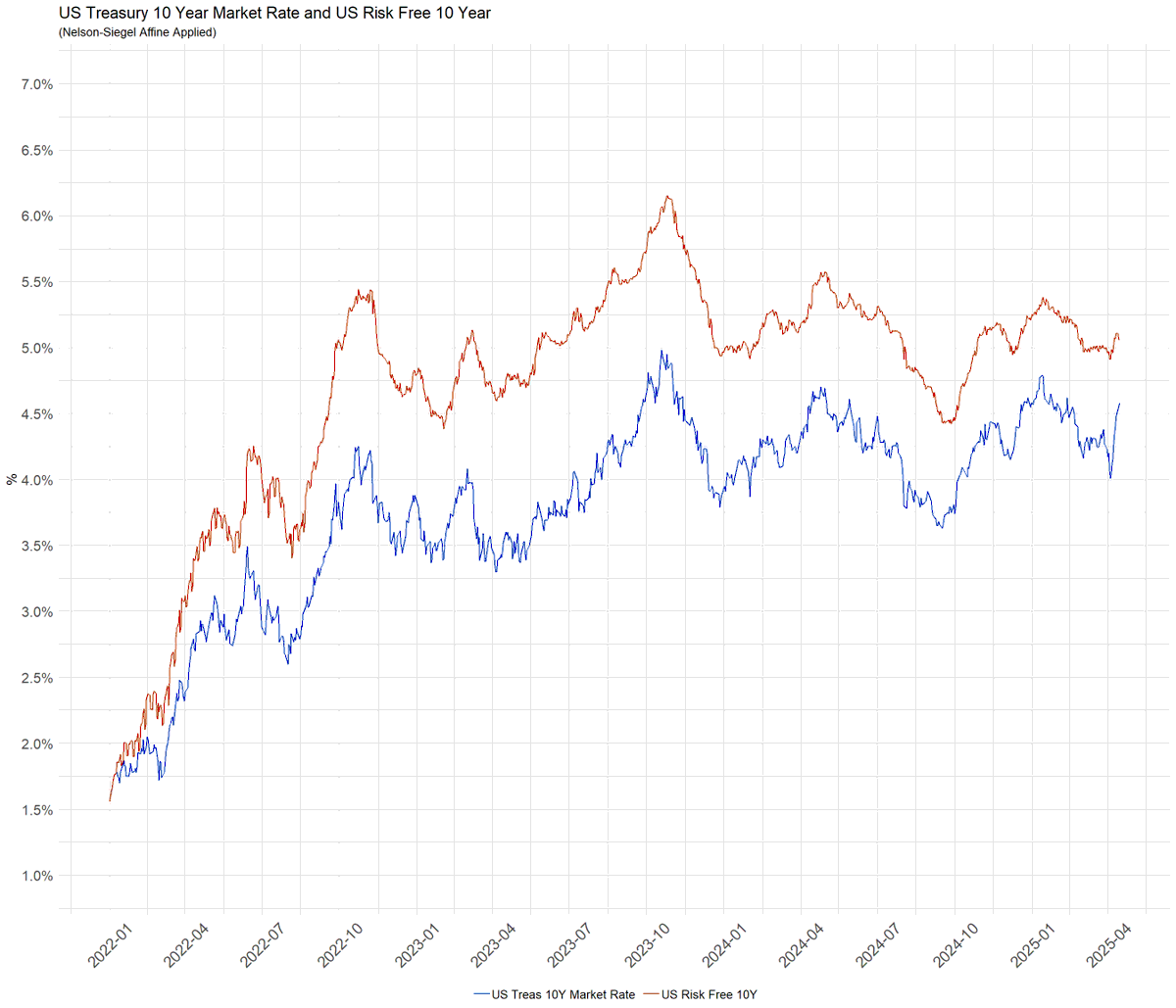

there really is not much going on in 10 year risk free rate. the UST 10 year is being gamed by very large HFT basis trades unwind using the treasury 30 year auction liquidity as the trigger to unwind, very similar to the QIII 2023 wilding.

this is manipulation of rates which is illegal. beats me why Fed/SEC not pressing charges. there will be indictments sooner or later. US Treasurys are perfectly elastic (in the end) with supply and demand have no effect upon rates but for sector segmentation from gaming...

