.8% of equity is FVOCI-driven. #HBL #CommercialBanks #KSE100 #PSX

🚨 Investor insight: EPS stability depends more on NII & FVTPL, while Book Value is very sensitive to FVOCI mark-to-market. #HBL #CommercialBanks #KSE100 #PSX

🔍 Cash Flow Impact: Neither FVTPL nor FVOCI gains = real cash. Only realized on sale/maturity. But accounting treatment changes perception of strength. #HBL #CommercialBanks #KSE100 #PSX

💡 HBL Dividend Policy: Dividends come from retained earnings → tied to EPS. So only FVTPL gains feed dividends, not FVOCI. #HBL #CommercialBanks #KSE100 #PSX

📊 Analyst takeaway: HBL’s huge FVOCI book means: EPS might look “stable” even if bond prices move. But BVPS could swing widely → affecting P/BV valuation. #HBL #CommercialBanks #KSE100 #PSX

⚖️ Pros of FVTPL: Transparency in earnings. Immediate reflection of market moves. Better for trading book. #HBL #CommercialBanks #KSE100 #PSX

⚠️ Cons of FVTPL: Higher EPS volatility. Noise from unrealized gains/losses. Dividends may be artificially boosted by temporary gains. #HBL #CommercialBanks #KSE100 #PSX

⚖️ Pros of FVOCI: Smooth EPS (stable dividends). Equity reflects long-term fair value. Preferred for bond-holding banks like HBL. #HBL #CommercialBanks #KSE100 #PSX

⚠️ Cons of FVOCI: Earnings hide market volatility. Investors may underestimate risk. Book value swings harder → affects P/BV ratios. #HBL #CommercialBanks #KSE100 #PSX

🧮 Quick Calculation – HBL P/BV (June 2025): Equity = PKR 448.7bn Shares = 1,466.8m BVPS = 305.9 At share price 254.35 → P/BV = 0.83x #HBL #CommercialBanks #KSE100 #PSX

But without FVOCI surplus (strip out PKR 57.5bn): Equity adj. = 391.2bn BVPS adj. = 266.7 P/BV adj. = 0.95x #HBL #CommercialBanks #KSE100 #PSX

So investors should ask: 👉 Is HBL “cheap” at 0.83x, or actually “fair” at 0.95x after excluding FVOCI noise? #HBL #CommercialBanks #KSE100 #PSX

📉 Stress Scenario: If interest rates rise, FVOCI surplus can fall. That means: EPS stays same Equity shrinks → P/BV multiple rises artificially. #HBL #CommercialBanks #KSE100 #PSX

📈 Opposite Scenario: If rates fall, FVOCI surplus expands. Book value jumps → P/BV looks cheaper → upside for investors. #HBL #CommercialBanks #KSE100 #PSX

🔔 Core Message: Always break down HBL’s EPS drivers: 👉Core NII 👉FVTPL gains vs Book Value drivers: 👉FVOCI surplus #HBL #CommercialBanks #KSE100 #PSX

📌 Practical Investor Tip: Don’t just look at EPS. Track: OCI movements FVOCI surplus % of equity P/BV adjusted (ex-OCI) #HBL #CommercialBanks #KSE100 #PSX

🎯 Final Word: For HBL, huge FVOCI book means book value volatility is bigger risk than EPS swings. Smart investors track both sides of IFRS 9. #HBL #CommercialBanks #KSE100 #PSX

@MeherJazibAli Good analysis, but try to make it simpler and easier to understand for a layperson. A common investor doesn't need to understand any such values or indicators as long as he is concerned with what to buy, how to buy, and how much gain it will give.

@Hasnat_Yusufzai Thanks. For sharper decisions, you need to understand the details. Otherwise, you’ll end up paying others to make choices for you. And if you’re only here for buy/sell calls and % gains, then this isn’t the right place. Continuous learning is essential for investing.