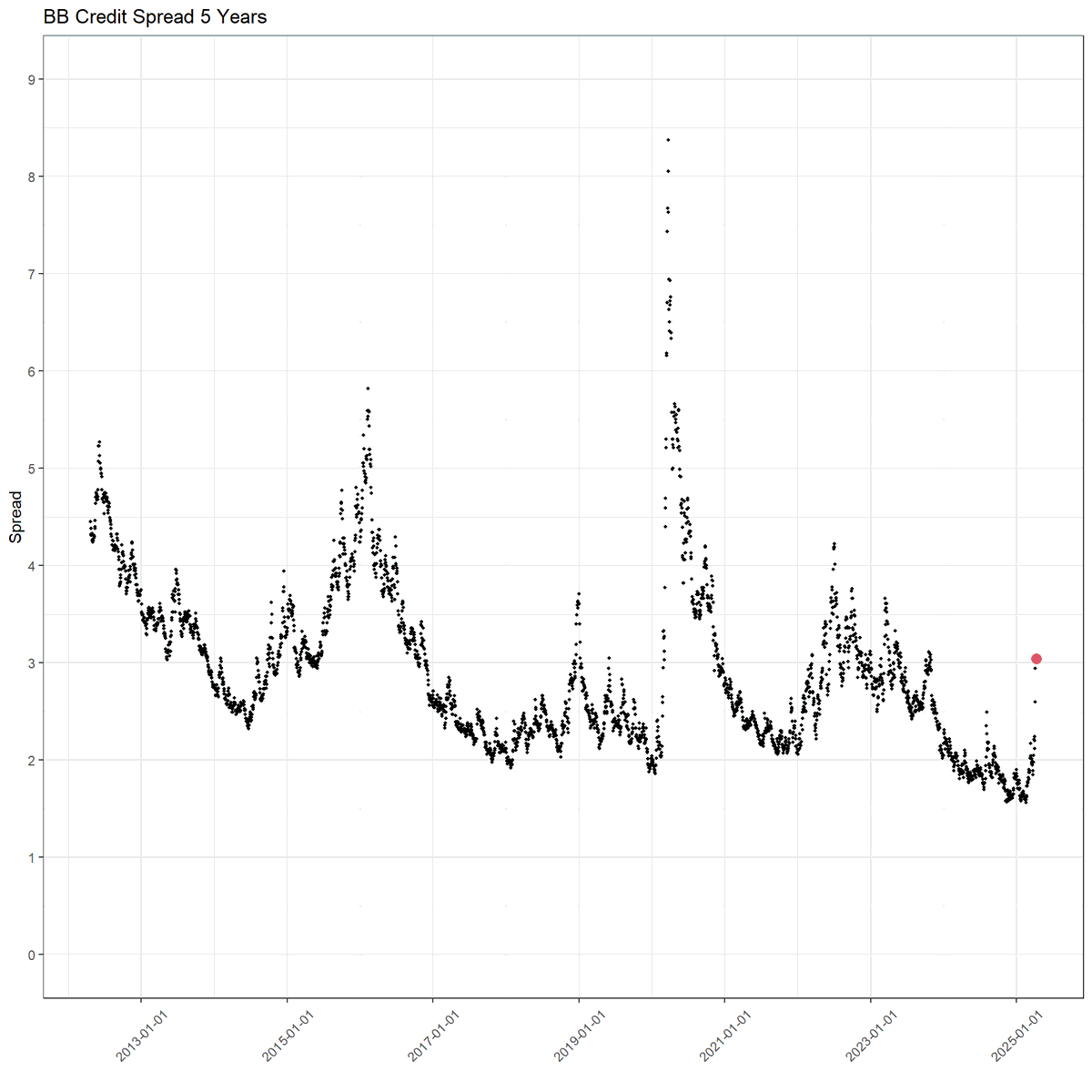

lot of mention now that credit spreads foreshadow a recession despite large rally yesterday. this is wrong. fixed income rates and spread wider or tighter, higher or lower do not correlate to the economy change and thereby market levels

