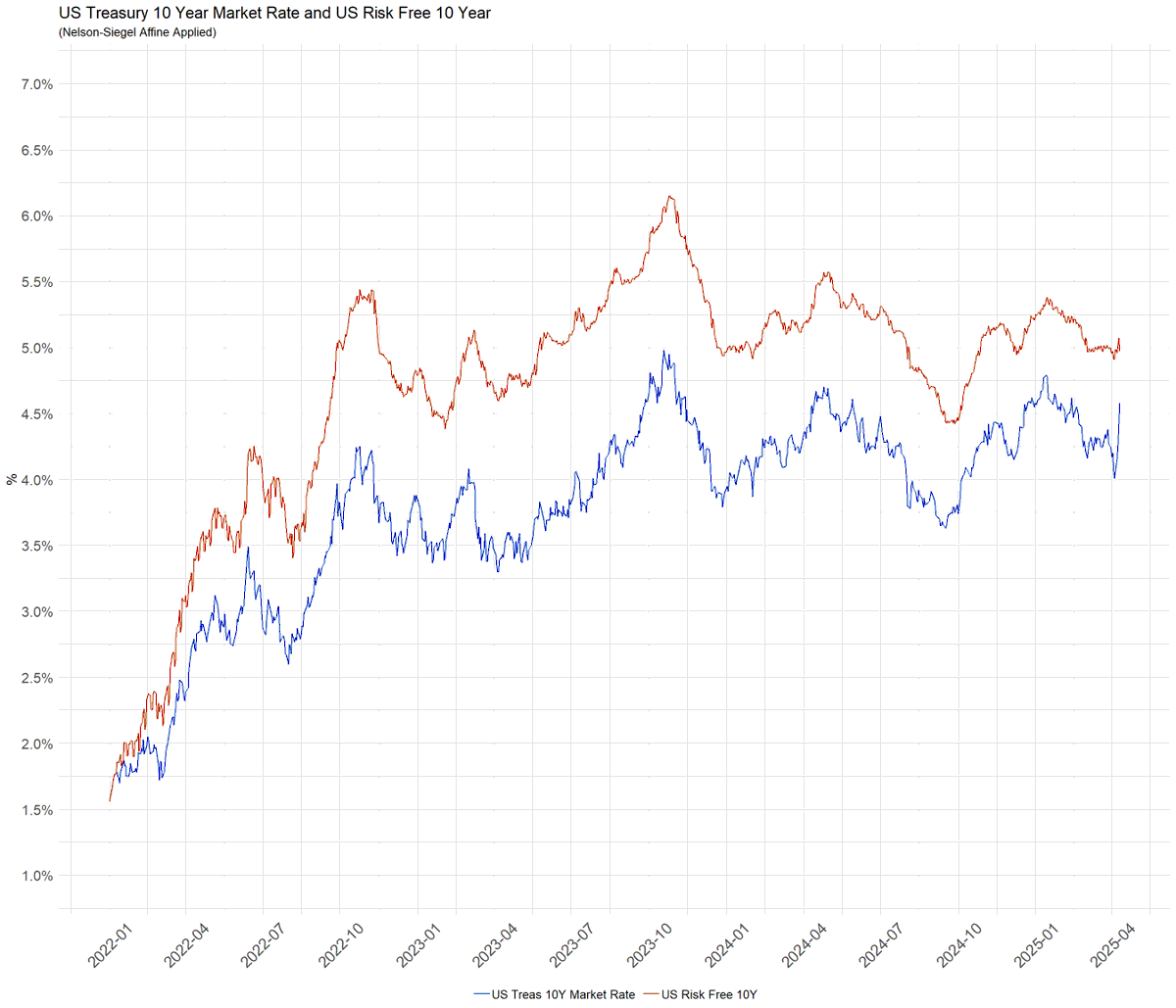

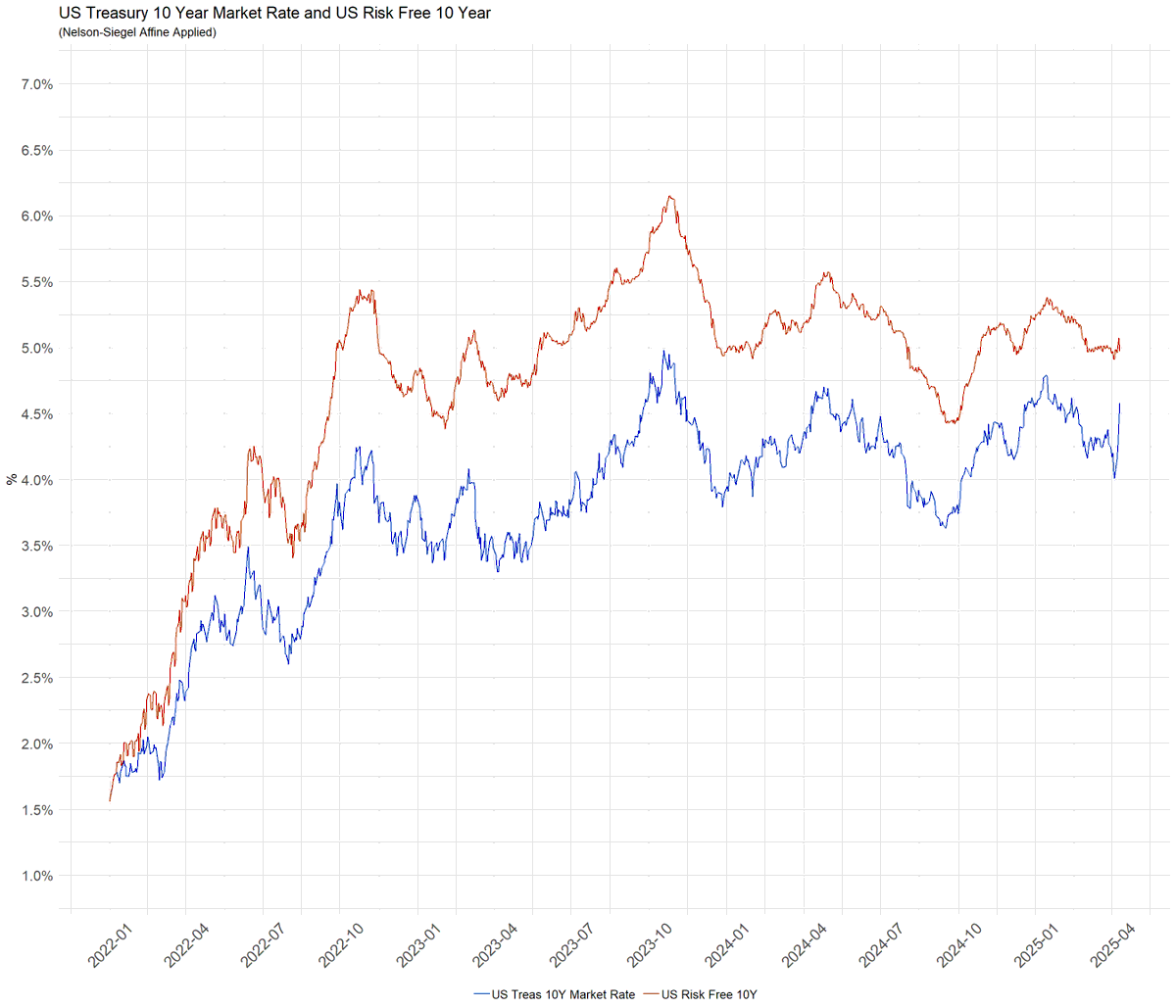

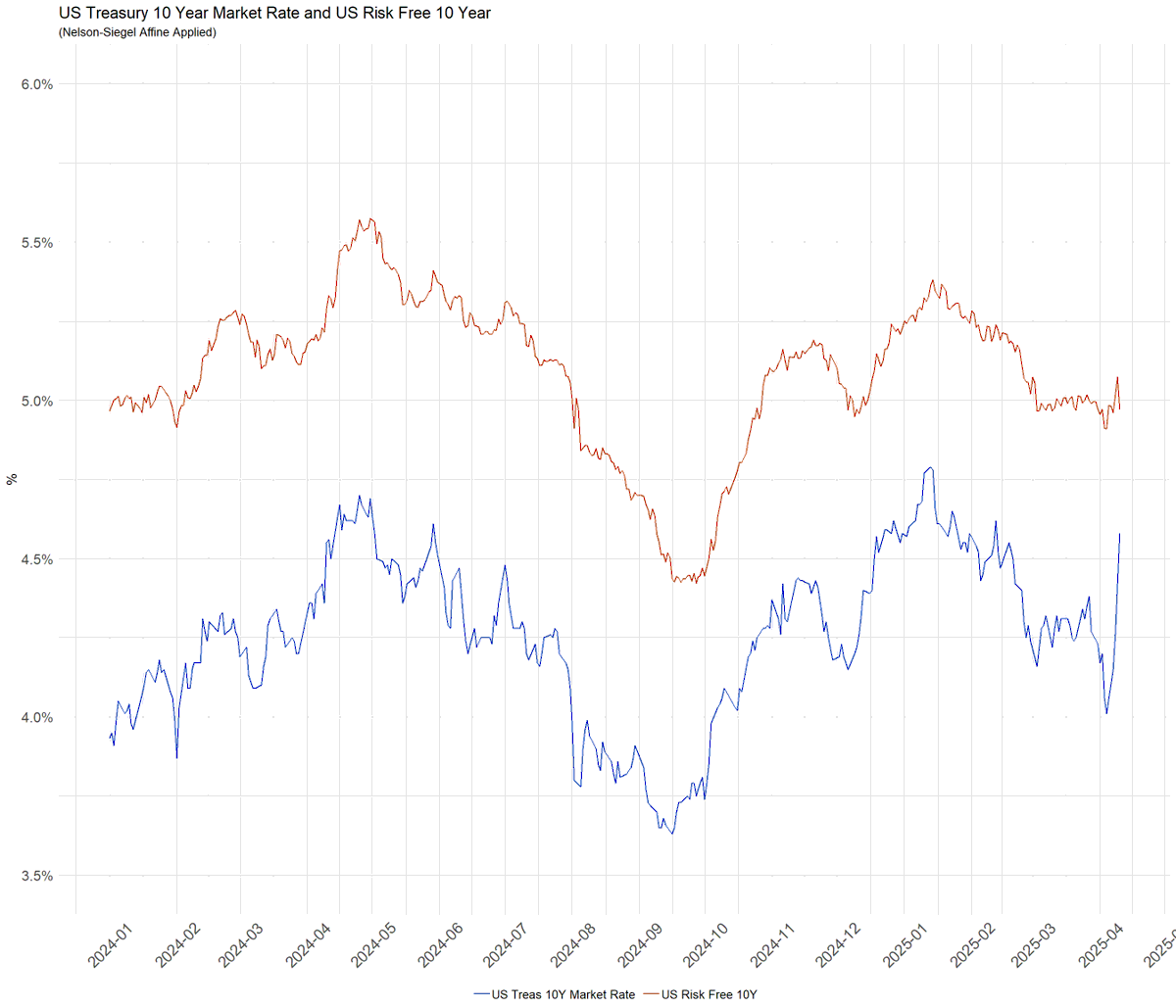

lot of commotion in US Treas 10 year but reality for the US risk free 10 year rate is it aint doing much of anything. the US Treasury 10 year is being