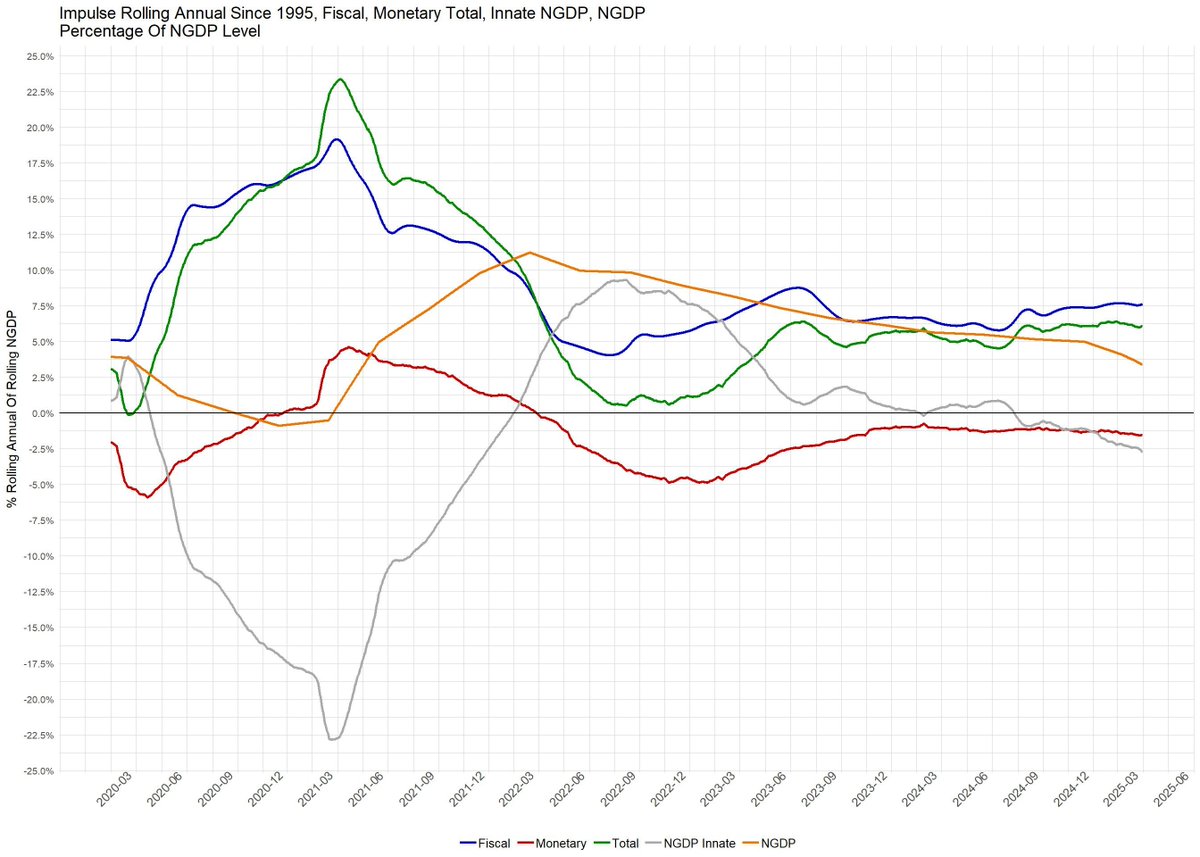

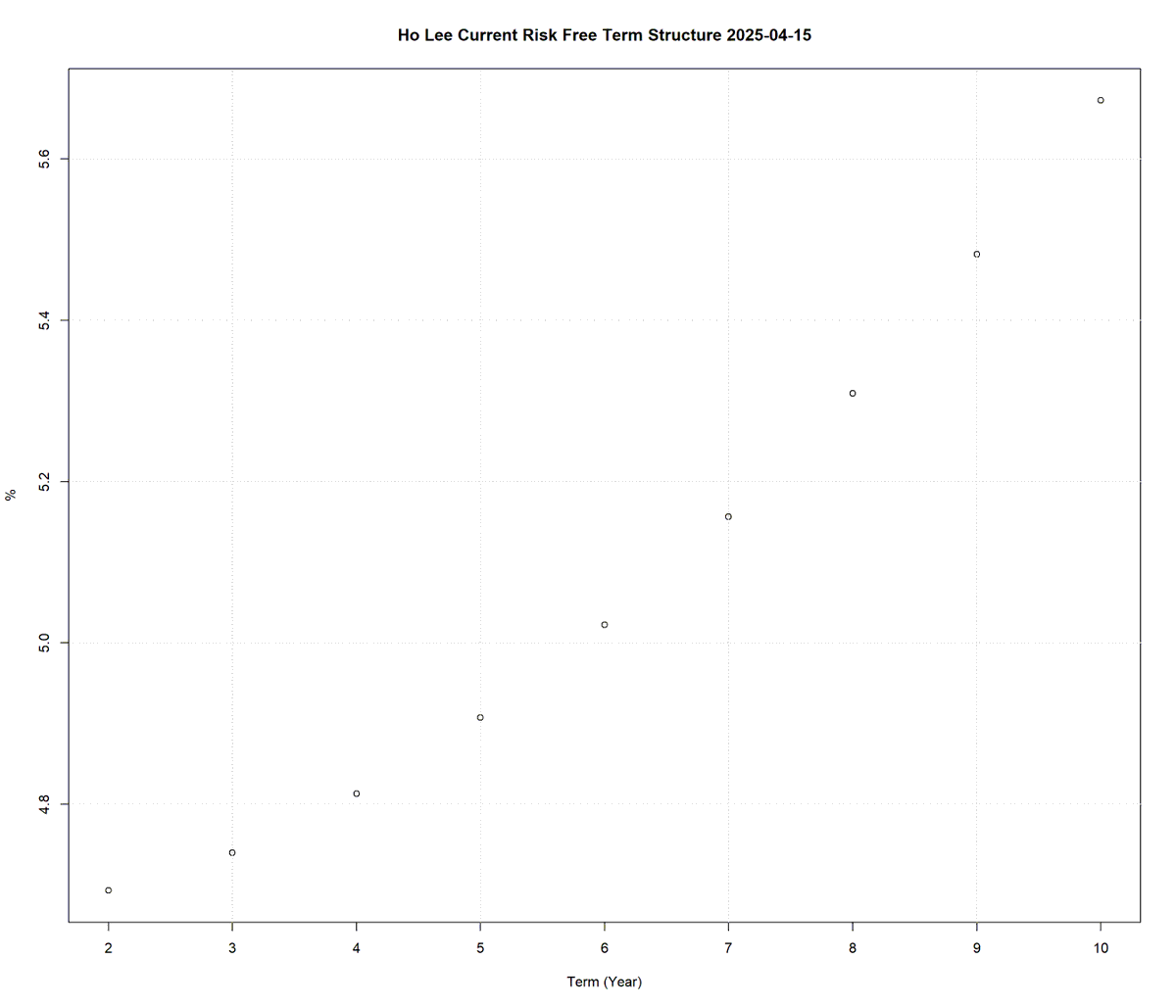

...or as the Fed has seen fit to set the entire rate curve downwards and lower yield. this rate setting by Fed allows or invites the HFT to manipulate the Treas. the actual risk free rate - the rate US Treas 10 year is usually equivalent to the 10 y risk free rate - has remained as per a 5% to 6% NGDP growth since Covid