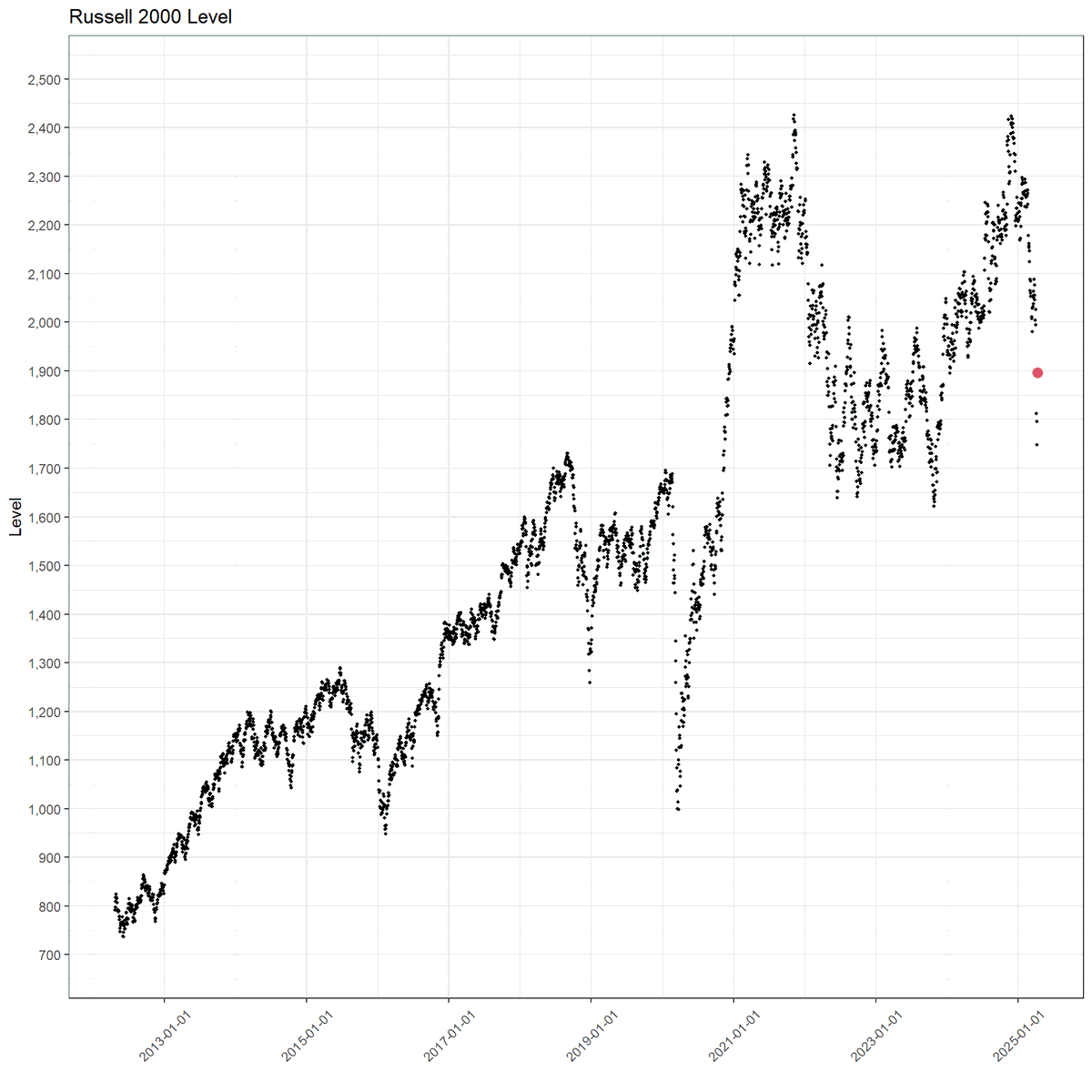

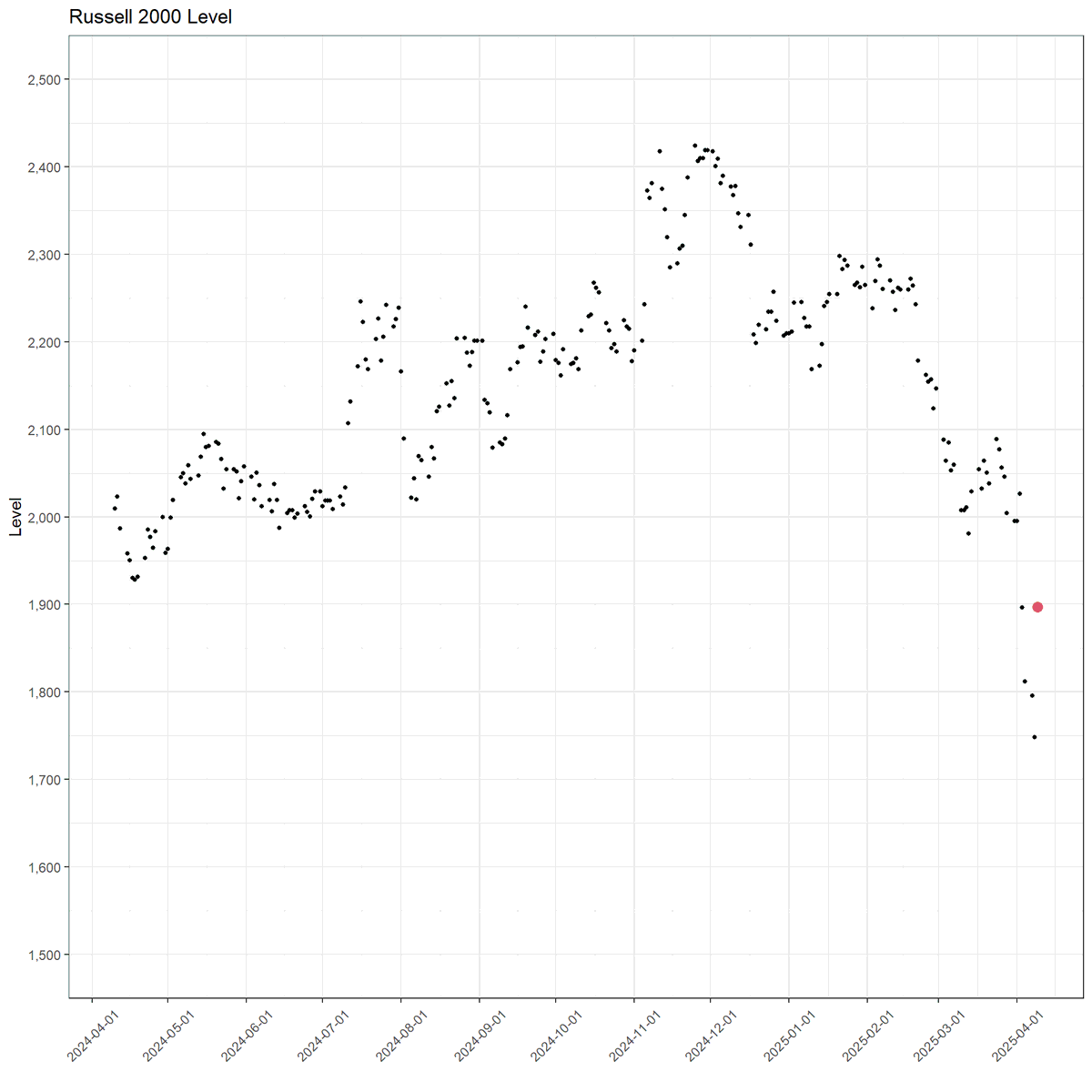

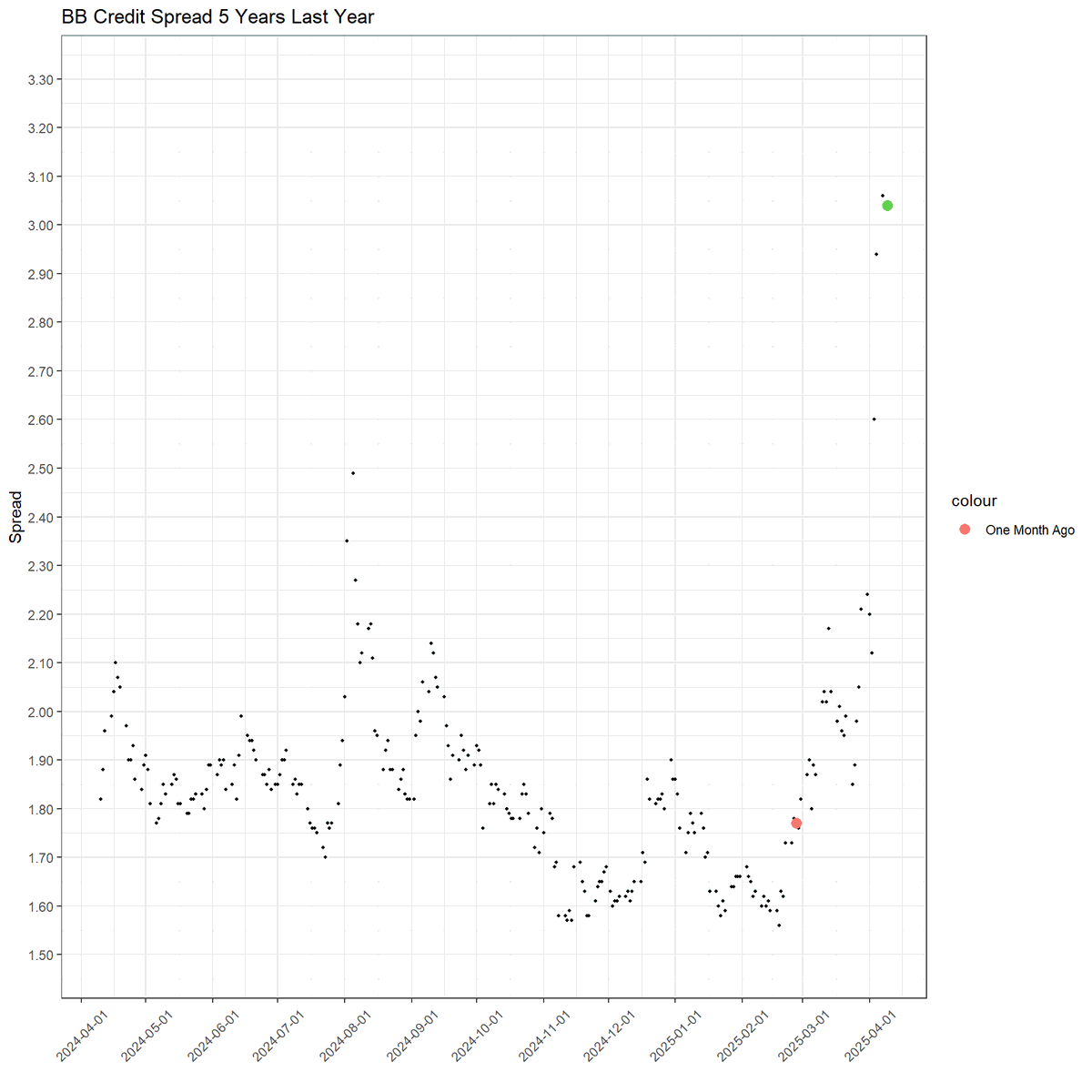

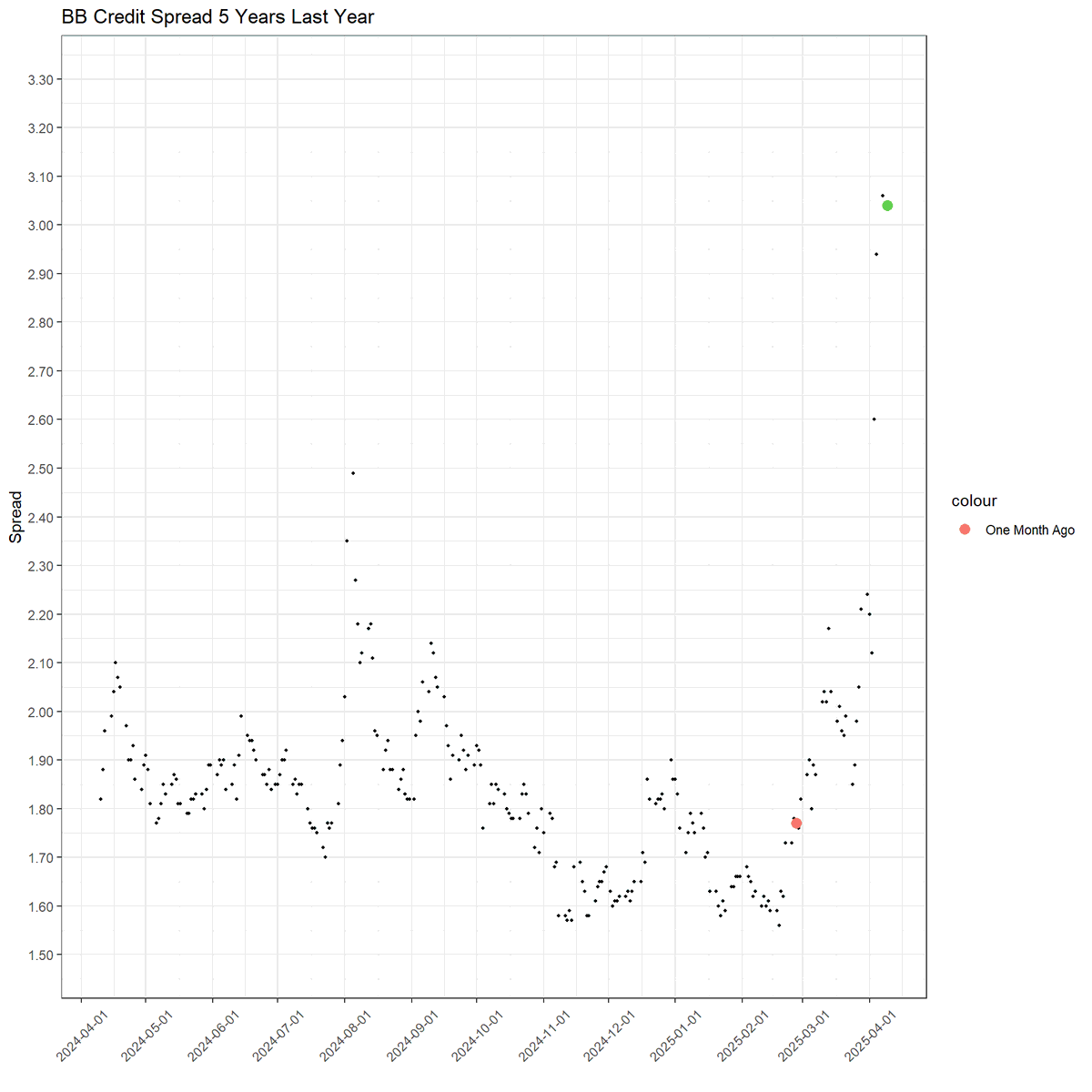

yes the R2K is down significantly last couple of months and did have a partial but small recovery yesterday. credit spread BB did not come in only stayed unchanged. this is thought to be sign yesterdays rally will not last.