spivved by HFT - likely Citadel - who is harvesting like sorghum. down to 4% back to 4 5/8% then likely back. illegal.

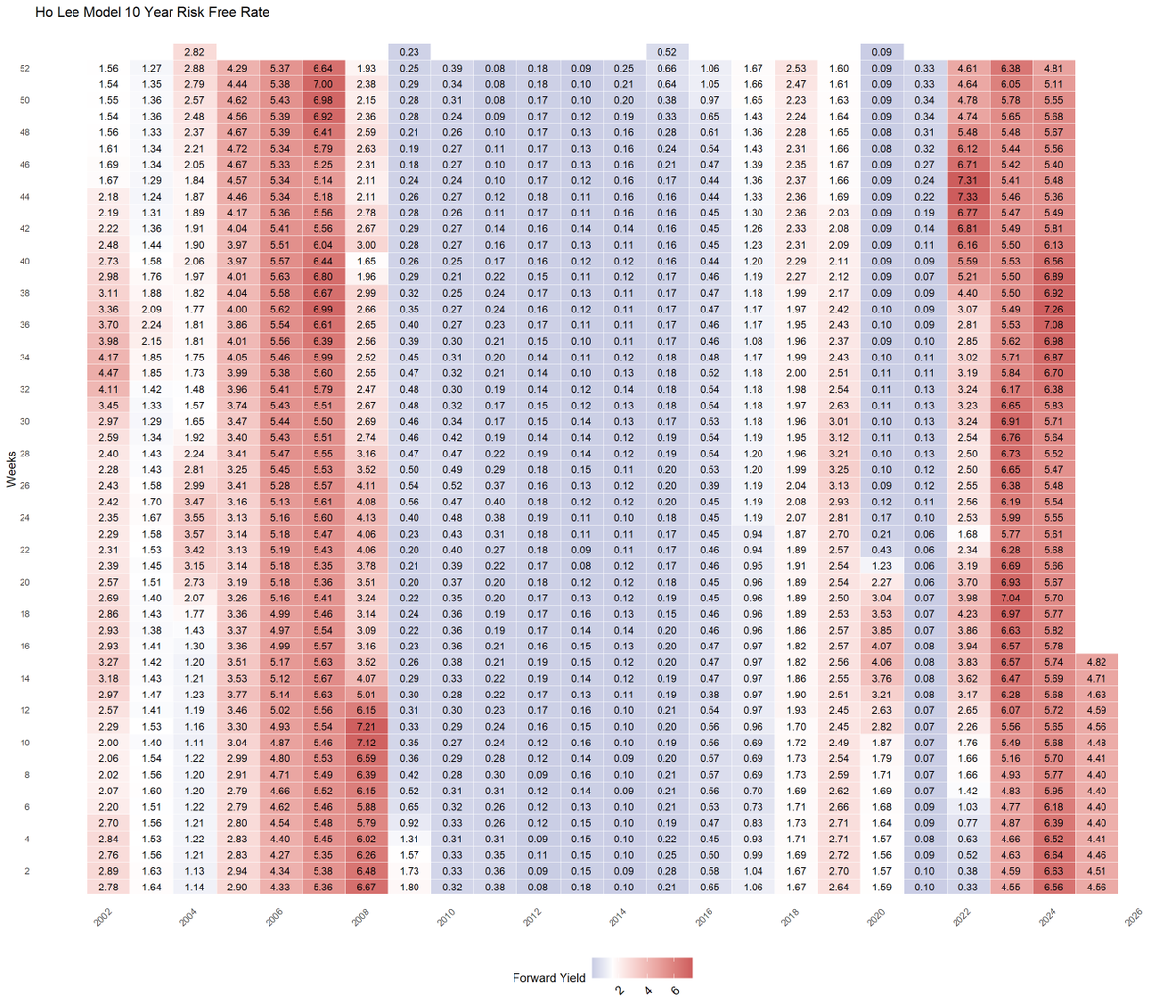

the risk free rate is bootstrapped by the 10 year rate that matters in terms of the econ, inflation, risk free, and reality - a bootstrapped rate from conventional 30 year mortgages that end up in GSE MB.

those going on and on that US Treasury 10 year movements of late reflecting the econ and possible recession is as goofy now as was when it screwed everyone over in 2022 into 2023 recession calls.