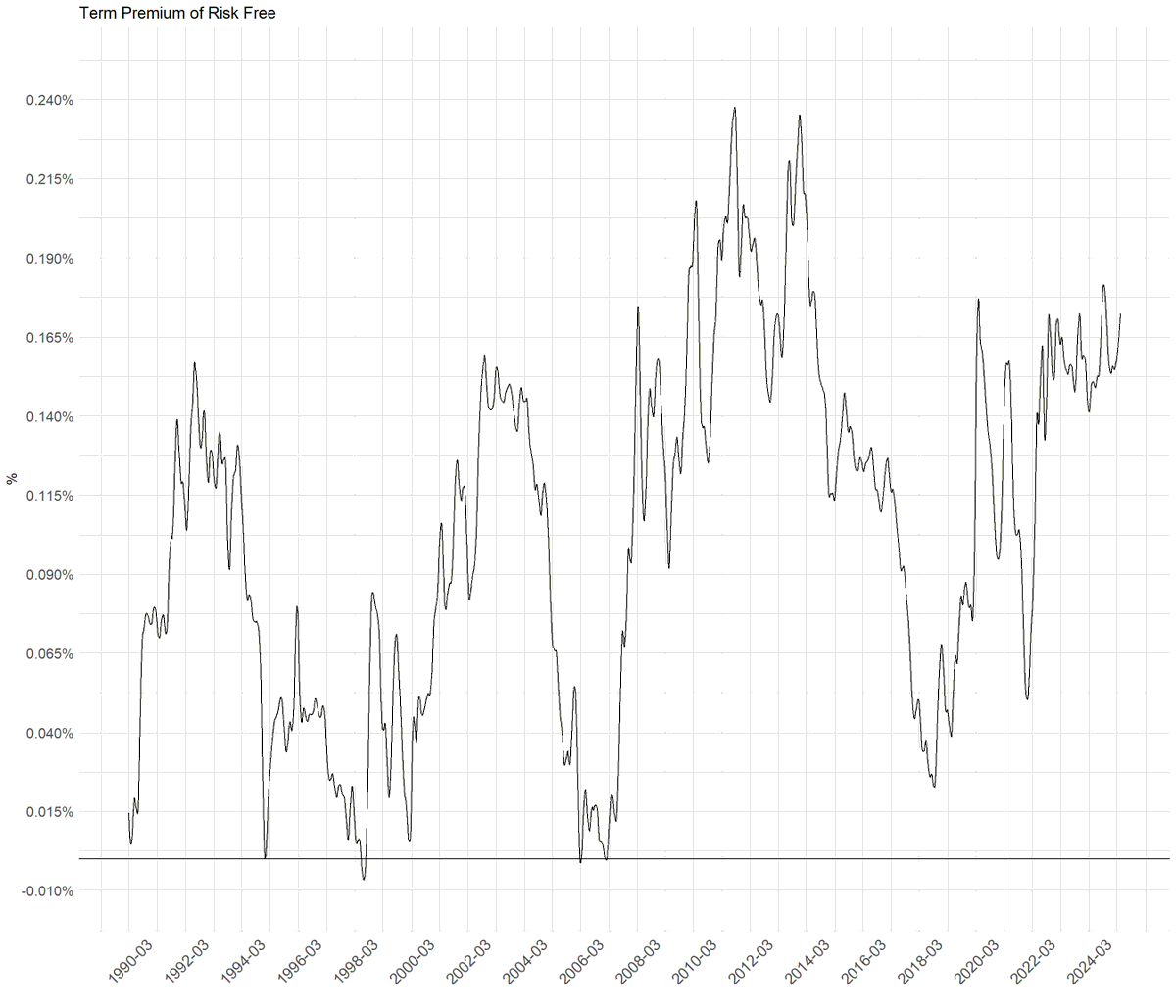

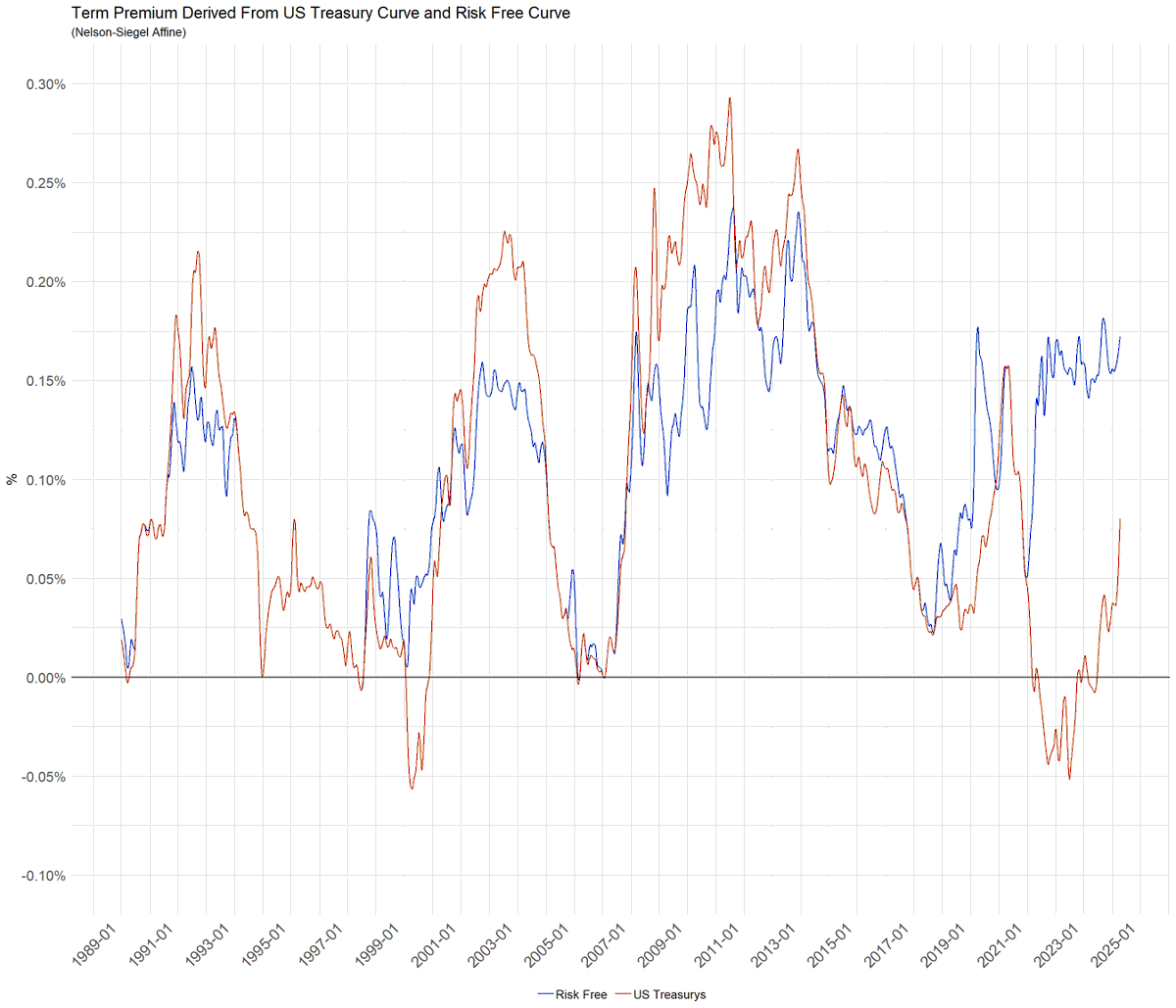

the reported change in "risk premium" which is the change in yield per change in time is not from duration risk or maturity schedule but to price the volatility risk of Fed Funds changing. the risk premium for risk free has been stable since 2022, slightly rising as vol increases