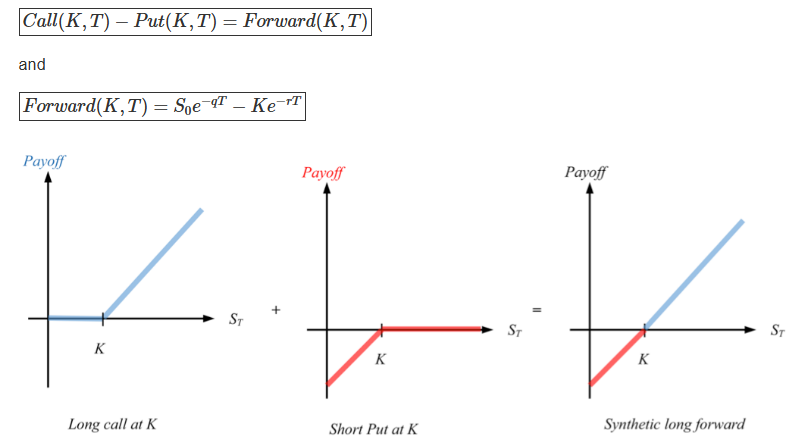

this has little information comparing credit spread to price level. credit spread is an option problem, the premium bond holders receive for the short put that bonds are in the asset value - will the equity is a long call. combined they are the ongoing asset value.

the combo of short put and long call is the straight lines, here showed at "expiry" and current values being lower equal to the premium from the short put.

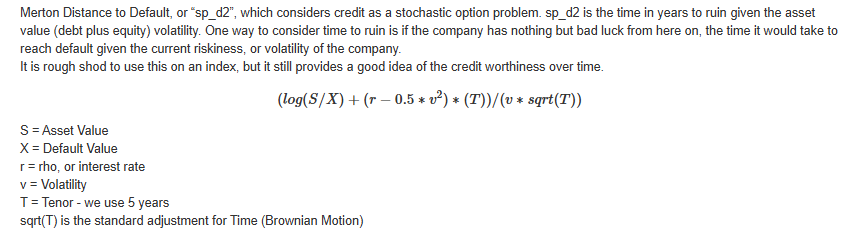

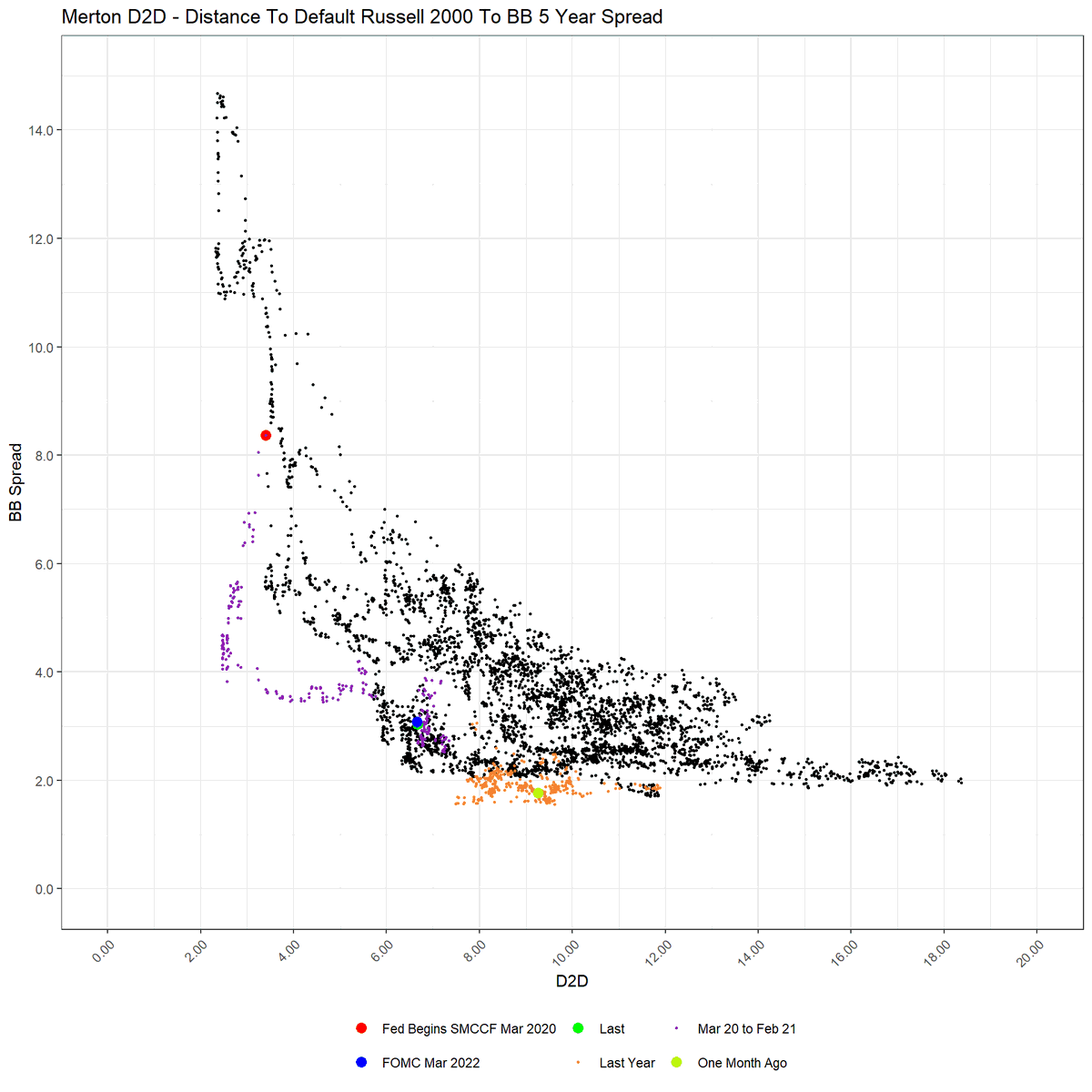

the way to qualify is to use the formula "d2" in option math and in credit markets termed called "distance to default" (D2D). dont get too hung up on the math just note it is trying to qualify the spread or distance between current price (S) and strike (X) or default value.