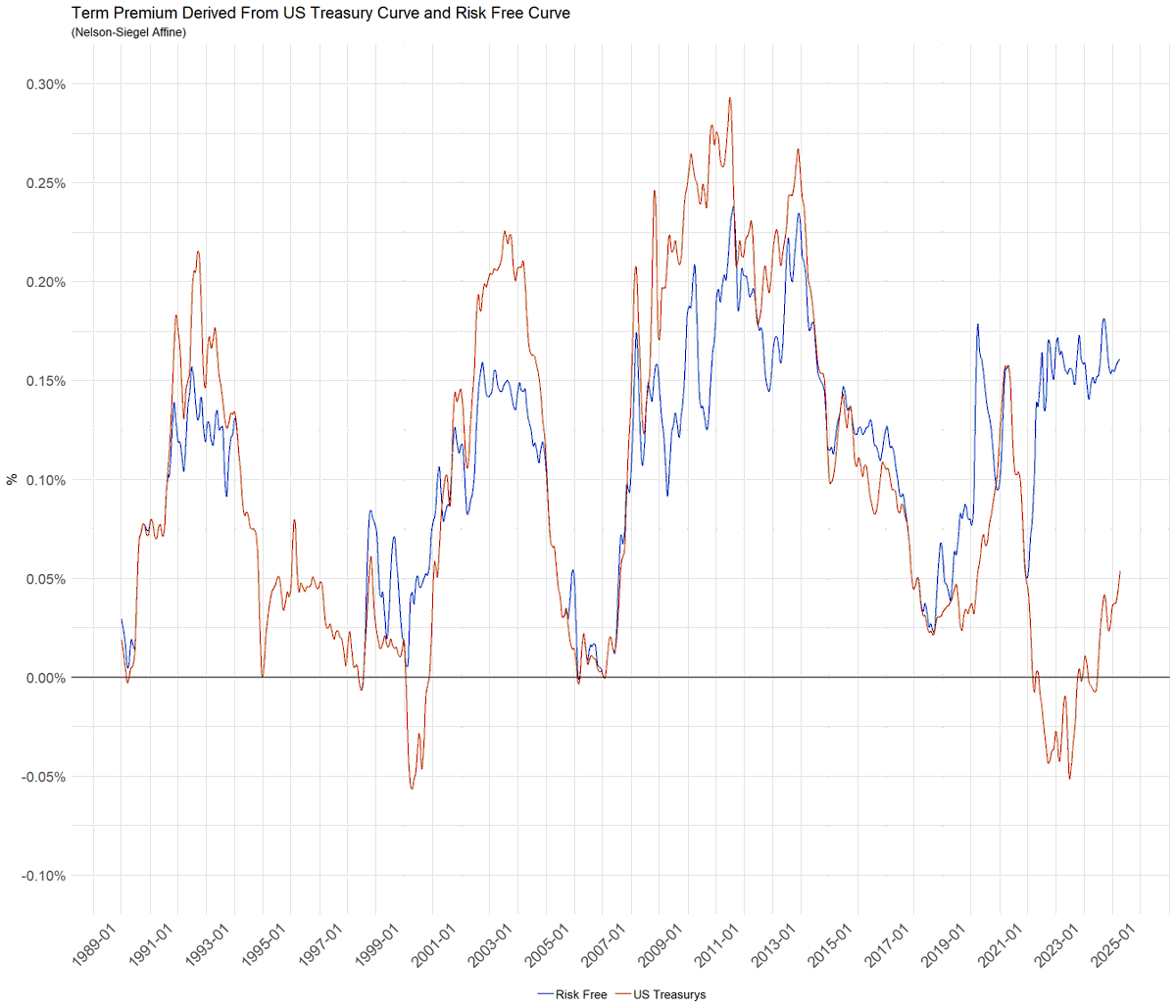

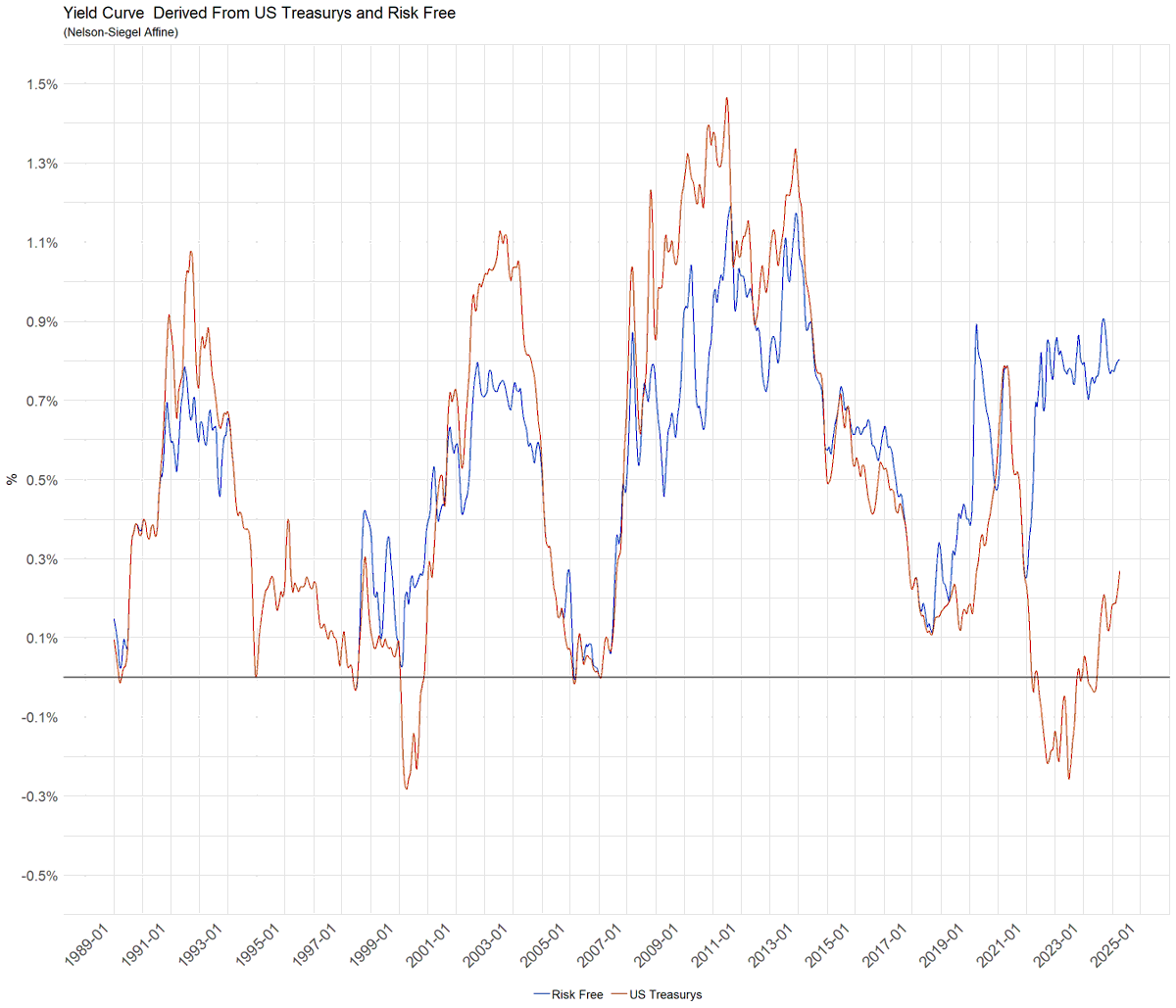

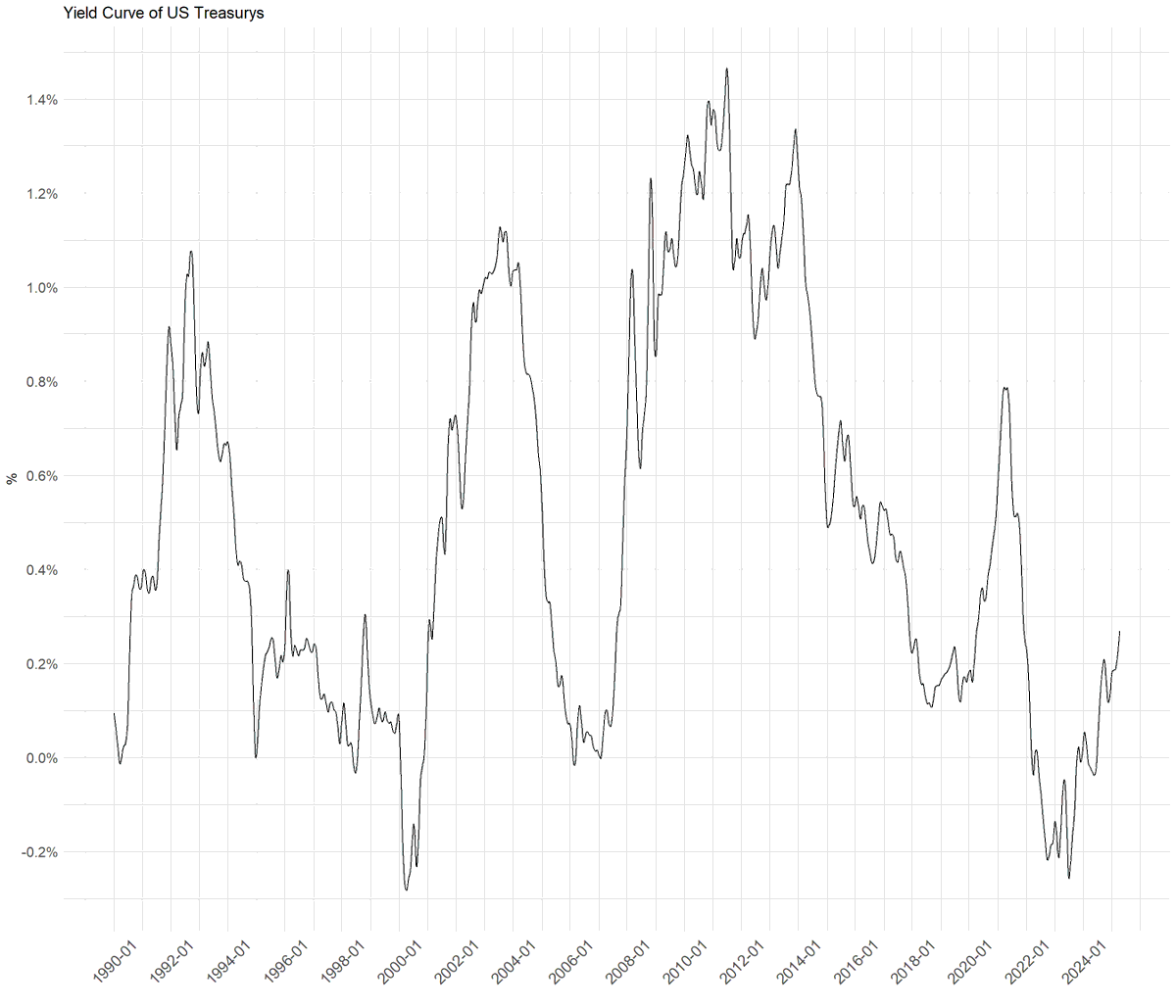

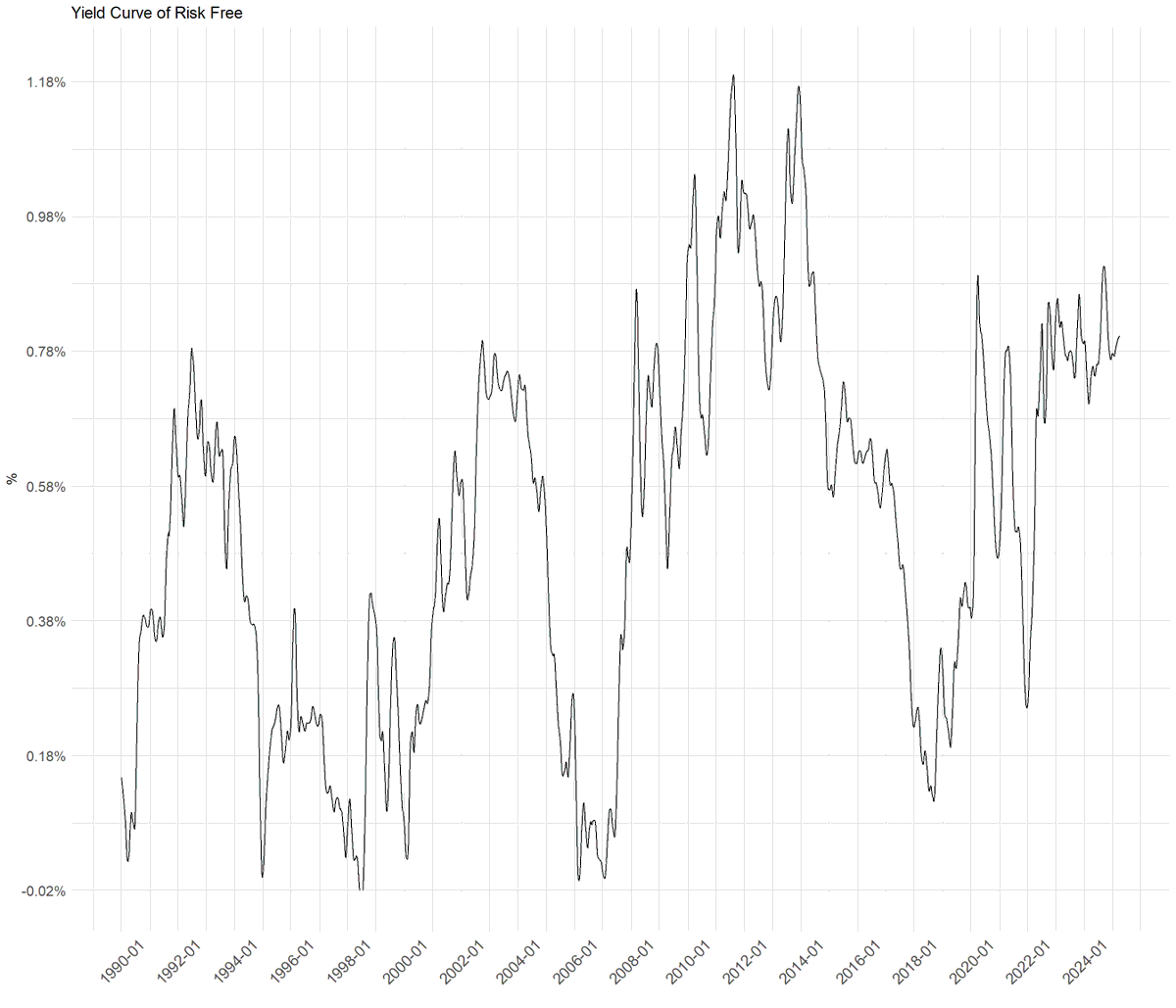

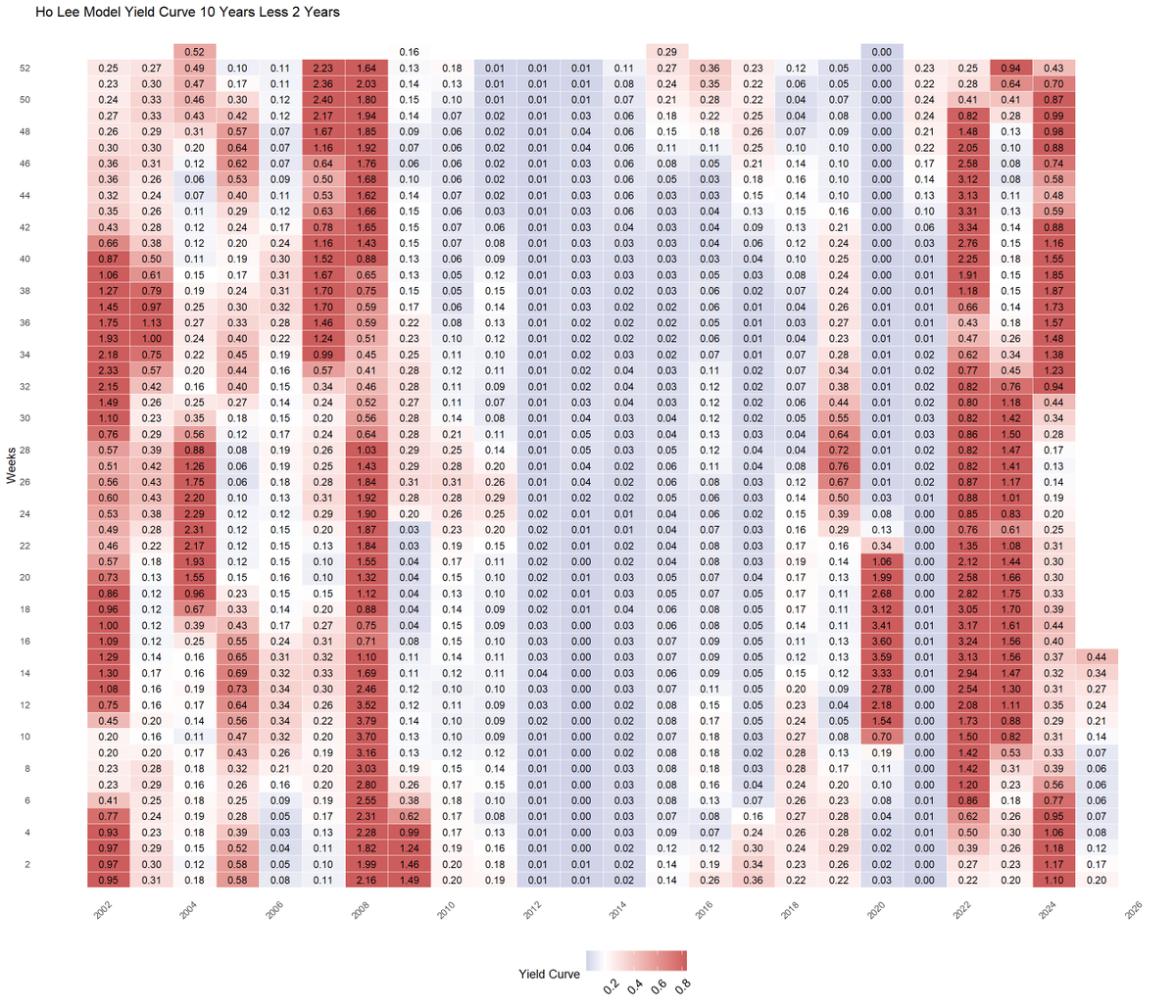

the yield curve derived from the US Treasury 10 year being gamed and about 5/8% below risk free has been useless to understand the economy and then equity. even if has recently steepened. it is the "phony curve"

the actual yield curve in the USA has indicated strong consistent growth wince 2022 and accordingly growth has been strong and consistent since 2022.

the above risk free rate is anchored with the bootstrap from 30 year conventional mortgages which go into GSE mortgage backs. if one doesnt do that but just use Merton's process (same approach as in Black Scholes Merton) same story in brief but more dynamics.