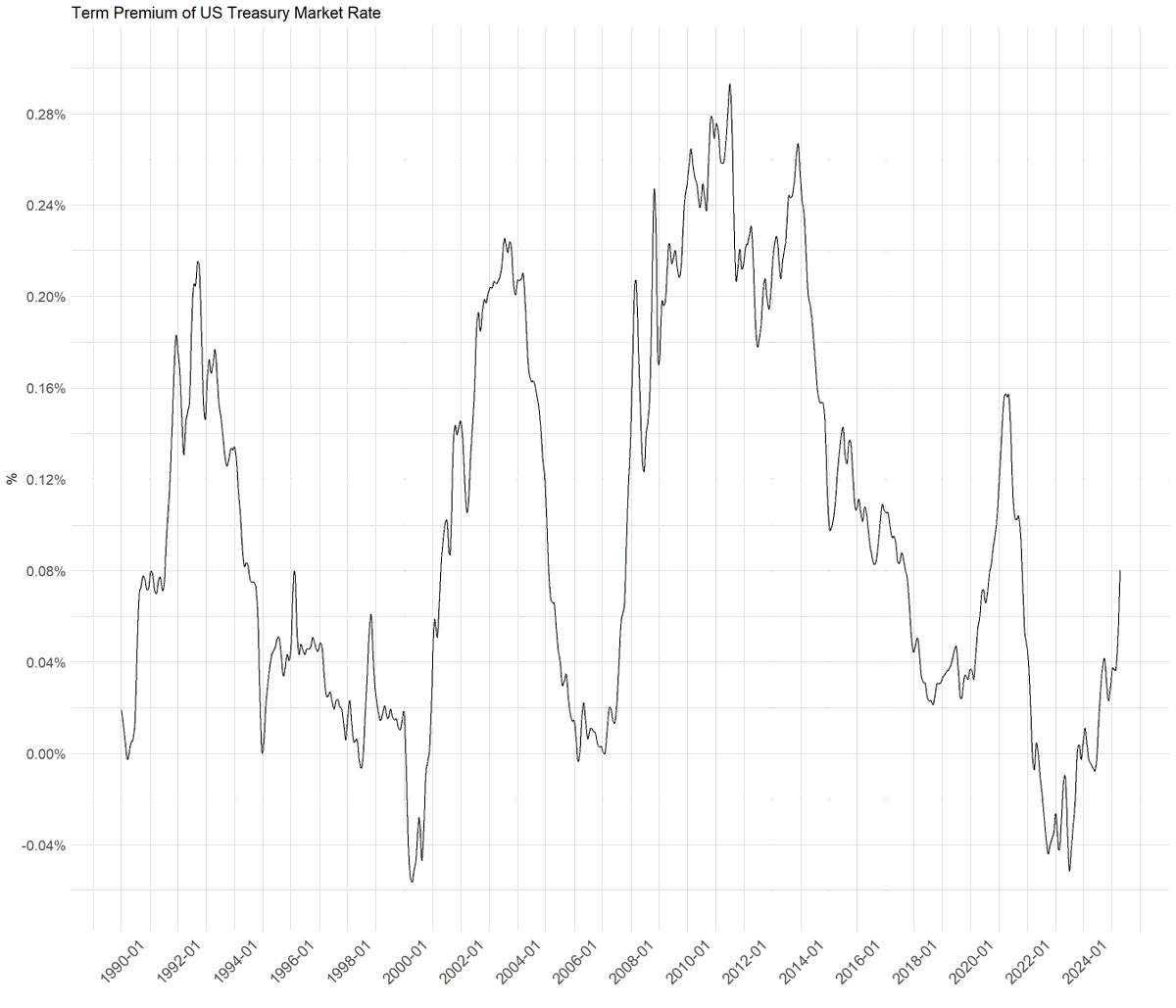

the risk premium the focus now from market rate US Treasurys 10 year has nothing to do with the economy and is not the macro economic term premium.

the actual term premium to the US Treasury market rate risk premium

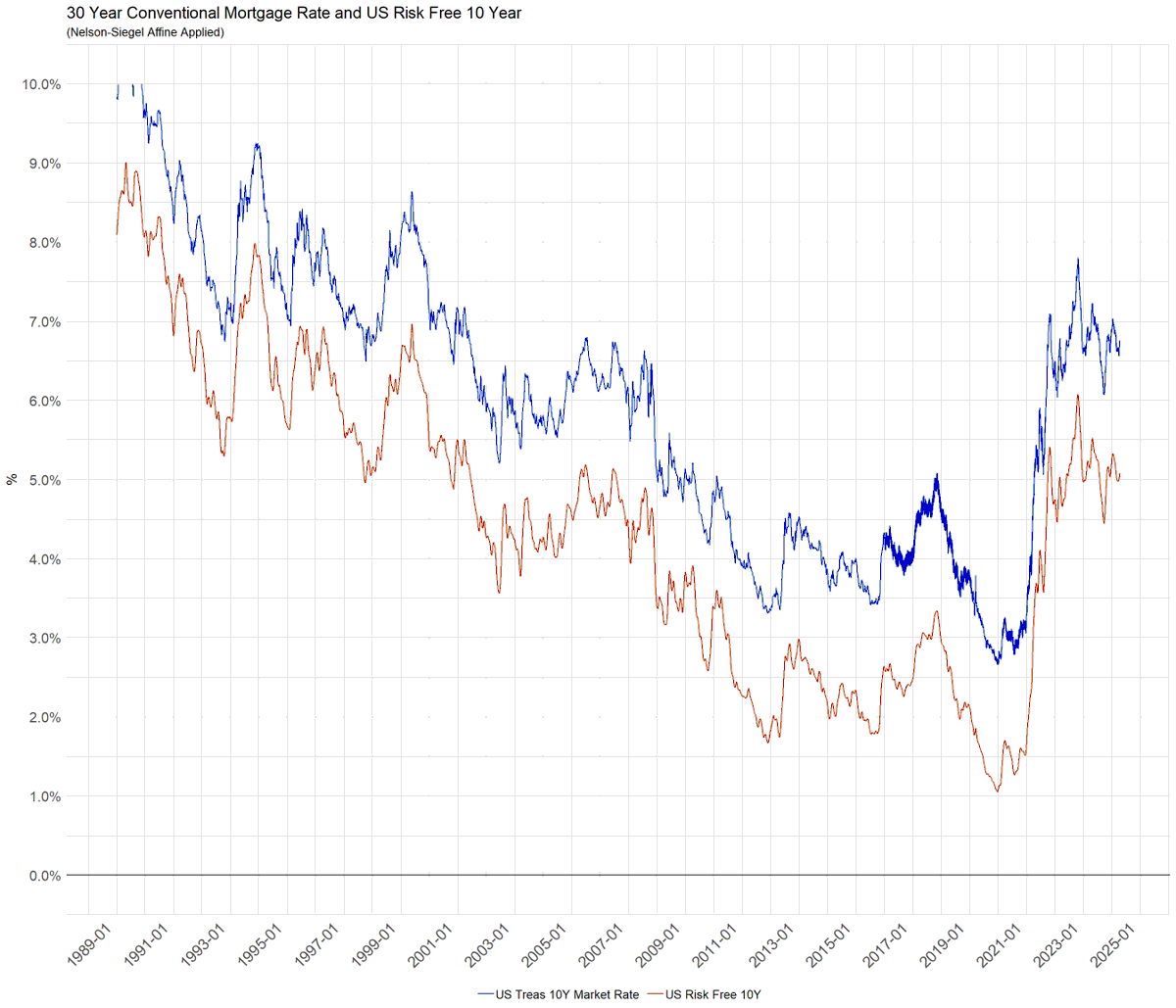

the risk free 10y above is bootstrapped from the pricing of the risk free corpus of the MBS from GSEs and is from the conforming 30 year conventional and complying mortgage rate. the 30 year mtg rate is as one would expect given the residential real estate market since 2022.