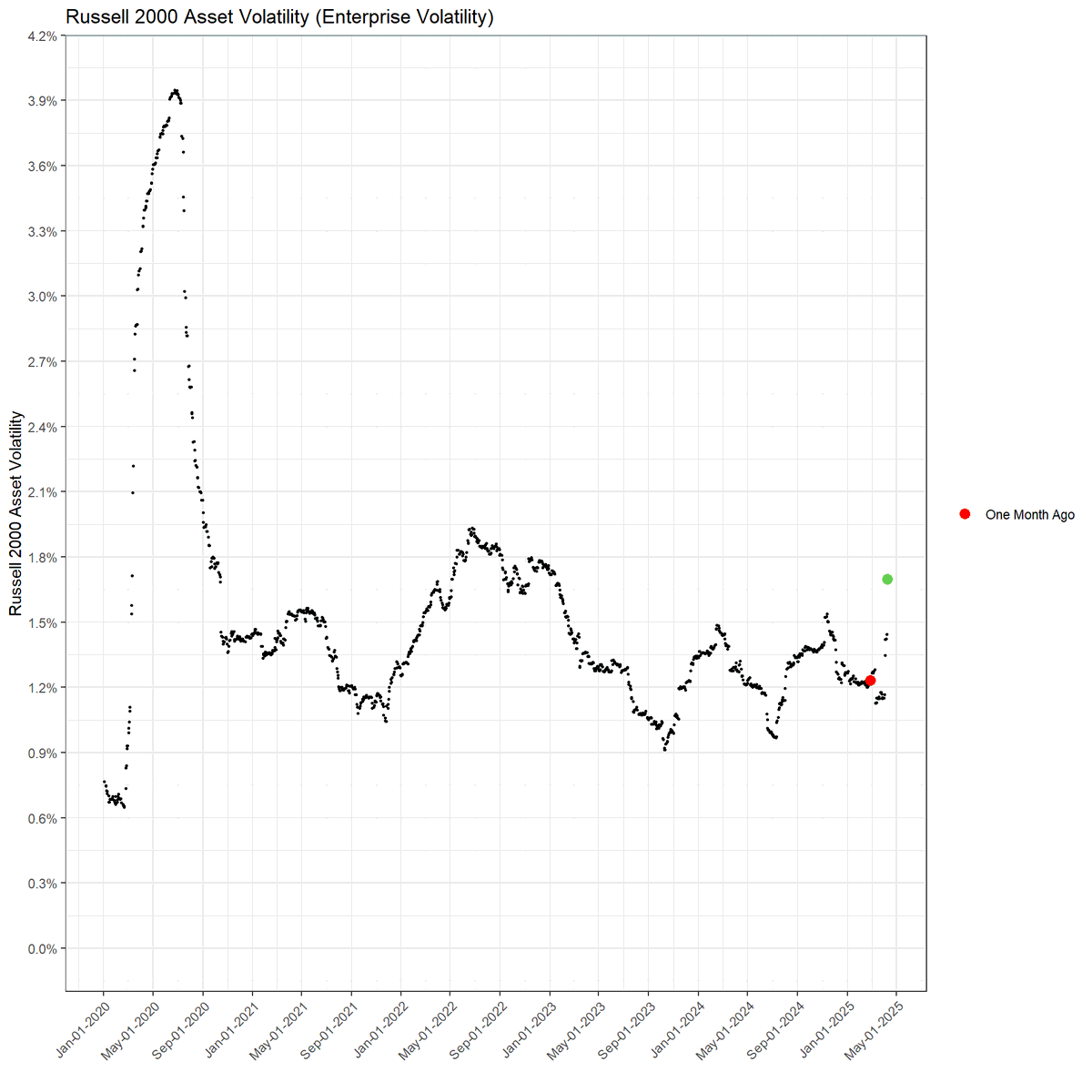

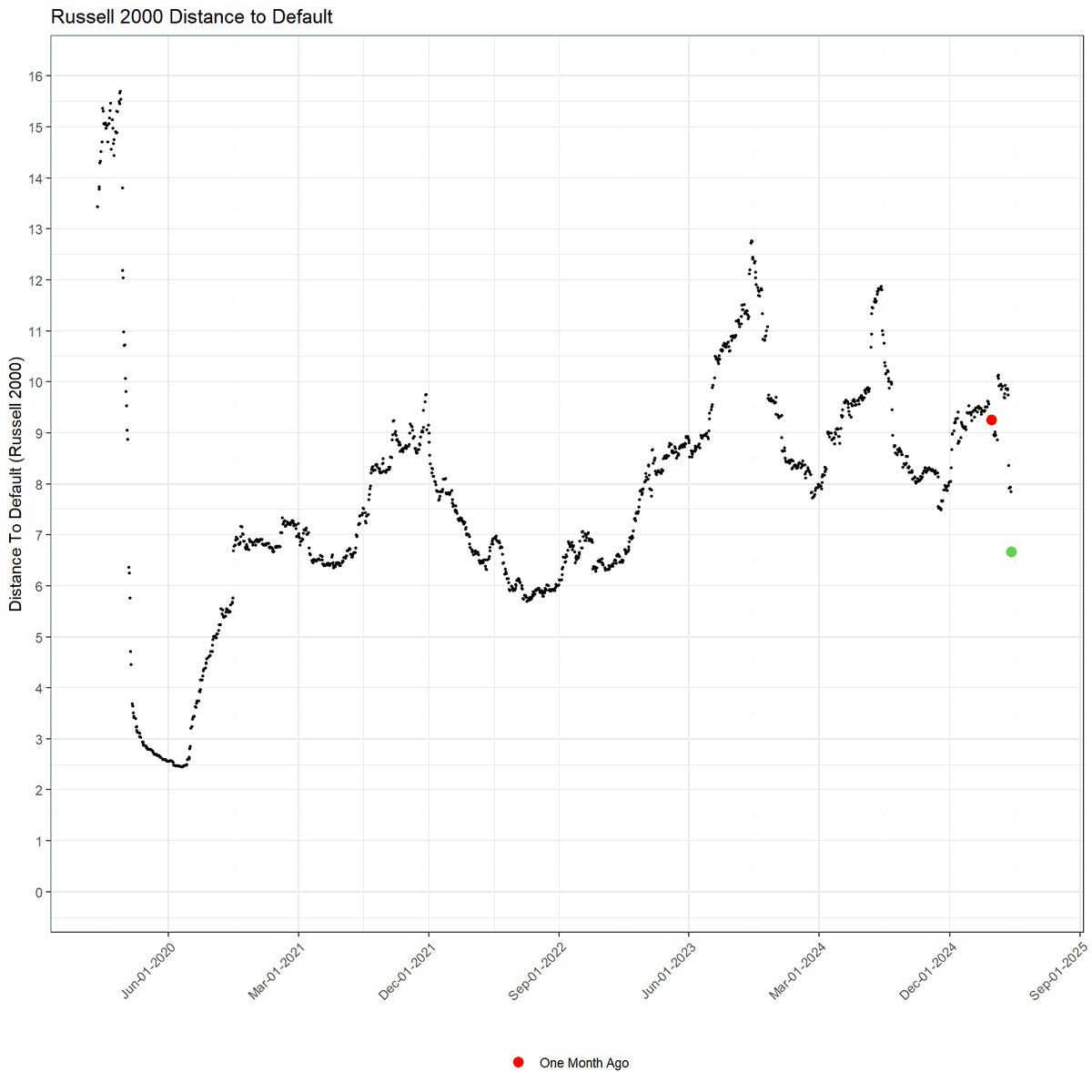

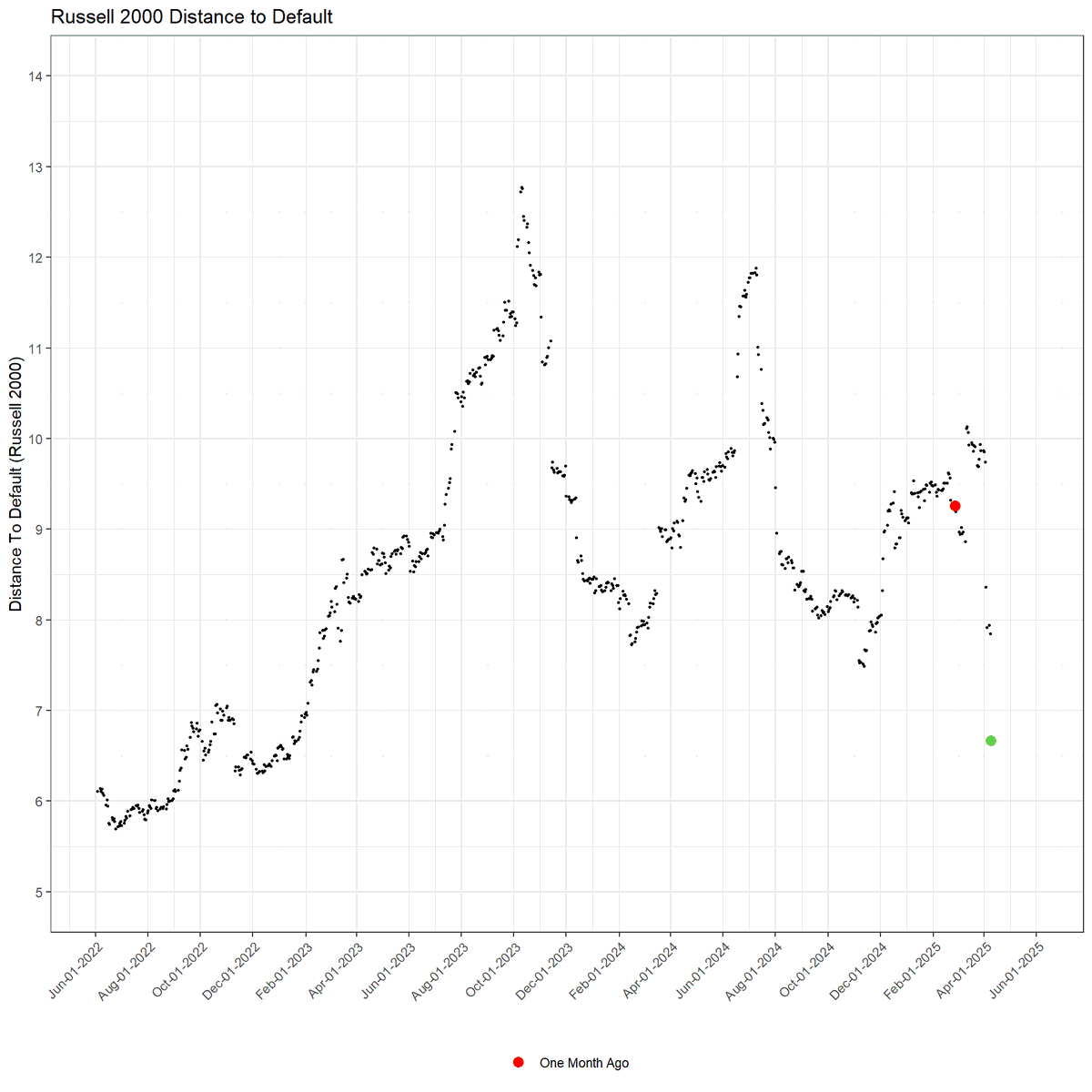

this is the current D2D from the volatility of the entire asset value of R2K, the level of the asset value of R2K and the interest rate to maturity. note that D2D continues to drop to new recent lows even with the rise in R2K level.