it is interesting to see that there was some concern as to what Trump was going to do to the economy using a Merton projection. but over last month or so that is alleviating as strong economic data continues.

a tell in figuring out if folks understand macro or do not is to see those who do not understand US risk free rates are always neutral to the economy (Fisher) and go on and on about supply demand of risk free setting risk free pricing which is a de facto tightening or ease.

it is always neutral. an extension of this is those babbling about credit spreads forecasting a recession. credit spreads will price a recession and be the first to do so but are not forward looking. perhaps the goofiest spiels are those babble higher US Treasury 10 y

is going to weaken housing/home builders. first the 30 year conventional hasnt moved much is anything has moved lower a shade. but in any case higher 30 year conventional indicates stronger residential market @TheStalwart

it is time we start to retire these notions which have stymied or made many ridiculous since Covid if not before. get out Fisher, figure it out. stop this inane babble about risk free rates and impact on the econ. there is none as the nominal econ prices risk free.

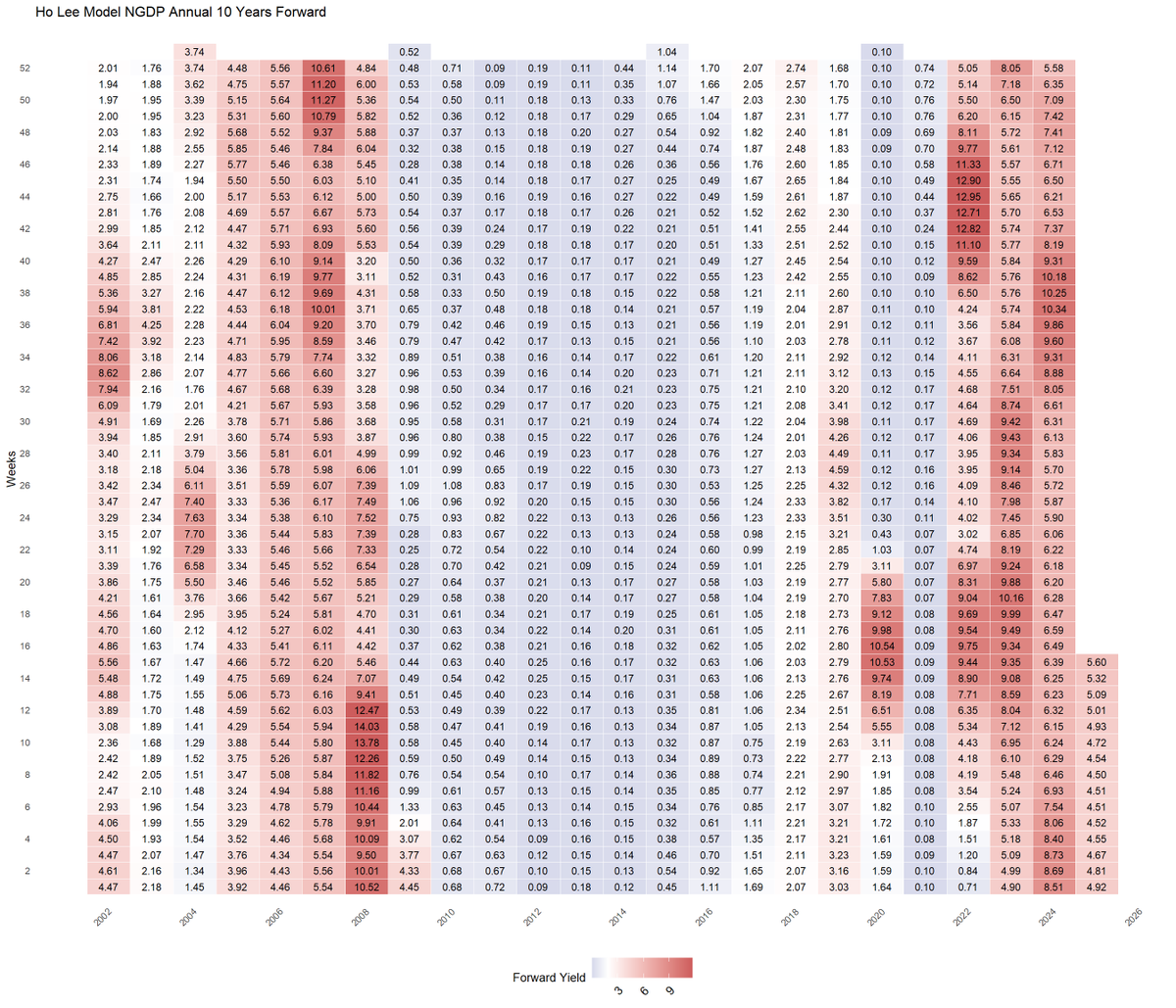

the yield curve is always the schedule of expected NGDP. since 2022 the US Treasury 10 year has not reflected the economy and to lesser and greater degree has not been the risk free rat, it is manipulated.