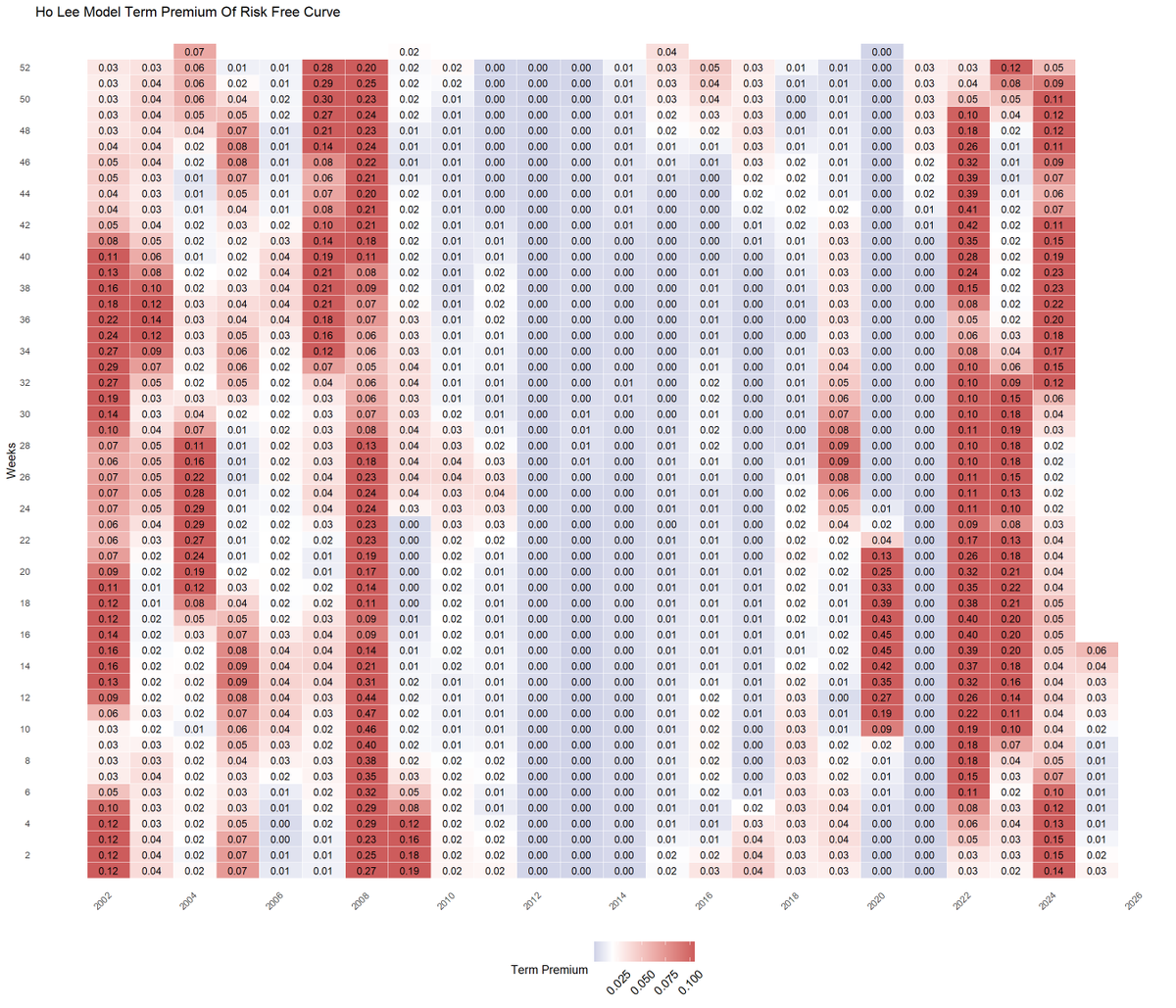

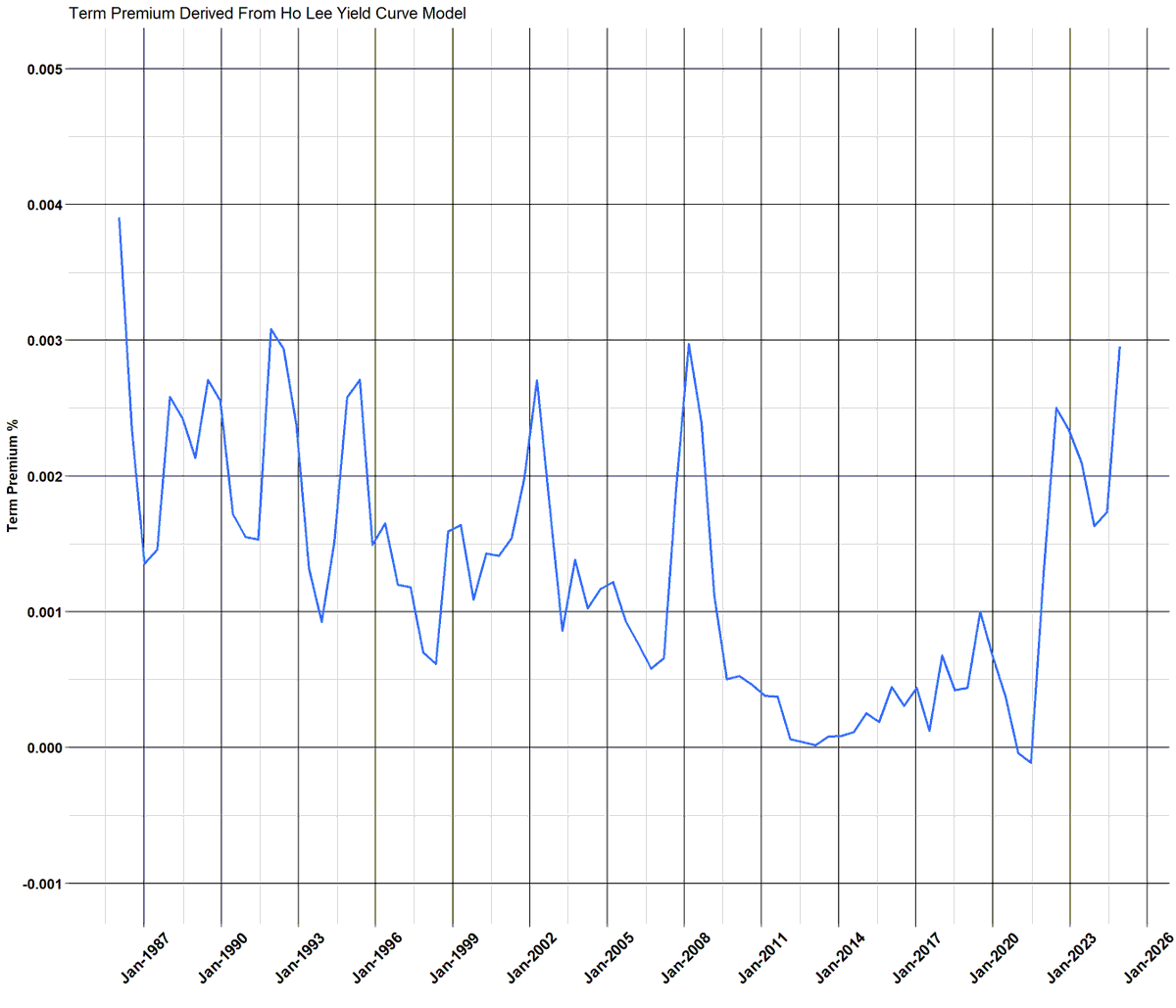

a calibration of sorts can be had by not using a 30 year mortgage rate but to use the Merton expansion of spot risk free rate (imagine a 3 month Fed Funds rate) use the volatility of the 2 year US Treas rate and then transform to a 10 year rate. this is conceptual but does provide a useful term premium and how that changes

the Merton approach using vol is unanchored to a pragmatic range of likely 10 year rate, which is the same as a basket of NGDP rates for 10 years. but the dynamics are useful showing a drop going into Jan 2025 but then a rise to date, this forecasts ongoing strong econ

risk free fixed income and term structure do not show any anticipated slowdown in the economy due to Trump Agenda and while discounting for Trump slowing down the economy they now depict Bidenomics as usual for 2025 , fiscal impulse. econ is strong