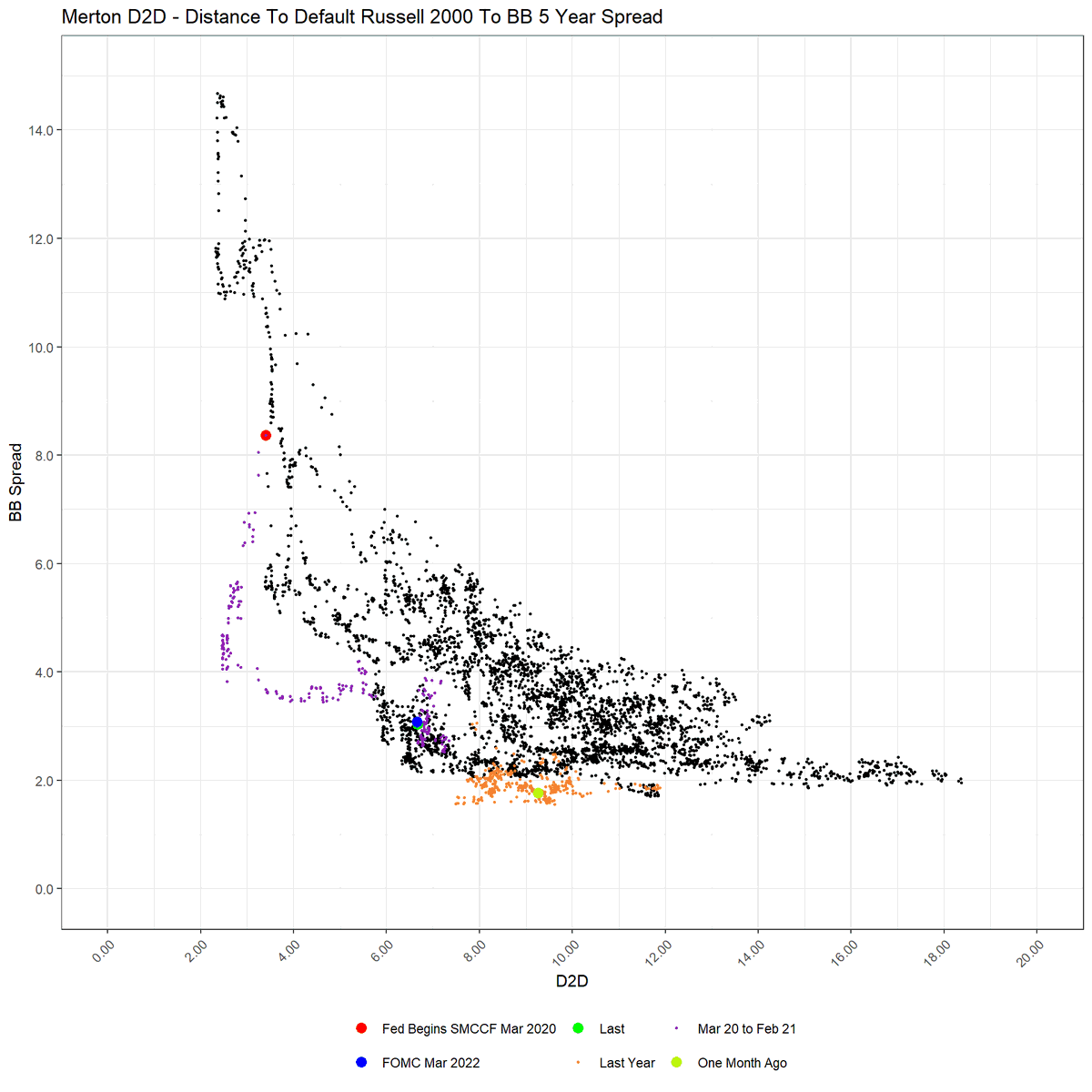

folks make the error that this portends more of bear in R2K, but that would be an error. the D2D is not a pricing mechanism only to qualify the current spread level in context of risk, price level and interest rate. therefore must be charted as (x) to credit spread (y)

the above scatters seems noisy but note that D2D is not trading in distress to credit spread but shows that the relationship is showing non stressed credit spread given the increased vol, increasing even as price level increased. larger scatter again, then recent.

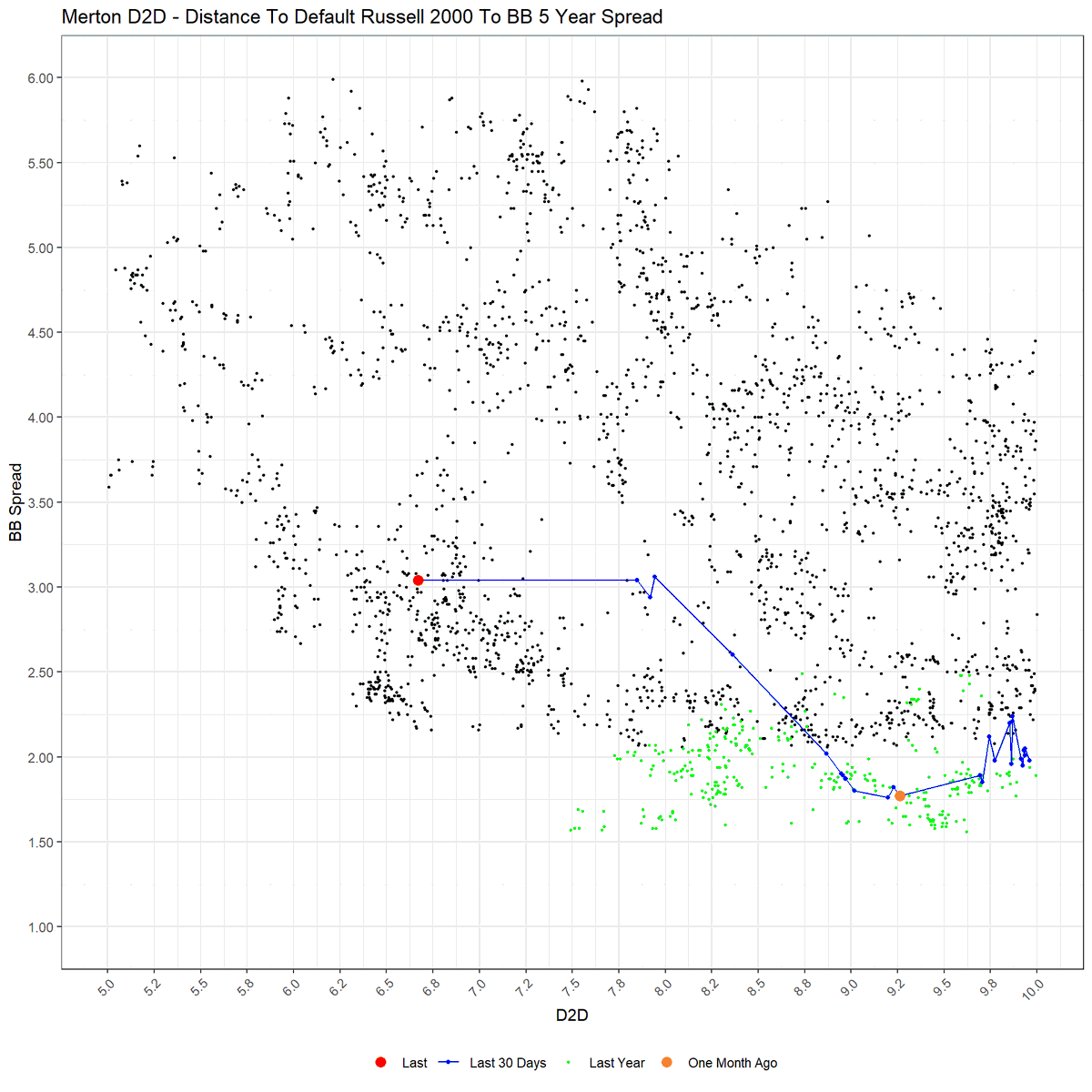

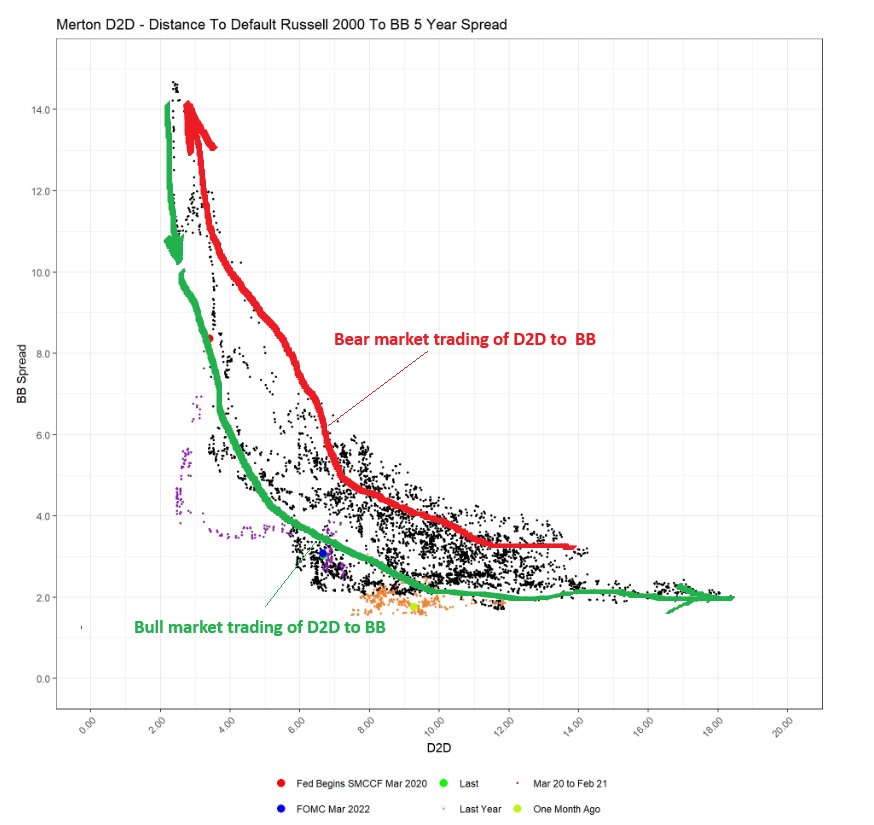

credit spread to D2D either moves on the top boundary of the scatter when markets under duress or close to the lower boundary when all is good. In a bull the realtionship can trade back and forth in proximity to the green, in bear usually is gap and only trades counter clockwise.

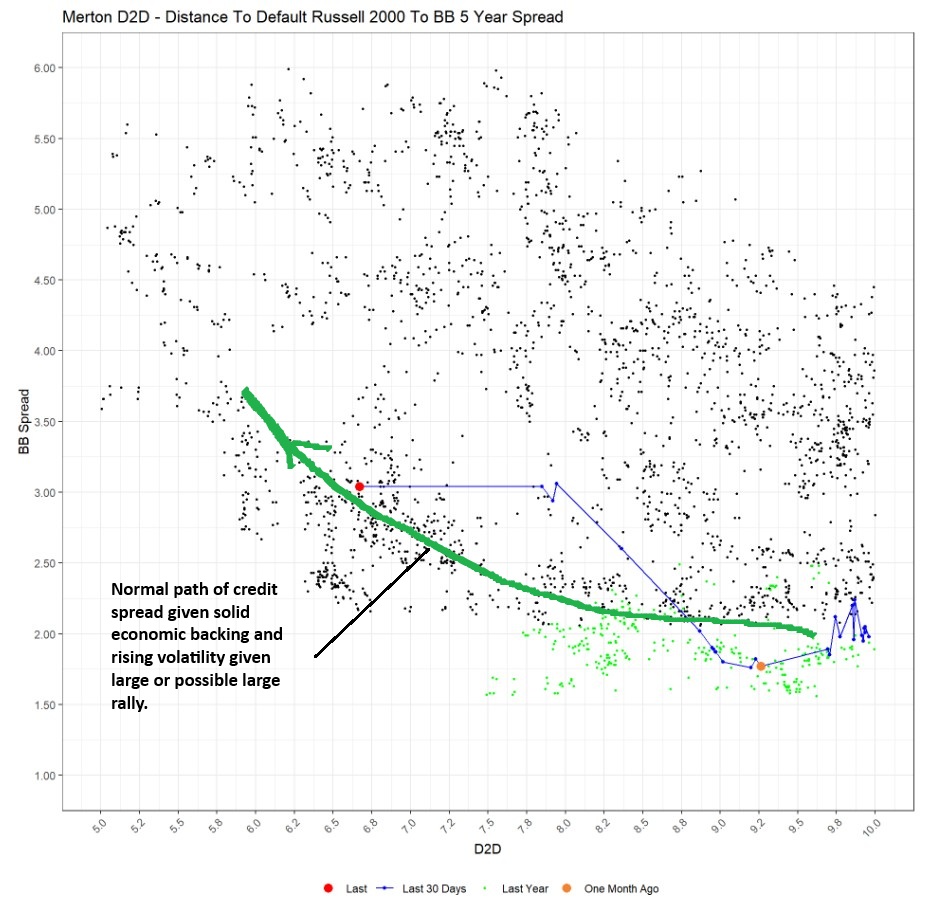

the current spread did not change but that it is maintaining towards the green area shows that while D2D dropped it was from increased volatility which often proceeds a large bull move.

this at first seems complex but is really common sense. current credit spread by maintaining the position of D2D towards the lower boundary indicates the bull market is still with us. the current pop view of credit spreads is not useful and wrong @TheStalwart